Technically Speaking: Have "Tax Cuts" Been "Priced In" Already?

“Did you hear the news that was driving the markets to new records this morning?

No? Yeah, me either. But such is the nature of a speculative driven frenzy.”

Since the markets were closed yesterday, there is nothing to update from this past weekend’s newsletter.

While that missive was primarily directed at why “bond bears will likely be wrong again,” I did state the following about the market:

“That extension, combined with extreme overbought conditions on multiple levels, has historically not been met with the most optimistic of outcomes.

Importantly, such extensions have NEVER been resolved by a market that moved sideways. But, ‘exuberance’ of this type is not uncommon during a market ‘melt-up’ phase.

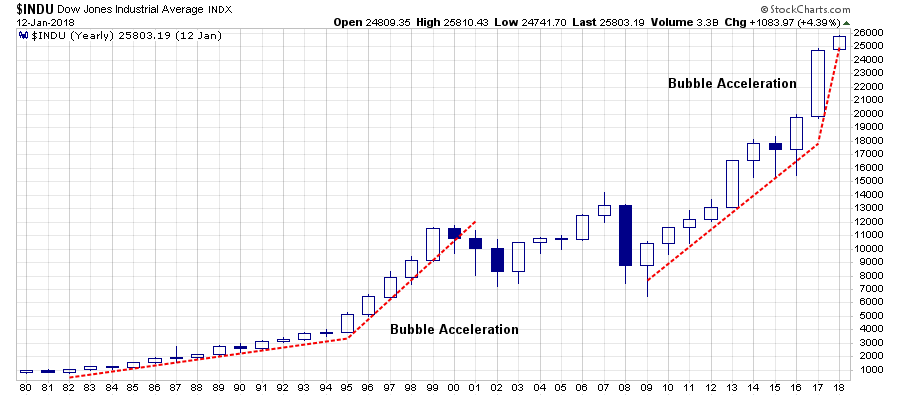

Nothing changed this past week as the “melt-up” phase gains momentum. We are on track currently to ratchet the both the fastest and most numerous sequential milestone advances for the Dow in history.

You can barely print ‘Dow 2X,000’ hats fast enough.”

Well, as the market opened this morning, the Dow and the S&P both set the fastest pace of a milestone advance in U.S. history as the Dow crested 26000 and the S&P touched 2800.

The surge in market exuberance in terms of both individual and professional investors is generally indicative of the “capitulation phase” of an advance which is when the last of the “holdouts” finally jump back into a market which “can seemingly never go down.”

From “QE” to “Low Rates Justify High Valuations” to “Tax Cuts,” the unfettered rise in asset prices has been underpinned by a shifting narrative backing bullish sentiment.

The latest, of course, is that “tax cuts” will boost bottom line earnings giving investors a reason to bid asset prices up further.

But have the markets already fully “priced in” the tax cuts even before they arrive?

It’s All About “Effective”

Just recently, Shawn Langlois penned an interesting article for MarketWatch:

“Zach Scheidt of the Daily Reckoning blog detailed his thoughts in a post Wednesday warning that anybody who’s investing based on these predictions is in for a big surprise as we move through 2018.

‘I’ve seen analysts make some bad calls before, but this one really takes the cake. Wall Street’s best and brightest are massively underestimating how much the new tax law will benefit companies’ bottom lines.”

As Shawn states, a company that posted $5.00 in pretax profits would have an after-tax profit of $3.25 in 2017. Under the new law, that after-tax profit would rise to $3.95 — a big 21% improvement.

I don’t disagree with the analysis at face value. However, there are two important issues that need to be addressed.

The first is the difference between the statutory rate of 35% versus the “effective” tax rate that corporations actually pay. This is crucially important and a point recently addressed by my partner, Michael Lebowitz:

“The statutory tax rate is the legally mandated rate at which corporate profits are taxed. As shown above, the rate has been consistent over the last 75 years except for one significant change as a result of the Tax Reform Act of 1986.

“The effective corporate tax rate is the actual tax rate companies’ pay. One can think of the statutory rate as similar to the MSRP sticker price on a new car. It provides guidance on cost but consumers always pay something less.

From 1947 to 1986 the statutory corporate tax rate was 49% and the effective tax rate averaged 36.4% for a difference of 12.6%. From 1987 to present, after the statutory tax rate was reduced to 39%, the effective rate has averaged 28.1%, 10.9% lower than the statutory rate.”

So, back to the math.

In reality, a company that earned $5.00 pretax only paid $1.41 in taxes in 2017 on average, leaving an after-tax profit of $3.59, and not $3.25. Under the new tax law that after-tax profit would come in at the $3.95 as stated in the article and the gain would be 10%, or half, of the gain the author forecasted.

