Technically Speaking: Past Performance Is A Guarantee?

“Past Performance Is no guarantee of future of results.” Such is the disclaimer below every performance chart produce by the financial marketplace. However, as Jason Zweig recently noted, that warning has taken on a different meaning:

“Being told that historical returns don’t ensure future success seems to make the typical investor rely on them even more. It’s as if the phrase ‘past performance is no guarantee of future results’ makes people think, ‘Well, if it’s no guarantee, then that must mean it’s just pretty close to a sure thing.’“

The more the market rises, of course, the more investors extrapolate the current trend into future returns. After all, with the Federal Reserve pumping $120 billion a month into the financial system, what will stop it from going higher? Such is why you see headlines like this:

In that article, Mark Hulbert makes the excellent point that “if” the Nasdaq continues its current pace of advance, it will double in price by 2023. Notably, while the headline will certainly get clicks, he discusses the dangers of making such an assumption. However, it represents the “psychology” of investors caught up in the heat of the moment.

The Guarantee Of Past Performance

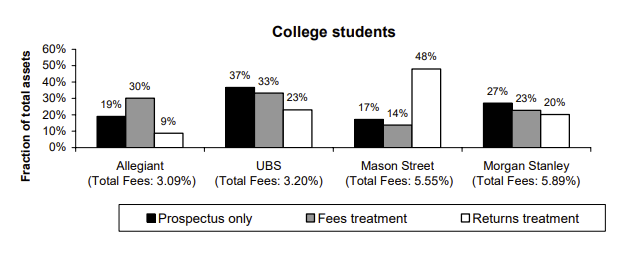

One of the mistakes that investors repeatedly make is in the investment decision-making process. A Havard study on the selection process by individuals of high-fee index mutual funds made an interesting observation.

“Finally, highlighting misleading long-horizon historical returns by providing the returns summary sheet caused

students to allocate more money to the fund with the highest long-horizon historical return.”

The point here is that only looking at the long-term history of any investment, a misleading assumption of potential future performance will likely get made. In other words, if the investment “X” returned “Y” annually over the last 10-years, it should do the same over the next 10-years.

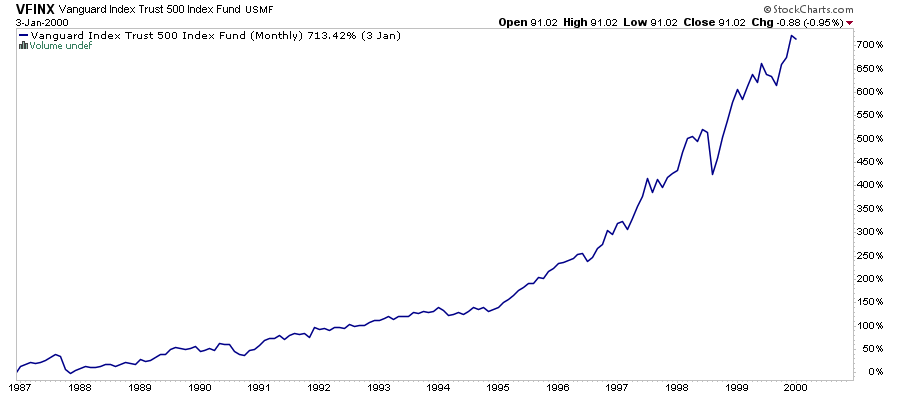

What gets missed in that assumption is the difference between starting periods. For example, take a look at the chart below of the Vanguard S&P 500 Index fund. (The index is total return with dividends reinvested.)

If an investor started investing in 1987, the fund generated a 713% return over the next 13-years. Therefore, an investor would look at the performance and assume they would experience the same rate of return if they bought the fund.

