Technically Speaking: February Stats & Taking Action

In this past weekend’s newsletter, I discussed the two factors that saved the markets from breaking critical support and likely pushing the markets into a critical correction. To wit:

“The first is month-end window dressing by fund managers after a brutal start to the new year. After much liquidation, fund managers will need to rebalance holdings.

The second is the potential for Central Banks to intervene which could embolden the bulls as further support could temporarily delay the onset of a bear market and recession.

Not to be disappointed, the BOJ announced a move into NEGATIVE interest rate territory to try and boost economic growth in Japan.”

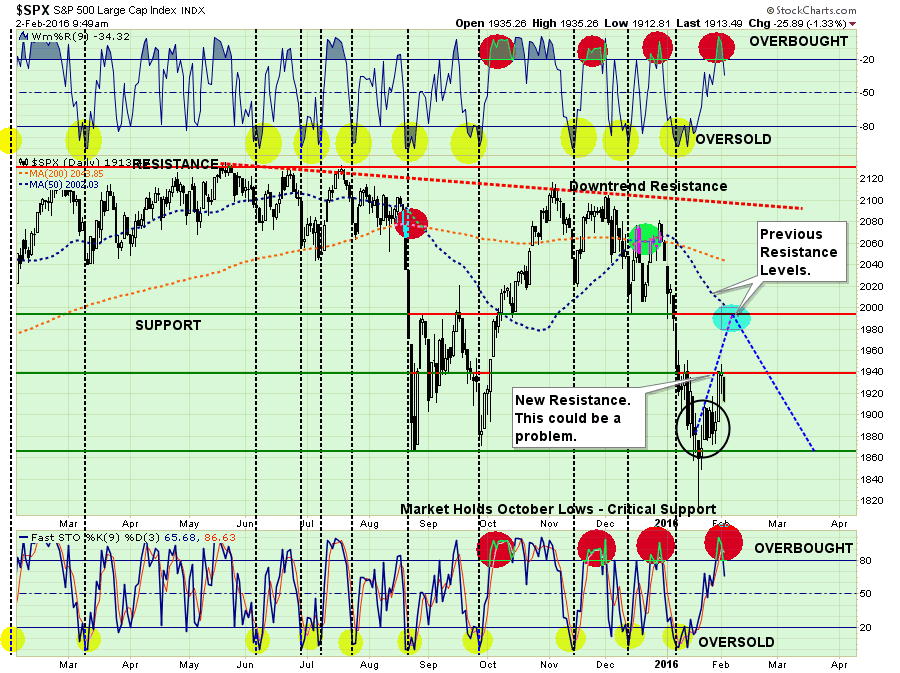

Those two factors pushed the markets higher on Friday, and as shown below, broke the markets out of the recent consolidation near critical support. That was the good news.

(Click on image to enlarge)

The bad news comes from the overbought / oversold indicators at the top and bottom of the chart. As I stated on Friday:

“The oversold condition that once existed has been completely exhausted due to the gyrations in the markets over the last couple of weeks. This leaves little ability for a significant rally from this point which makes a push above overhead resistance unlikely. Just as an oversold condition provides the necessary ‘fuel’ for an advance, the opposite is also true.”

The problem is that the market, as of this morning, appears to be failing at minor resistance. It is now critical that the markets hold previous lows or a more severe correction will likely take hold.

MORE BAD NEWS

In last week’s technical update I noted three potential reflexive rallies that should be used to rebalance equity risk into as follows:

“The chart below identifies the potential retracement levels of such a reflexive rally.

1970ish – Sell laggards and losers in portfolios.

2000ish – Trim back winners to target levels

2030ish – Be at final risk-adjusted allocations.”

(Click on image to enlarge)

NOTE: For conservative investors it is currently unlikely the market will rise much more than between 1970-1990 during this rally. I would do the majority of your portfolio rebalancing and risk reduction in this range.

Unfortunately, the 1970 level is likely no longer a viable option unless the market can reverse the decline and end the week higher than where it began. A failure to do so, by close of the market on Friday, will suggest more risk reduction actions must be taken in portfolios to preserve capital.

