Fundamental Forecast for the S&P 500: Bearish

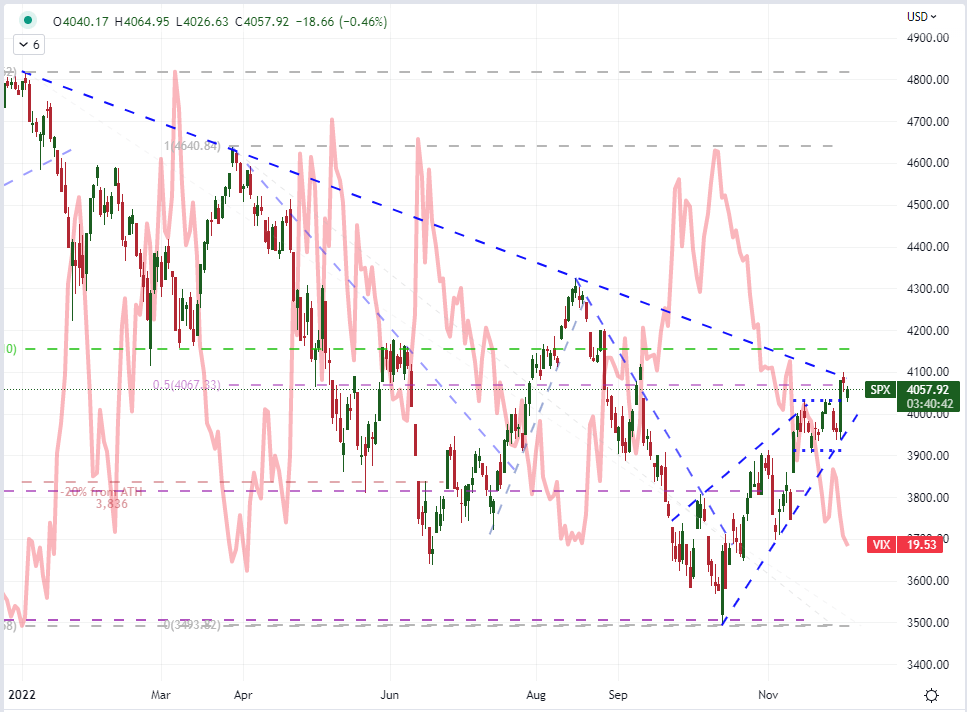

US equity indices made a considerable effort to revive the choppy bullish trend from mid-October this past week and investors attempted to draw on the fervor of a cooling monetary policy regime from the Fed. The spark that caught for bulls initially were the comments from Chairman Jerome Powell in which he attempted to balance expectations by saying that a reduction in the pace of tightening was ahead while also warning that the ultimate peak rate (also referred to as the ‘terminal rate’) would be higher than previously expected. While neither reference was particularly new from the central bank’s forward guidance efforts these past months, the markets ran initially on the tempo reference with Dow pushing to a technical ‘bull market’ (20 percent from structural lows) while the S&P 500 advanced above its 200-day moving average for the first time since April. Yet, the enthusiasm this would suggest was quickly called into question when the Fed’s favorite inflation indicator (PCE deflator) didn’t rouse any follow through despite its cooling and an NFPs beat ultimately knocked the market back. What could have been a clear course for bulls on a coasting ‘rates are slowing’ theme, will now be a mess of nuance. With the Fed in its pre-FOMC meeting blackout period and unable to direct expectations while the actual decision is further ahead out on December 14th, doubt will be a prominent feature of the landscape. And, don’t forget that we are also contemplating the possibility and timing of a recession. Events like the ISM service sector activity report on Monday and UofM consumer sentiment survey on Friday will prod at this concern.