There is a good bit of difference between a statutory increase of $0.70 profit per share the author assumed, versus the reality of $0.36 per share which is nearly a 50% reduction from the estimated benefit.

All Priced In

Secondly, investors didn’t just start estimating the impact of the “tax reform” bill when it was passed in December of 2017.

Far from it.

The rally that begins in November 2016 was the beginning of the “Trump Rally” in anticipation of regulatory reform, the repeal of the Affordable Care Act, infrastructure spending, and tax reform. It is worth noting that “tax reform” was the easiest of the four to calculate the beneficial impacts from passage. Therefore, a large portion of the post-election gains are reflective of those expected benefits.

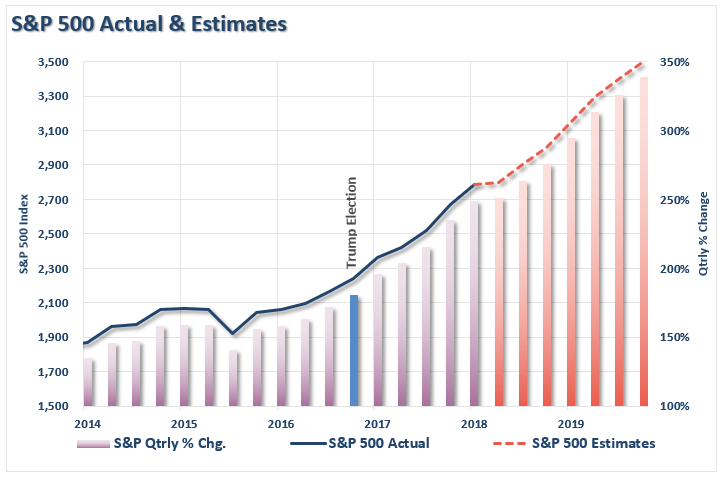

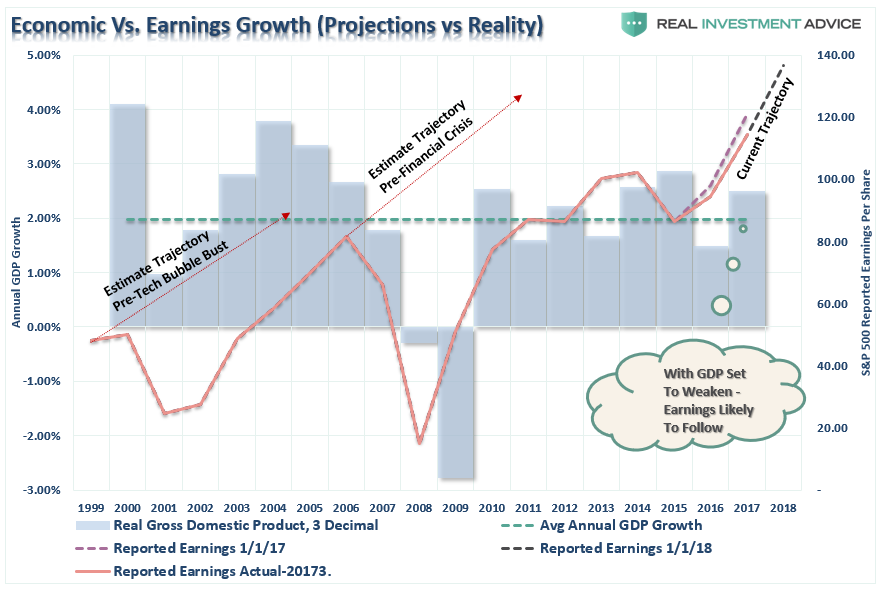

The chart below shows the S&P 500 from 2014 to present with Wall Street projections through 2020.

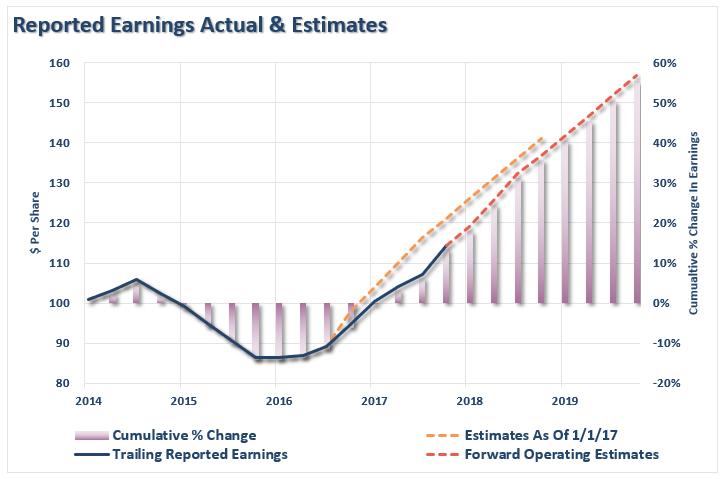

The rise in the index is not surprising given cheaper valuations following the “Financial Crisis” combined with more than $33 Trillion in monetary accommodations. Considering reported earnings were deeply negative in 2008, the initial recovery in earnings was quite strong. However, since 2014 earnings growth has been weaker. Despite, minimal growth since 2014, Wall Street believes currently that earnings will rise strongly through the end of this decade.