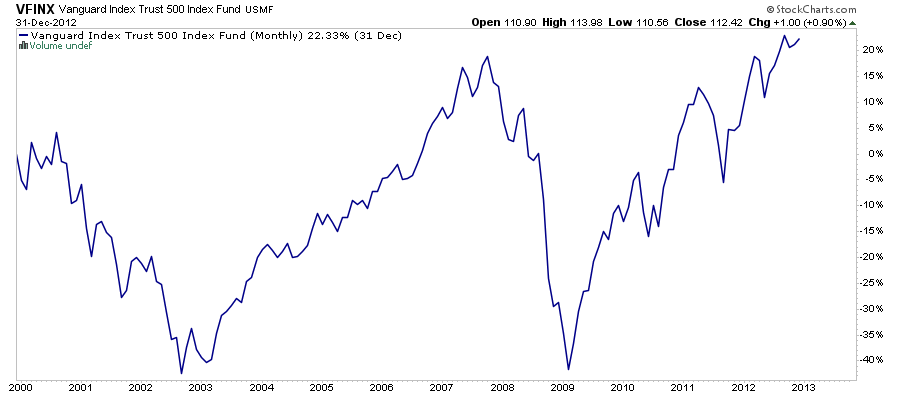

Unfortunately, such was not the case over the next 13-years as the fund returned just 22% on a total return basis.

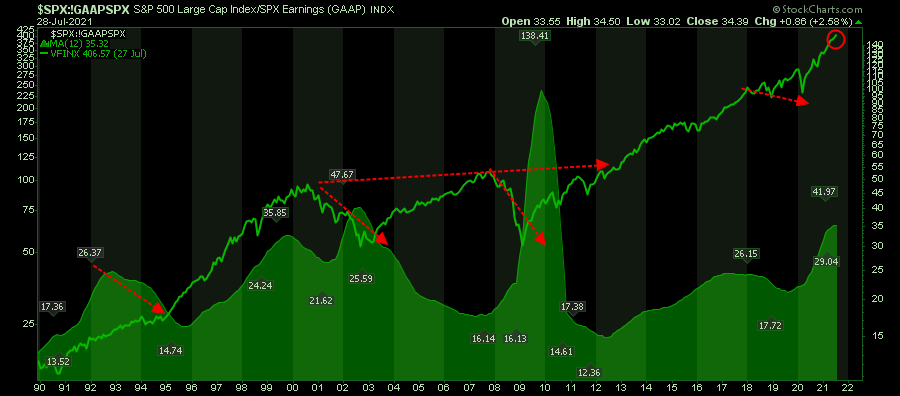

What was the difference between the two starting periods? Valuations.

(The chart below, courtesy of Stockcharts, is the 12-month average of Price/GAAP earnings. The price labels show the actual peaks and troughs of valuation multiples)

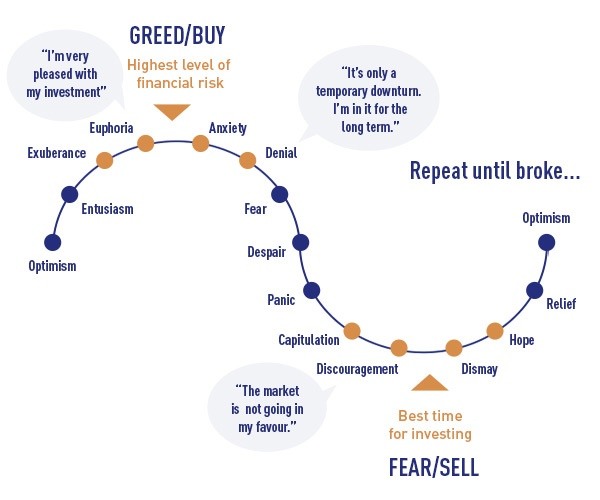

Recency Bias

The psychological phenomenon of performance chasing is a function of “recency bias.”

“Recency bias occurs when people more prominently recall, and extrapolate, recent events and believe that the same will continue indefinitely into the future. This phenomenon frequently occurs with investing. Humans have short memories in general, but memories are especially short when it comes to investing cycles.”

