Technically Speaking: A Simple Method Of Risk Management

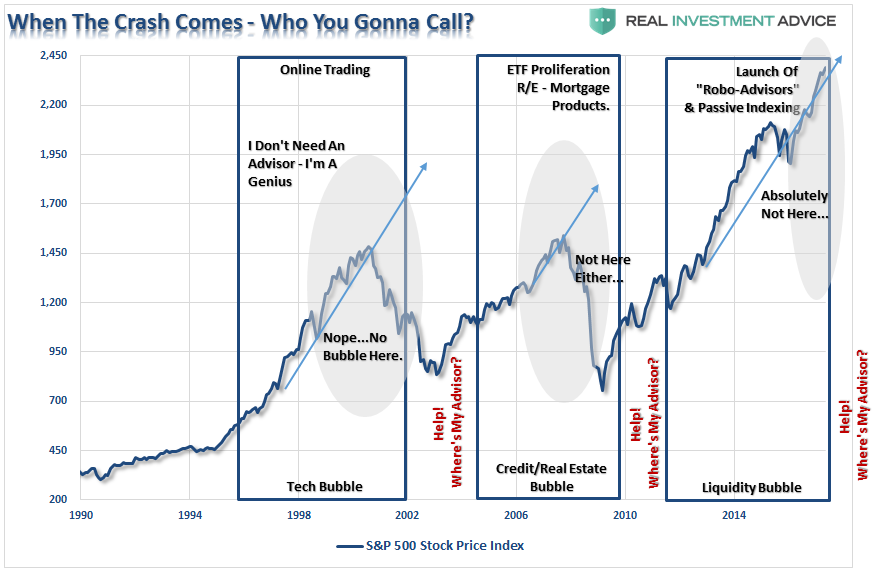

Yesterday, I addressed the issue of how market innovations and “crowding” into specific trades have been signs of market excesses in the past. To wit:

“That is the cycle of innovation in the financial marketplace. Despite the best of intentions, and advances in innovation, humans will always seek out the comfort of other humans in times of distress. The rising notoriety of Robo-advisors and the crowding of investors into ‘passive indexing’ are the current symbols of excess in the markets today. They will also be the ‘whipping boy’ of the next decline as ‘passive indexing’ is realized as a ‘foolish’ investment strategy.”

(Click on image to enlarge)

“I have been around long enough to see many things come and go in the financial world, and there is only one truth: ‘The more things change, the more they stay the same.'”

Just recently, Scott Nations via MarketWatch also made an interesting point with respect to the “psychological” influences that drive behaviors in the longer term:

“One problem investors face is the concept of the ‘anchor’ price, first described by Daniel Kahneman and Amos Tversky. Regardless of the value of a share of stock, we tend to believe that value must be close to the only bit of information many of us have — the current price. This anchoring effect makes it easier to justify paying a wildly inflated price for a company that is operating at a loss or for a market that is hugely overvalued by any objective measure.

Another common fallacy investors face is ‘herding,’ or the tendency to use the actions of others as a measure of sensible behavior. Fads, fashion, and stock-market bubbles are three examples of this mindset. When investors lose the sort of hard-nosed skepticism and difference of opinion that marks a healthy market, it becomes fashionable, and nearly unavoidable, for too many investors to buy too many stocks that have too little going for them.”

The psychology behind “market exuberance,” is an issue that has recurred with regularity in the financial markets and was always dismissed as “this time is different.” Unfortunately, for investors, it never was.

As Scott notes:

“If it were just psychological quirks that lead to runaway stock market rallies, the bubble might deflate itself slowly as the anchor price is gradually lowered and as financial fads and fashions change.

But the stock market isn’t a purely psychology exercise; too often the real world intrudes. Each modern stock-market crash has been precipitated by a catalyst that has little to do with finance and that catches us off guard. These catalysts push a system barely able to maintain equilibrium into chaos.”

Actually, it’s every time.

The market always “prices in” events or issues it is aware of such as economic data, earnings estimate changes, and even geopolitical events. In other words, it isn’t the thing that markets are aware of, but the unexpected event which sends traders, and algorithms, rushing for the exits. But, as Scott notes:

“And the raw material for a crash is a buoyant stock market.”

Despite the fact we know this is the issue and that such will happen again, according to the financial media, there is simply no way to avoid it, so we must simply “ride it out.”

Why?

Because we are told we can’t do better?

You Can Manage Your Risk

For years, the investment industry has tried to scare clients into staying fully invested in the stock market at all times,no matter how high stocks go or what’s going on in the economy. Investors are repeatedly warned that doing anything otherwise is simply foolish because “you can’t time the market.” As I noted yesterday, there is a reason for this:

“Wall Street firms, despite what the media advertising tells you, are businesses. As a business, their job is to develop and deliver products to investors in whatever form investor appetites demand…Wall Street is always happy to provide ‘products’ to the consumers they serve.

As Wall Street quickly figured out that it was far more lucrative to collect ongoing fees rather than a one-time trading commission…The mutual fund business was booming, and business was ‘brisk’ on Wall Street as profits surged.”

