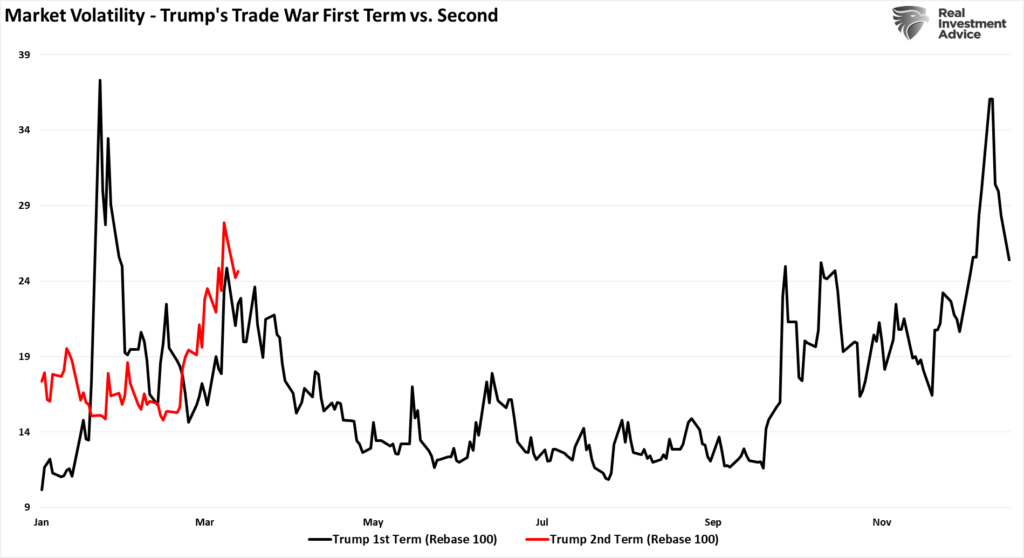

Market Volatility Spikes

Last week, we discussed that the market continues to track Trump’s first Presidential term as he launched a trade war with China.

“However, despite the deep levels of negativity, the current correction is well within the context of the volatility seen during Trump’s first term as he engaged in a trade with China.”

(Click on image to enlarge)

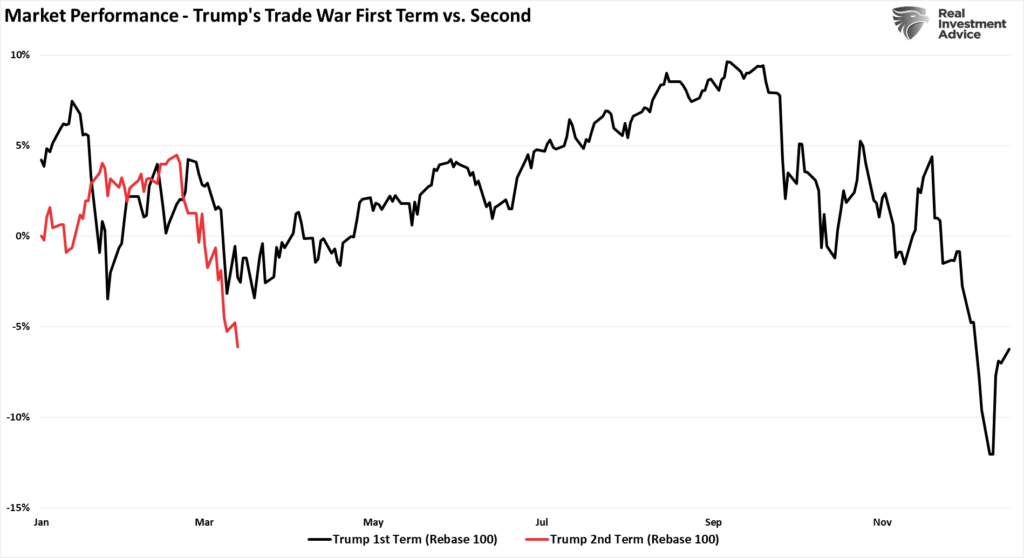

Overall market performance is also tracking closely to President Trump’s first term as Wall Street tries to assess the impact of tariffs on earnings. The markets will complete that assessment soon, and they will rally once the outlook becomes firmer.