Chart of S&P 500 Overlaid with VIX Volatility Index (Daily)

(Click on image to enlarge)

Chart Created on Tradingview Platform

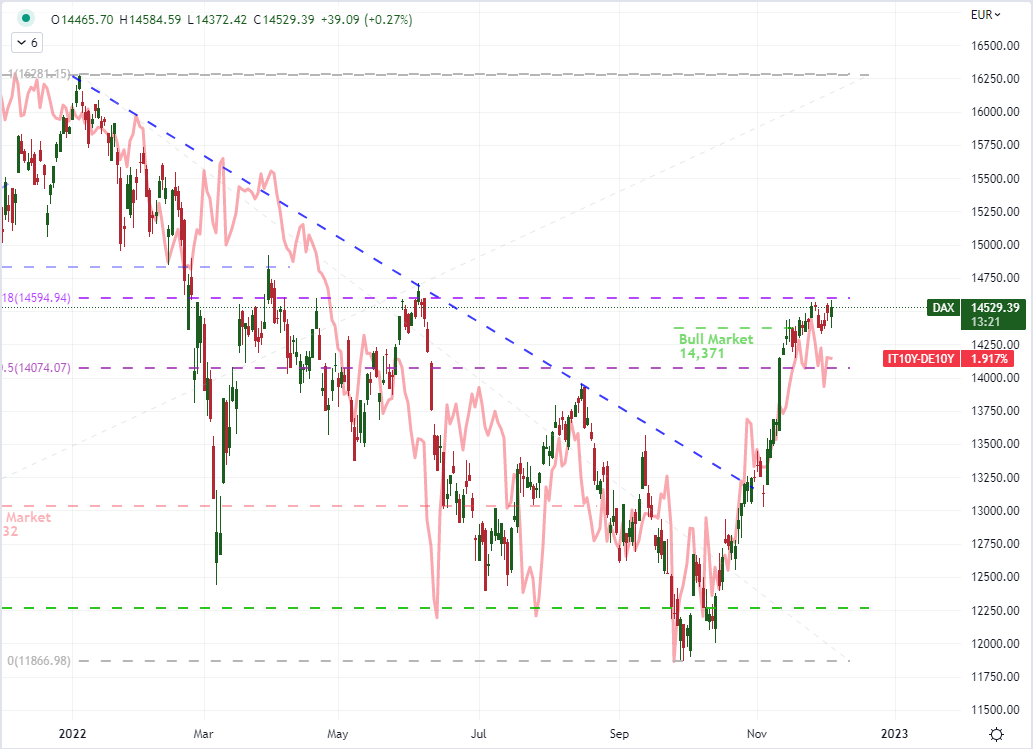

Fundamental Forecast for the DAX 40: Bearish

Similar to its Dow Jones Industrial Average counterpart in the US, the German DAX 40 index has managed to return to a technical ‘bull market’ – though it managed this feat weeks before its peer. For fundamental motivation behind Europe’s largest economy, there is the familiar draw of recovery mentality across global equities that seems more heavily based in speculative appetite than genuine fundamental inspiration. In Europe, the onset of winter will bring about the concern over energy prices and shortages that has long been warned by officials. With Brent oil still trading at more than a $5 per barrel premium to the WTI standard in the US and the EU agreeing to cap Russian oil exports to $60, economic pain will be pressed. Of further economic concern is the anticipation for the ECB amid calls from the OECD and inflation hawks to close the interest rate gap with the Federal Reserve. There is an ECB rate decision on December 15th – the day after the Fed’s meeting – which will lend itself to just as much anticipation and potentially fear. Given the premium given back to the markets from its 2022 lows, a lack of information will increasingly play to concern rather than optimism. It is worth keeping tabs on economic pressure measures, one of which I include below: an inverted Italian-German 10-year yield spread.