Here is the interesting question as I noted in “Spot What’s Missing.”

“Every day the media continues to push the narrative of passive investing, indexing and ‘buy and hold.’ Yet while these methods are good for Wall Street, as it keeps your money invested at all times for a fee, it is not necessarily good for your future investment outcomes.

You will notice that not one of the investing greats in history ever had ‘buy and hold’ as a rule.

So, the next time that someone tells you the ‘only way to invest’ is to buy and index and just hold on for the long-term, you just might want to ask yourself what would a ‘great investor’ actually do. More importantly, you should ask yourself, or the person telling you, ‘WHY?’”

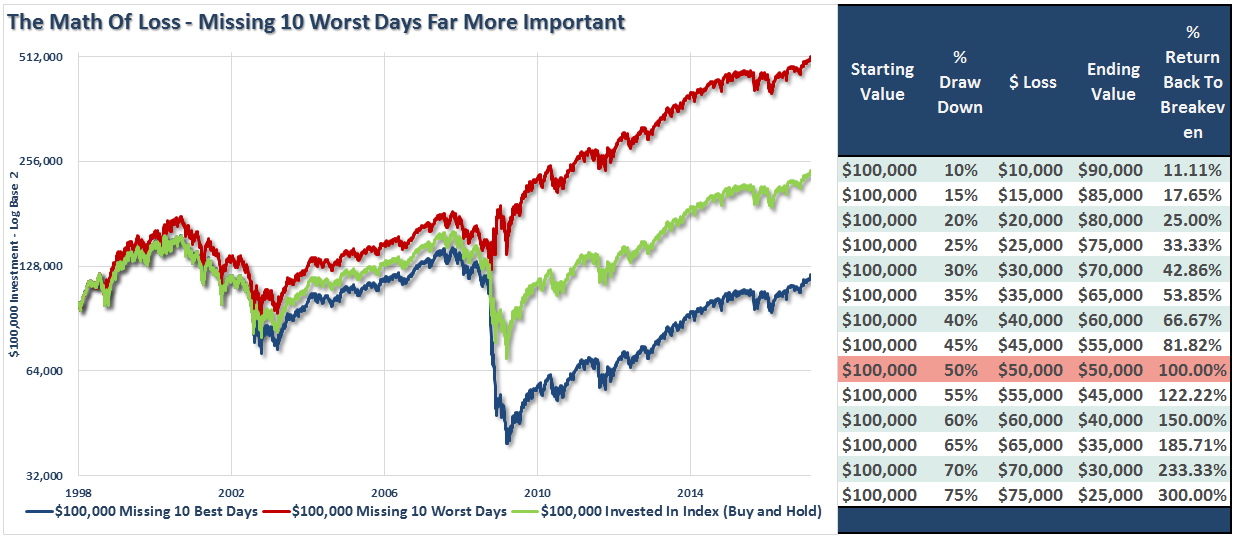

The reason is simple, “getting back to even” is not an investment strategy.

(Click on image to enlarge)

Every great investor has one facet of their investment discipline in common – loss avoidance. Why? Because avoiding major drawdowns in the market is key to long-term investment success. If I am not spending the bulk of my time making up previous losses in my portfolio, I spend more time compounding my invested dollars towards my long term goals.

The reason that the finance industry doesn’t tell you this is because it is NOT PROFITABLE for them. The finance industry makes money when you are invested – not when you are in cash.Therefore, it is of no benefit to Wall Street to advise you to move to cash.

A Simple Method Of Risk Management

Now, let me be clear. I am discussing “market timing” which is specifically being “all in” or “all out” of the market at any given time. The problem with trying to time the market is consistency. Being all in, or out, of the market will eventually put you on the wrong side of the ‘trade’ which will lead to a host of other problems.

As I stated, there are no great investors of our time that “buy and hold” investments. Even the great Warren Buffett occasionally sells investments. (He just recently sold almost his entire stake in Walmart and IBM) True investors buy when they see value, and sell when value no longer exists.

While there are many sophisticated methods of handling risk within a portfolio, even using a basic method of price analysis, such as a moving average crossover, can be a valuable tool over the long term holding periods.

Will such a method ALWAYS be right? Absolutely not.

Will such a method keep you from losing large amounts of capital? Absolutely.

The chart below shows a simple moving average crossover study. The actual moving averages used are not important, but what is clear is that using a basic form of price movement analysis can provide a useful identification of periods when portfolio risk should be REDUCED. Importantly, I did not say risk should be eliminated; just reduced.