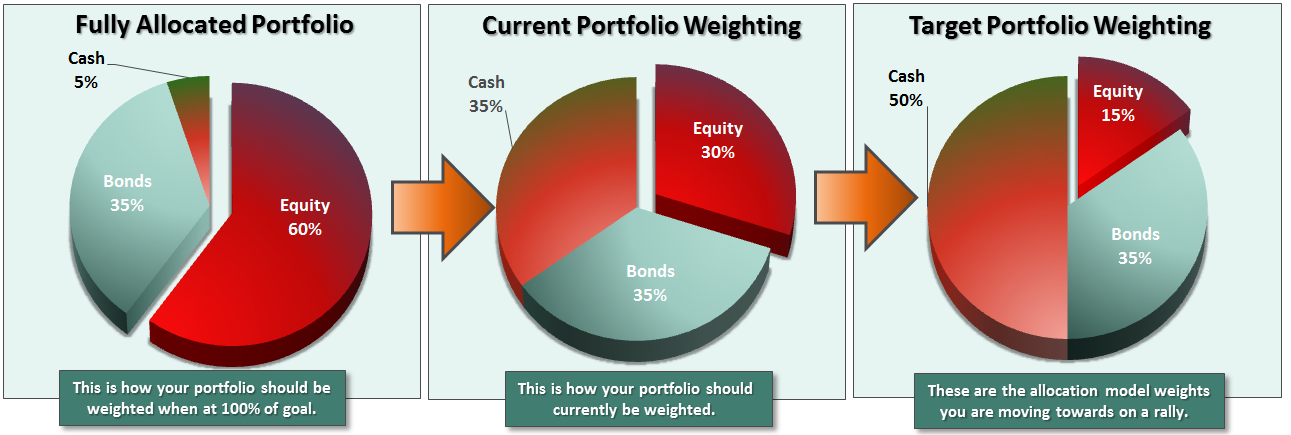

(Important Note: Portfolio allocation models have been at 50% exposure to equity since May of 2014. Further reductions would reduce the allocation model to 25% as shown below. For more information on the allocation model click here and scroll down to the 401k Plan Manager section.)

(Click on image to enlarge)

ANOTHER WARNING SIGN

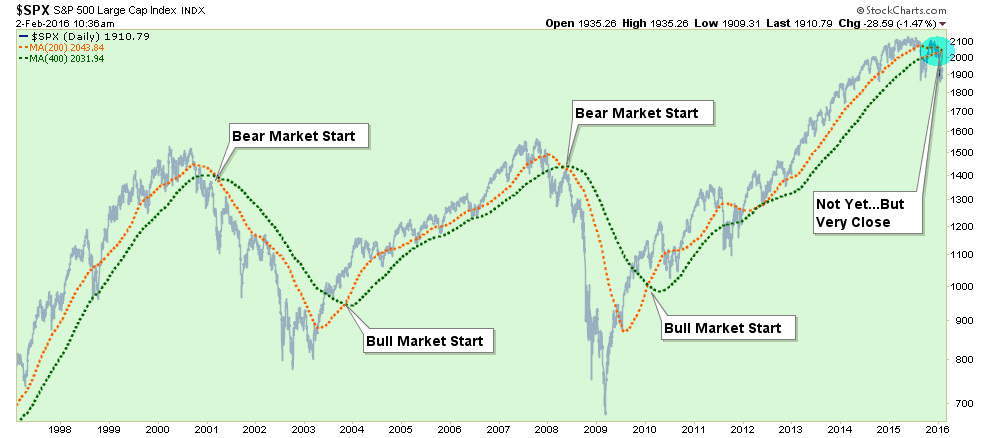

Furthermore, as shown in the chart below, another bit of technical data was brought to my attention just recently by a reader (HatTip RZ):

“Most identify the death cross as when the 50-day moving average breaks below the 200-day moving average on the S&P 500. However, the real death cross takes place when the 200-day moving average crosses below the 400. In 13 of the last 18 major correction episodes going back 1920- 72% this crossover marked the onset of a major Bear market.

In the five exceptions, which were 1953, 1990, 1984, 1987, and 1996, the same crossover actually ended the correction at that time. Importantly, these five episodes were during strongly trending SECULAR bull market cycles. Given we are not currently in one of those periods, it is likely a cross-over now would be more related to each of the market failures since the turn of the century.”

(Click on image to enlarge)

This cross-over WILL occur in next few weeks UNLESS the market can turn up sharply, break out to new highs and resume the bull market trend. Given the deterioration in the economic, fundamental and earnings backdrop, this seems highly unlikely currently.

FEBRUARY STATS AS AN ACTION GUIDE

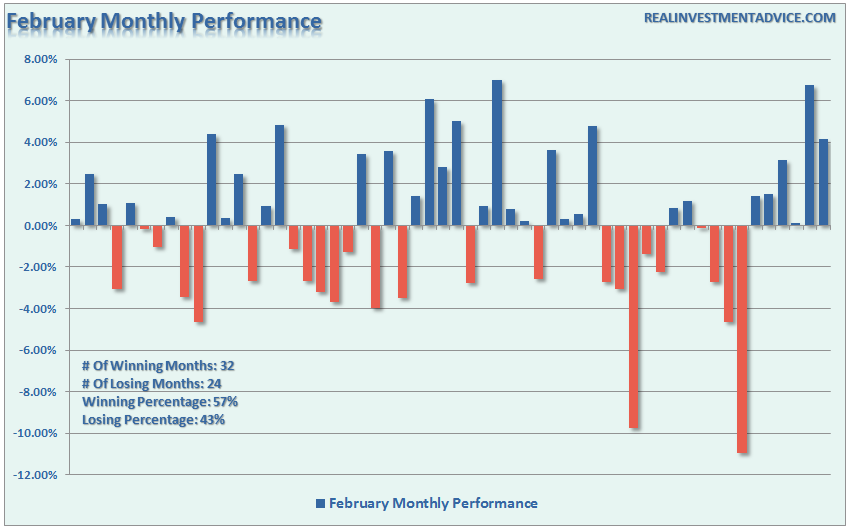

Last week, I took a look at the statistics of February months following poor performances in January. Statistically speaking, the odds are currently 70% that February will also end lower than where it began.