Just remember two things.

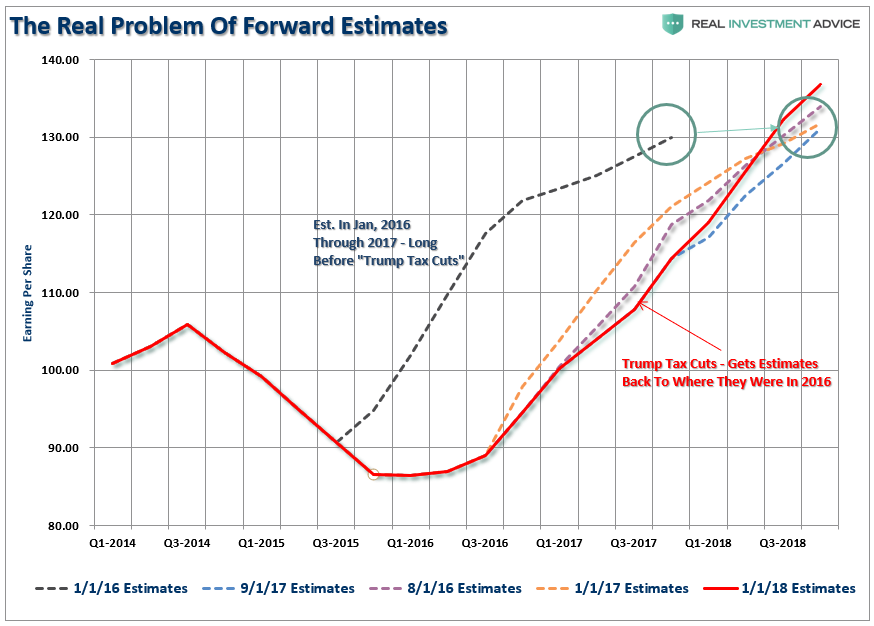

First, while asset prices have surged to record highs, reported earning, estimates for the S&P 500 through the end of 2018 are currently only slightly above where 2017 was expected to end in 2016. Wall Street ALWAYS over-estimates earnings and by about 33% on average. That overestimation provides a significant amount of headroom for Wall Street to be disappointed by year end, particularly once you factor in the “effective” rate issue noted above.

Secondly, Wall Street has never foreseen a recession or an earnings reversion until well after the fact.

It is quite likely that once again Wall Street is extrapolating the last few quarters of earnings growth ad infinitum and providing even more fodder for the market rally. It is also quite likely Wall Street will be proven wrong on earnings as so often has occurred in the past.

All Dressed Up

As I have addressed over the last few weeks, investors, both individual and professional, are overly exuberant and confident about the future of the market.

However, as I recently noted in “Bob Farrell’s 10-Investment Rules” – Rule #9 is pretty clear

“When all the experts and forecasts agree – something else is going to happen.”

Or even as Sam Stovall, the investment strategist for Standard & Poor’s once stated:

“If everybody’s optimistic, who is left to buy? If everybody’s pessimistic, who’s left to sell?”

Of course, Wall Street is notorious for missing the major turning of the markets and leaving investors scrambling for the exits.

This time will likely be no different.

Will tax reform accrue to the bottom lines of corporations? Most assuredly.

However, the bump in earnings growth will only last for one year. Then corporations will be back to year-over-year comparisons and will once again rely on cost-cutting, wage suppression, and stock buybacks to boost earnings to meet Wall Street’s expectations.

The risk of disappointment is extremely high.

Simply – the markets are “all dressed up with nowhere to go.”

Disclosure: The information contained in this article should not be construed as financial or investment advice on any subject matter. Streettalk Advisors, LLC expressly disclaims all liability in ...

more

While you are right that the tax reduction is priced in in terms of earnings per share after taxes, I don't see that you have factored in how the tax savings will also be used for additional stock buybacks, reducing the number of shares in the denominator and increasing the demand for shares. I also don't see how you've factored in how the income-tax cuts will increase before-tax earnings by increasing everyone's buying power. There are more dynamics at play, so I think the market has more room to run (even though I hate this tax plan).

Good read. Giving this article a bump on the homepage.