As Morningstar once penned:

“During a bull market, people tend to forget about bear markets. As far as human recent memory is concerned, the market should keep going up since it has been going up recently. Investors therefore keep buying stocks, feeling good about their prospects. Investors thereby increase risk taking and may not think about diversification or portfolio management prudence. Then a bear market hits, and rather than be prepared for it with shock absorbers in their portfolios, investors instead suffer a massive drop in their net worths and may sell out of stocks when the market is low. Selling low is, of course, not a good long-term investing strategy.”

The problem with chasing performance is that “what’s currently hot” becomes “what’s not.” Therefore, it is essential to recognize that what was at the top of the performance scale tends to fall towards the bottom with regularity. (Emerging markets, Small Cap, International, and Real Estate are notorious for big performance swings, a.k.a. volatility.)

Such was a point Jason Zweig made in his note:

“The more vivid and more recent the past performance is, the more likely it will feel to repeat. The manager of a fund with an annual return of 100% will seem to have some juju that someone who gained “only” 20% lacks. And a hot return in 2020 feels more likely to recur than a high return from, say, five years ago.”

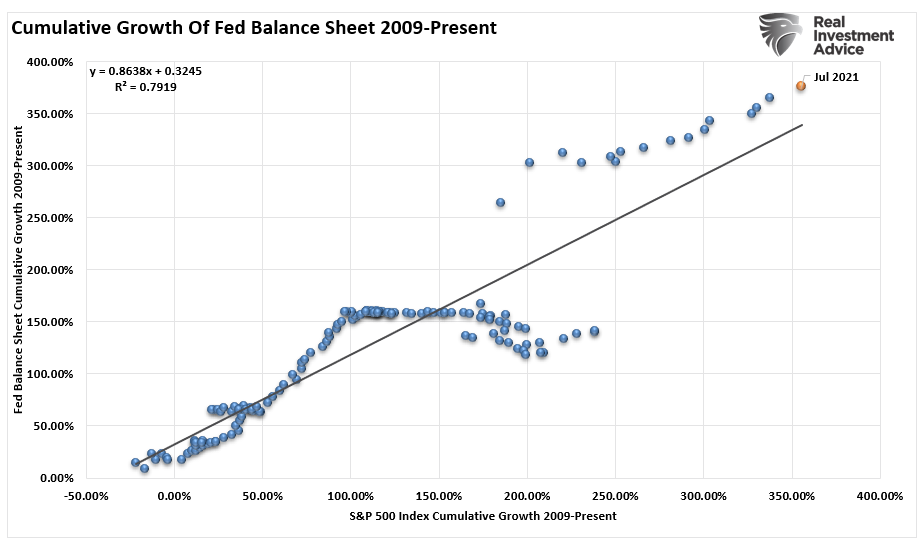

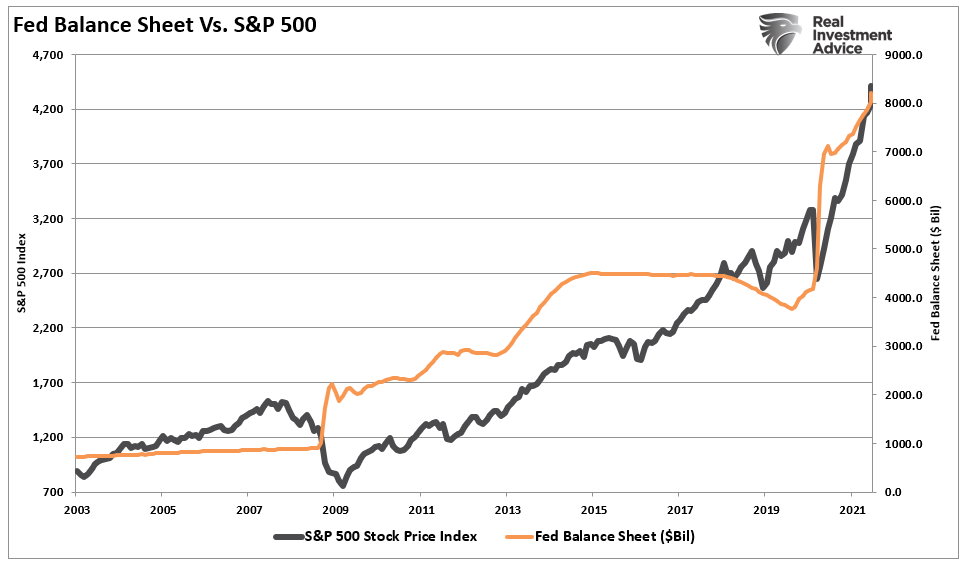

The Fed’s Performance Guarantee

So, why am I telling you all of this? Because we are once again at the point where individuals are chasing past returns. However, as I started in this missive, why shouldn’t they? With the Federal Reserve pumping in $120 billion a month in liquidity, “stocks have nowhere to go but up.” As I noted in “The Next Minsky Moment:”

“Given the high correlation between the financial markets and the Federal Reserve interventions, there is credence to Minsky’s theory. With an R-Square of nearly 80%, the Fed is clearly impacting financial markets.“

Those interventions, either direct or psychological, support the speculative excesses in the markets currently.