However, this week I want to dig into the month of February more deeply to see where the best opportunity to lighten exposure will most likely occur.

First, if we look at the month of February going back to 1960 we find that there is a slight bias to February ending positively 57% of the time.

(Click on image to enlarge)

Unfortunately, the declines in losing months have wiped out the gains in the positive months leaving the average return for February almost a draw (+.01%)

(Click on image to enlarge)

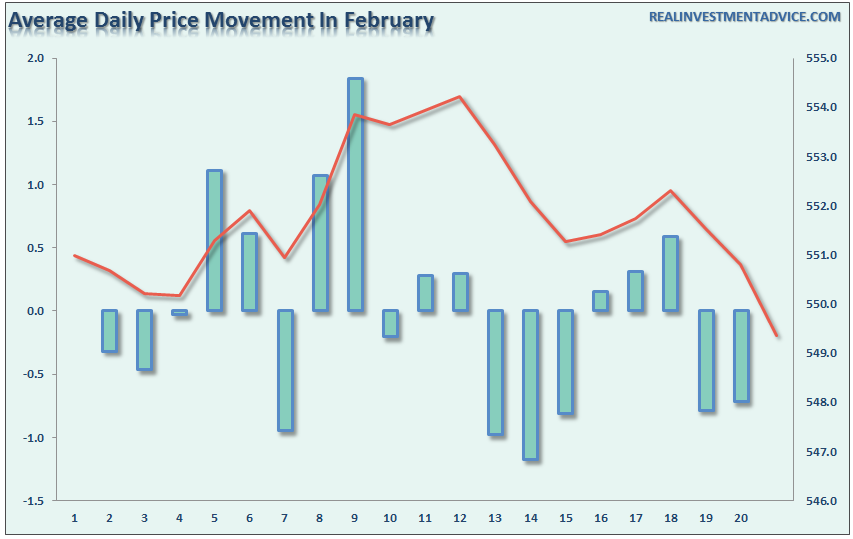

However, a look at daily price movements during the month, on average, reveal the 4th trading day of February through the 12th day are the best opportunity we will likely have to rebalance portfolio allocations and reduce overall portfolio risk.

(Click on image to enlarge)

SO, WHAT IF I’M WRONG?

Last week, I penned a piece on the problem with “Buy and Hold” investing. The crux of the article is that spending a bulk of your time making up lost gains is hardly a way to build wealth long-term. More importantly, is the consideration of “time” in that equation. Unless you discovered the secret of immortality, “long-term” is simply the amount of time between today and the day you will need your funds for retirement.

Of course, such articles always derive a good bit of push back suggesting that individuals can not effectively manage their own money, therefore, indexing is their only choice. I simply disagree.

Beginning last May, I suggested individuals reduce their portfolio risk to equities by 50%. According to the model I publish each week, that reduced equity to 30% in portfolios and raised cash to 35% and bonds remained at 35%. For simplicity sake, we are going to assume that cash yields nothing, bonds yield 2% and stocks equate to the S&P 500 on a capital appreciation basis only.

Since May, the S&P 500 has declined by 9.04%.

However, a portfolio allocated as described above declined by just 2.1%.

[35% Cash @ 0% + 35% Bonds @ 0.7% (2% X 35%) + Stocks @ -2.82% (-9.40% X 30%) = -2.1%]

Yes, managing risk still effectively lost money in the short-term, BUT much less than being overly exposed to equities during a period of decline.

Let’s assume that I am wrong in my current downside risk assessment and the markets reverses course and begins to rise strongly. The market will have to effectively hit all-time highs at this point just to break even with the current allocation model.

However, if the market does turn and re-establish the previous bullish trend, the allocation would likewise be adjusted to increase exposure to equities. The differential in performance currently gives a fairly substantial cushion in which to make non-emotional, logically based, investment decisions. Did you miss some of the gains? Sure. Does it matter? No.

But what if I am right?

If I am right, the preservation of capital will be far more beneficial. As I have stated previously, participating in the bull market over the last seven years is only one-half of the job. The other half is keeping those gains during the second half of the full market cycle.

If the market breaks critical support, the subsequent decline into a more corrective bear market will only widen the performance gap further. The purpose of risk management is to protect investment capital from destruction which has two very negative consequences.

First, when investment capital is destroyed, there is less capital to reinvest for future gains. The second, is the destruction of compounded returns. Small losses in principal can quickly erode years of gains in wealth.

Raising cash and protecting the gains you have accrued in recent years really should not be a tough decision. Not doing so should make you question your own discipline and whether “greed” is overriding your investment logic.

While the financial press is full of hope, optimism and advice that staying fully invested is the only way to win the long-term investing game; the reality is that most won’t live long enough to see that play out.

You can do better.

Disclosure: The information contained in this article should not be construed as financial or investment advice on any subject matter. Streettalk Advisors, LLC expressly disclaims all liability in ...

more

Nice Article. Do you always use the Fast Stoh settings? I ask as the Full Stohs are getting there but obviously not as fast as? Well the Fast setting of course. Just curious.