(Click on image to enlarge)

While Trump’s tariffs and bearish headlines currently dominate investors’ psychology, we must remember that corrections are a normal market function. Yes, the market is down roughly 9% from the peak, but we have seen these corrections repeatedly in the past. That does NOT mean a more extensive corrective process is not potentially in process. It only implies that markets are likely in a position for a technical rally to reverse the more extreme oversold conditions. As shown, the MACD and relative strength are currently at levels not seen since the October 2022 lows. Furthermore, the market has completed a 23.6% retracement of the rally from those lows, providing the support needed for a rally.

(Click on image to enlarge)

Let me be clear. I am not saying the markets have bottomed, and the next move is back to all-time highs. While that could be the case, other technical warnings suggest we could be in for a longer corrective/consolidative process. As such, we recommend using rallies to rebalance portfolios, reduce risk and leverage, and increase cash levels slightly until the markets confirm the bullish trend is re-established.

This correction process has been painful. However, it is crucial to remember how you felt during previous corrections and what actions you took. Were they the correct actions? If they weren’t, then avoid potentially repeating past mistakes.

Volatility is the price we pay to invest. The hard part is avoiding volatility’s behavioral impacts on our investing outcomes.

Need Help With Your Investing Strategy?

Are you looking for complete financial, insurance, and estate planning? Need a risk-managed portfolio management strategy to grow and protect your savings? Whatever your needs are, we are here to help.

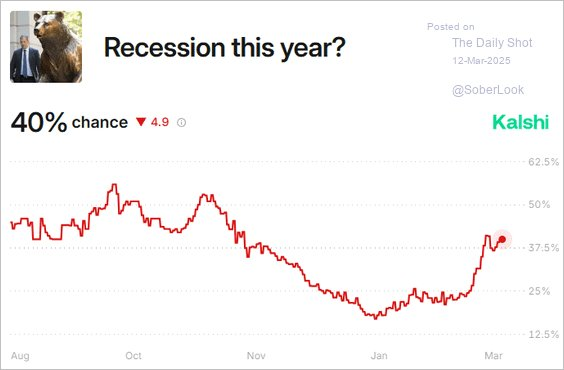

Sell Off Accelerates As Recession Fears Emerge

Over the last couple of weeks, the market sell off eclipsed 9% on an intraday basis, sending investor sentiment plummeting to levels usually seen during more significant declines and previous bear markets. While the markets have had a phenomenal run over the past two years, investors seemed to have forgotten that markets tend to correct now and then.

The one thing you can always count on during the midst of a sell off is the media trying to formulate a headline to rationalize investor actions. During this particular decline, it was the return of a recession.

Of course, it is wise to remember that in 2022, we had the most anticipated recession ever, which failed to occur and preceded one of the strongest bull markets in recent history.