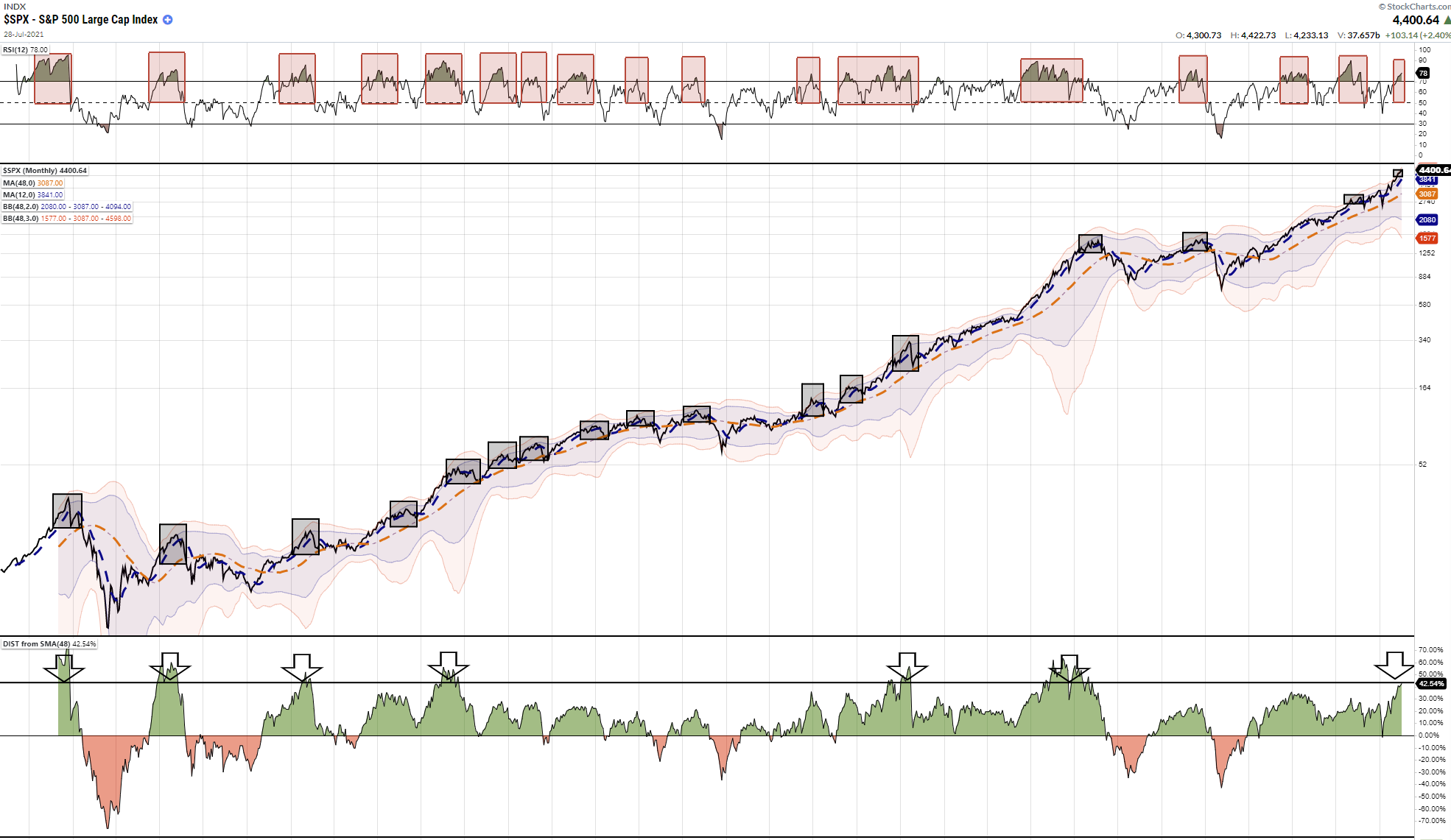

However, this is also where investors should be paying attention to the “risk” they are taking on. As shown, there are few points in history where the index, monthly, is this extended, deviated, and bullish.

However, as long as prices are advancing, then there is little reason to worry.

Until it changes, that is.

Hiding In Plain Sight

There are already warning signs that the current rally may be closer to its conclusion than not for investors. As noted yesterday, economic growth has likely peaked, and along with it, earnings growth as well. Revenue