Chart of DAX 40 Overlaid with the Italian-German 10-Year Yield Differential (Daily)

(Click on image to enlarge)

Chart Created on Tradingview Platform

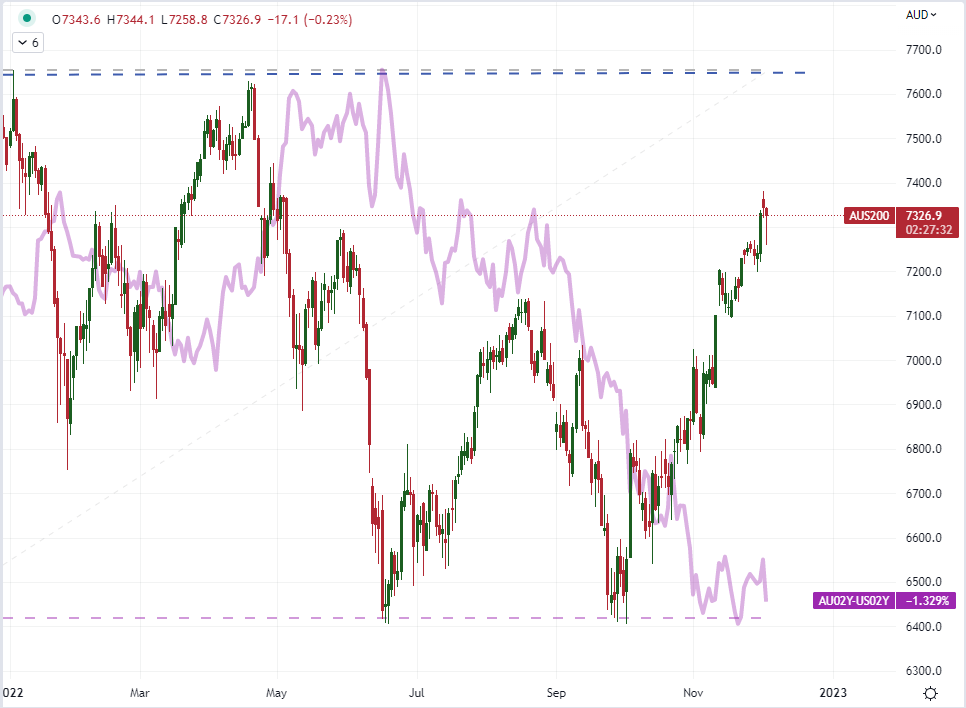

Fundamental Forecast for the ASX200: Neutral

Where anticipation will be a big part of the US and European fundamental landscape next week, there will be direct catalysts on offer for the Australian market. The ASX 200 managed to escape the official ‘bear market’ (20 percent correction from record or structural highs) that so many of its counterparts suffered, and it subsequently recovered from its shallow double bottom at the 38.2 percent Fib retracement of the post-pandemic recovery run down around 6,400. Now within only 4 percent of returning to record highs, we are facing a direct look at both the health of the Aussie economy and the level of restriction (and return) on the financial system with an RBA rate decision – among other data. The central bank decision is up first on Tuesday morning and expected to deliver a further 25bp hike which would push the benchmark to 3.10 percent. That is will be a throttle to economic activity, but it is a deceleration that would lend itself to be a lower peak yield than many of its global counterparts (such as the FOMC which has a current 4.00 percent rate and is seen peaking above 5.00 percent next year). While that can be favorable for activity, it can also curb speculative flows that are looking for a higher yield. If the 3Q GDP disappoints – it’s expected to only slightly cool quarter-over-quarter from 0.9 to 0.8 percent – it could present a bigger fundamental issue.

Chart of ASX 200 Overlaid Australian-US 2-Year Yield Differential (Daily)

(Click on image to enlarge)

Chart Created on Tradingview Platform

More By This Author:

EUR/USD Consolidates Above Psychological 1.0500 Level; Further Gains In Store?

USD/JPY Update: BoJ And Fed Chair Powell’s Comments Form Perfect Cocktail For Yen Gains

Crude Oil Rises A Third Day From 76 Support As Risk Appetite Adds To Supply Data

Comments

Log in or sign up to join the conversation.