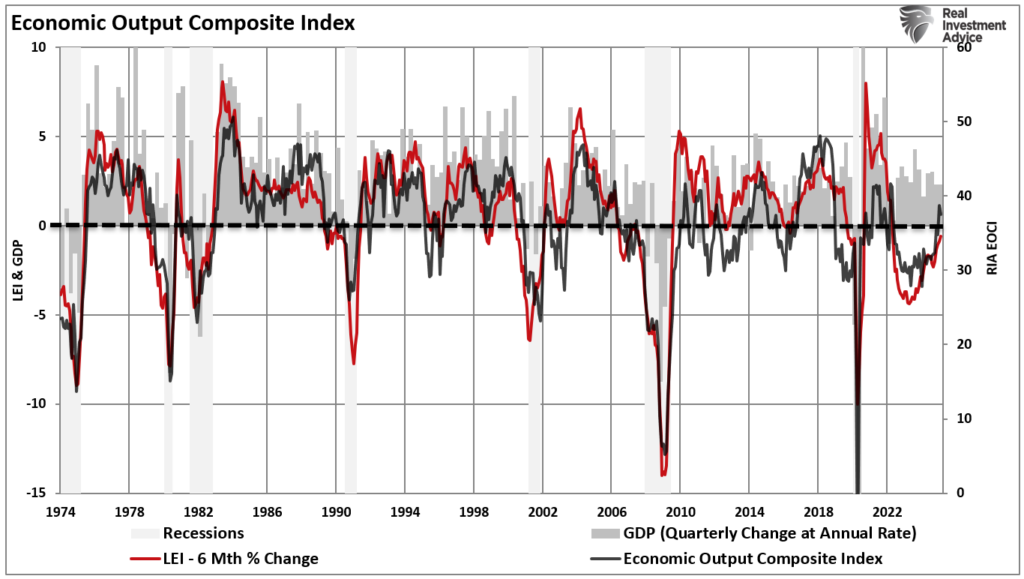

Is this time different? Maybe. However, few indicators suggest a recession is on the horizon. The Economic Composite Index (a comprehensive measure of economic activity comprised of more than 100 data points) is in expansionary territory. The EOCI index confirms the improvement in the 6-month rate of change in the Leading Economic Index (LEI), one of the best recession indicators, and current levels of economic growth. While economic growth will undoubtedly slow as all of the excess governmental spending under the previous Administration reverses, there is currently no recession warning in the data. That does not mean that such can not change in the future. However, for now, the risk of recession is extremely low.

(Click on image to enlarge)

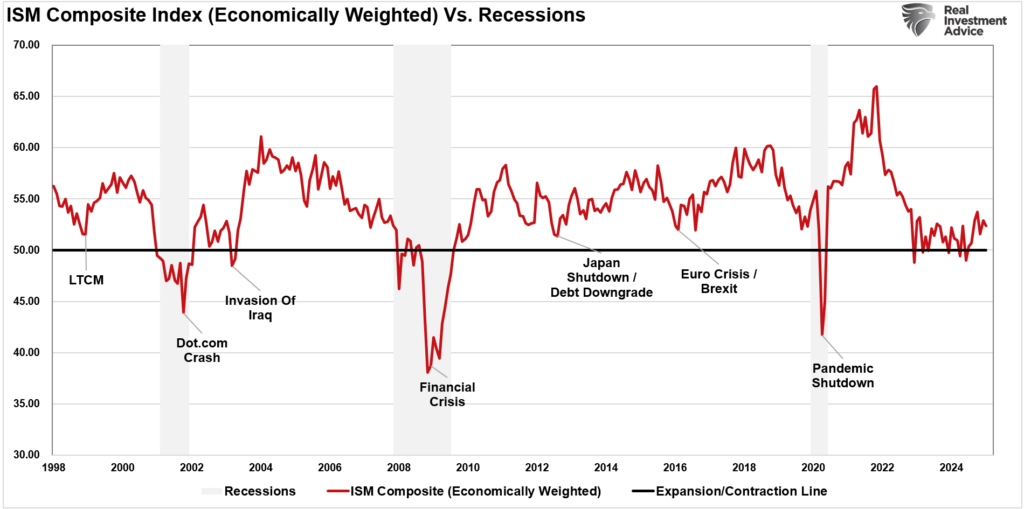

Adding to that analysis, the economically weighted ISM composite index is also in expansionary territory, suggesting a slower economic growth rate but no current risk of recession.

(Click on image to enlarge)

Yes, as we have discussed many times, there are reasons to expect the economy to continue to slow down. However, a slower growth environment is far different from a recession.

Does that mean we can not have a recession? No. I am only suggesting that the current weight of evidence suggests slower growth, not negative growth.

With that said, there are certainly implications for slower economic growth, primarily the change to the main driver of financial markets: earnings.