growth remains extremely weak, and the most significant risk is the Federal Reserve “tapering” monetary support.

There are clues “hiding in plain sight.”

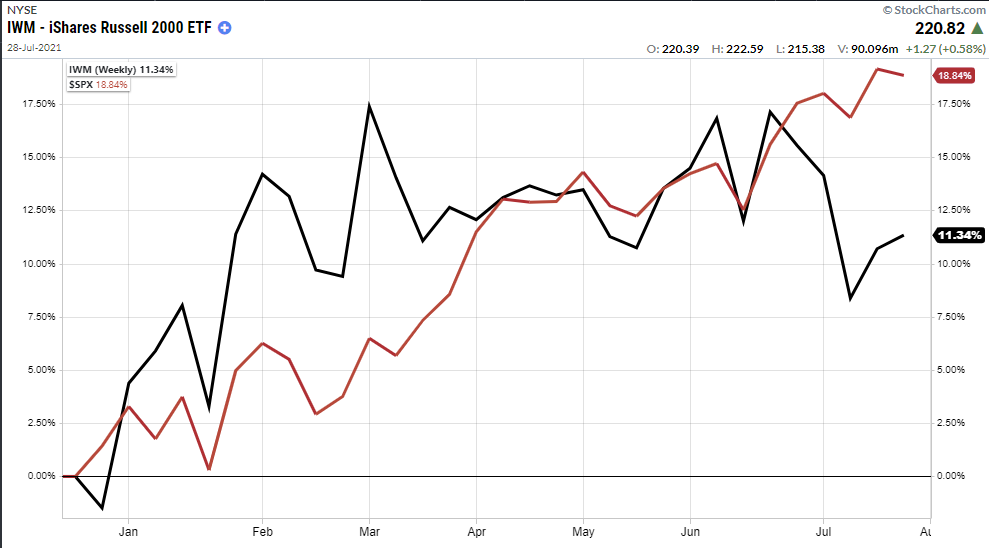

Typically in a bull market, as retail investors start making money in large-capitalization stocks, they shift to other areas to take on more risk. They generally shift to mid-capitalization companies and then to small-capitalization as markets become more saturated. As shown, over the last several months, the small and mid-capitalization indexes have begun to lose relative performance to large-cap stocks.