(Click on image to enlarge)

Again, I am not implying, suggesting or stating that such signals mean going 100% to cash. What I am suggesting is that when “sell signals” are given that is the time when individuals should perform some basic portfolio risk management such as:

- Trim back winning positions to original portfolio weights: Investment Rule: Let Winners Run

- Sell positions that simply are not working (if the position was not working in a rising market, it likely won’t in a declining market.) Investment Rule: Cut Losers Short

- Hold the cash raised from these activities until the next buying opportunity occurs. Investment Rule: Buy Low

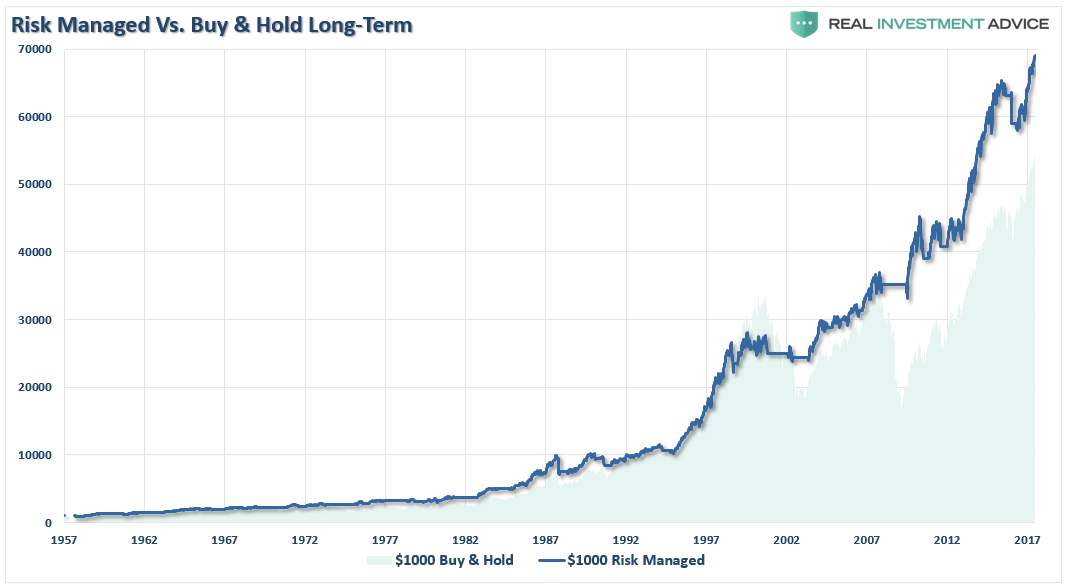

By using some measures, fundamental or technical, to reduce portfolio risk by taking profits as prices/valuations rise, or vice versa, the long-term results of avoiding periods of severe capital loss will outweigh missed short term gains. Small adjustments can have a significant impact over the long run.

This is shown in the chart below. There is always a big difference between market prices and the impact of losses on an actual dollar-based portfolio. Buy using a simple method to avoid losses, the differential over the long-term on $1000 is quite significant. (Chart below is capitalization only for example purposes.)

(Click on image to enlarge)

As shown in the chart above, this method doesn’t avoid every little twist and turn of the market. But what it does do is help avoid a bulk of the major market reversions. While it may not be possible to “time” the market, it is possible to reach intelligent conclusions about whether the market offers good value for investors on a risk/reward basis.

Yet, despite two major bear market declines, it never ceases to amaze me that investors still believe that somehow they can invest in a portfolio that will capture all of the upside of the market but will protect them from the losses. Despite being a totally unrealistic objective this “fantasy” leads to excessive risk taking in portfolios which ultimately leads to catastrophic losses. Aligning expectations with reality is the key to building a successful portfolio. Implementing a strong investment discipline, and applying risk management, is what leads to the achievement of those expectations.

Conclusion

There are many half-truths perpetrated on individuals by Wall Street to sell product, gain assets, etc. However, if individuals took a moment to think about it, the illogic of many of these arguments are readily apparent.

Chasing an arbitrary index that is 100% invested in the equity market requires you to take on far more risk that you realize. Two massive bear markets over the last decade have left many individuals further away from retirement than they ever imagined. Furthermore, all investors lost something far more valuable than money – TIME needed to achieve their goal.

To win the long-term investing game, your portfolio should be built around the things that matter most to you.

- Capital preservation

- A rate of return sufficient to keep pace with the rate of inflation.

- Expectations based on realistic objectives.(The market does not compound at 8%, 6% or 4% every year, losses matter)

- Higher rates of return require an exponential increase in the underlying risk profile. This tends to not work out well.

- You can replace lost capital – but you can’t replace lost time. Time is a precious commodity that you cannot afford to waste.

- Portfolios are time-frame specific. If you have a 5-years to retirement but build a portfolio with a 20-year time horizon (taking on more risk) the results will likely be disastrous.

The index is a mythical creature, like the Unicorn, and chasing it has historically led to disappointment. Investing is not a competition, and there are horrid consequences for treating it as such.

In hindsight, it is easy to see that investors should have been out of the market in 2001 and 2008. However, remember just prior to those two major market peaks the Wall Street mantra was the same then, as it is today:

“This time is different.”

Disclosure: The information contained in this article should not be construed as financial or investment advice on any subject matter. Streettalk Advisors, LLC expressly disclaims all liability in ...

more

thanks