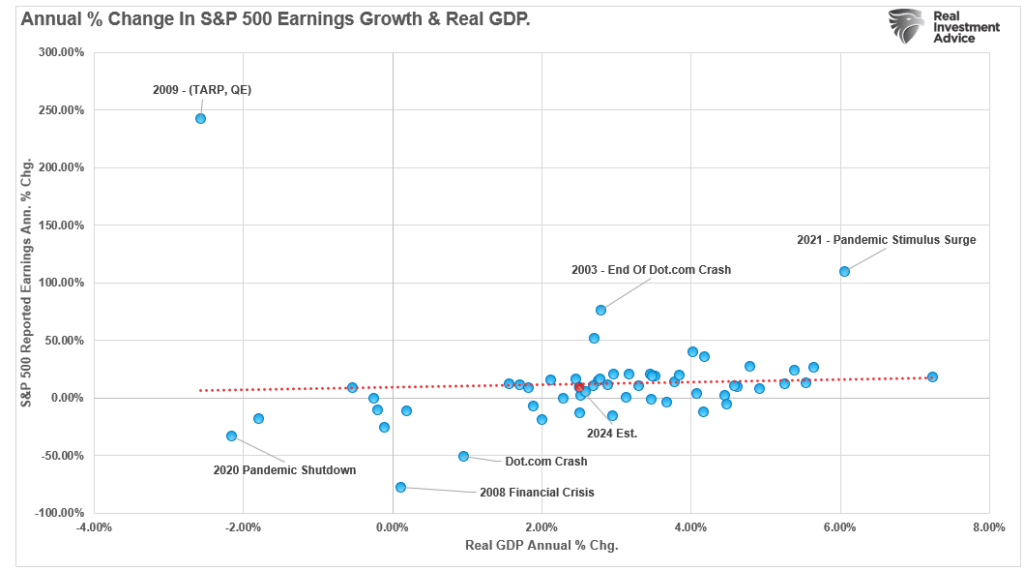

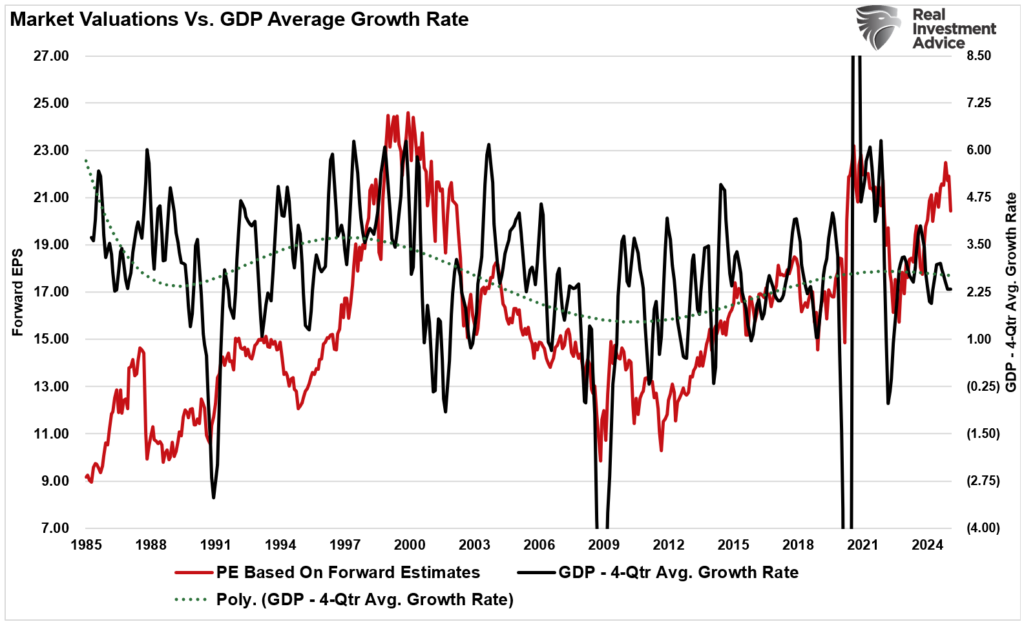

A better way to visualize this data is to look at the correlation between the annual change in earnings growth and inflation-adjusted GDP. There are periods when earnings deviate from underlying economic activity. However, those periods are due to pre- or post-recession earnings fluctuations. Economic and earnings growth are very close to the long-term correlation, but a slowdown will change that.