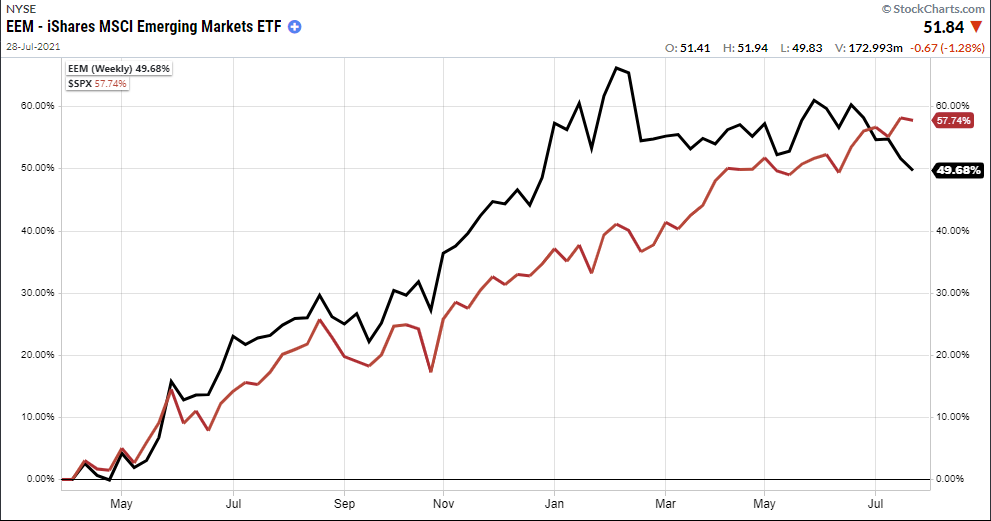

Another warning sign of “risk-off” behavior is the underperformance between large-cap stocks and emerging markets which tends to be the “poster-child” for risk preference.

These changes in “risk preference” are early warning signs. As such, the “bullish mania” can continue for some time. However, it is worth watching what is happening “below the surface,” particularly with bond yields, as a critical indicator for when it may be time to become “more bearish” in portfolio positioning.

Smart Money Beats LOLO.

It is usually the retail investor that is the “last in” and “last out” (LOLO) of the market. Performance chasing investors, also known a “bag holders,” are those that the “smart money” is often selling to as markets approach peaks. The financial media is of no help either.

It is a very conflicted system, and ultimately the retail investor is often left to their own devices. Unfortunately, a plethora of psychological behaviors, from confirmation bias to herding, eventually leads to poor outcomes.

While investors ultimately employ many rationalizations to justify “why this time is different,” what gets lost is that “what goes up, does indeed come down.”

“One of the main reasons investors earn disappointing returns over time is that vivid recent performance makes a fundamental property of finance harder to imagine. Extremely good — or bad — results are likely to be followed by outcomes closer to the long-term average. That’s regression to the mean, one of the most basic laws of finance. Nevertheless, vivid or recent results focus our attention on the past, not on the future where it belongs.

As soon as we see an extraordinarily unusual result, our minds immediately begin searching for a causal explanation.” – Jason Zweig

What it may seem that past performance is a guarantee, there are two essential things to remember.

- When you start, specifically at what valuation level, determines your eventual outcome.

- You don’t have 100-years to get “average returns.”

As soon as we come up with what seems like a plausible rationale, then the past performance automatically seems more likely to repeat. And remembering that results are likely to regress to the mean becomes almost impossible.” – Jason Zweig

Past performance is no guarantee.

Disclaimer: Click here to read the full disclaimer.

Thank you for sharing this information. Very interesting.

Good information. And always the thing to understand is that to sell one must have buyers willing and able to pay the price. This generally means selling before that peak, because at that point profit taking sales will start to push the price down. That is how the cycle works, it seldom works any other way. And those random unknowns always have effects, often negative ones.