(Click on image to enlarge)

As such, given the high correlation between the market and the corporate profits to GDP ratio, as is currently the case, markets can detach from underlying economic realities due to momentum and psychology for brief periods. However, those deviations are unsustainable in the long term, and corporate profitability, as discussed, is derived from underlying economic activity.

(Click on image to enlarge)

Such is what has been happening over the past couple of weeks.

A Repricing Of Valuations

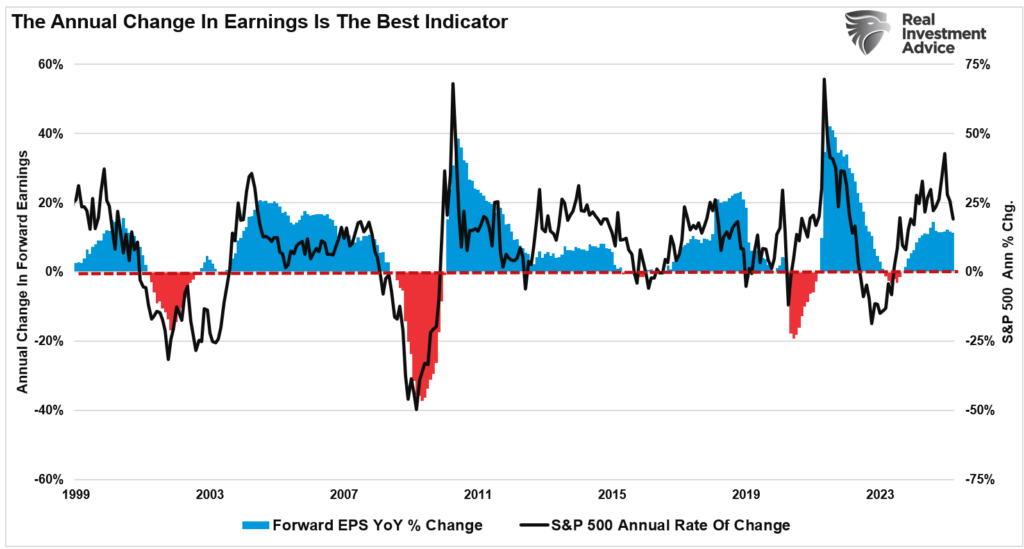

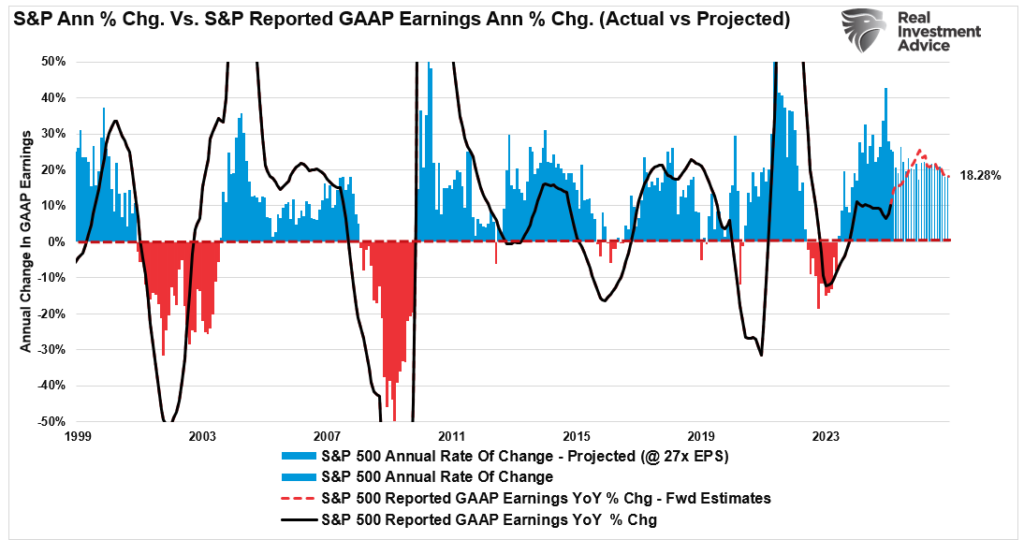

While media headlines were quick to jump on “recession” headlines, the reality, as shown below, was that the recent sell off was realigning overly bullish markets for future earnings growth. The deviation of the annual rate of change of the market from the rate of change of forward earnings was quite significant.

(Click on image to enlarge)

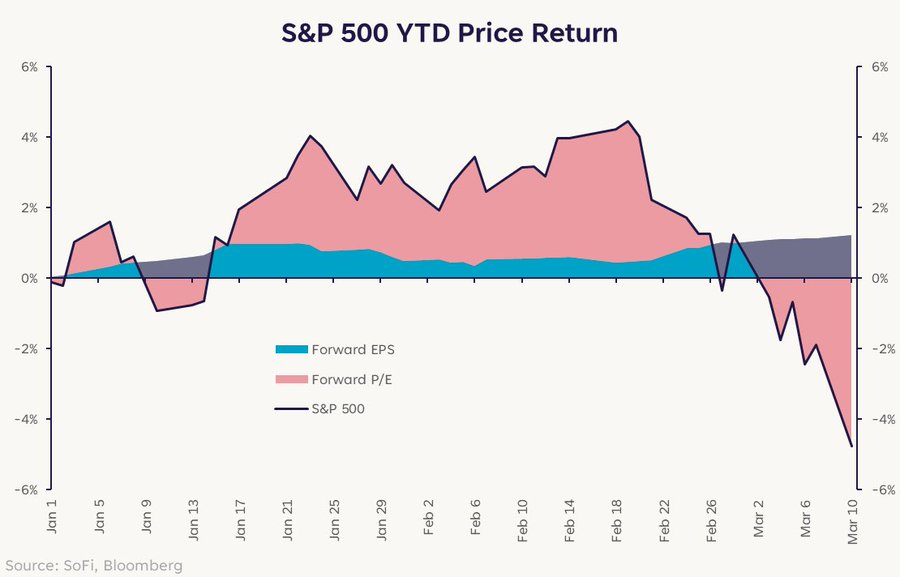

However, the sell-off has not resulted from a sharp decline in expected earnings growth, which would be a byproduct of a recession. Instead, it has been a reduction in valuations to align with expected earnings.

(Click on image to enlarge)

As noted just a few weeks ago, the recent sell off and the repricing of valuations were not unexpected.

“We see the same deviation between the annual rate of change of the S&P 500 versus actual reported earnings. As shown below, there was a sharp expansion in the market’s price without an equally substantial increase in underlying earnings per share. Such resulted in a dramatic rise in multiple expansions over the last two years. Analysts must increase their “manufactured” estimates to justify those elevated valuations and catch up with the market’s price. However, it is more likely that the growth rate of equity prices will slow substantially to allow earnings to catch up with valuations.”

(Click on image to enlarge)

While the daily headlines of tariffs and spending cuts are certainly weighing on investor psychology, earnings expectations remain the biggest driver of the market. As noted above, given that previous valuations exceeded the economy’s ability to generate the required earnings, the recent sell off is a healthy process. There is still more work to be done for the market to reach “fair” valuations in the current environment, but that does not mean the markets must decline sharply. An extended period of consolidation in the markets with little to no return would achieve the same revaluation process.

(Click on image to enlarge)

What To Expect Next

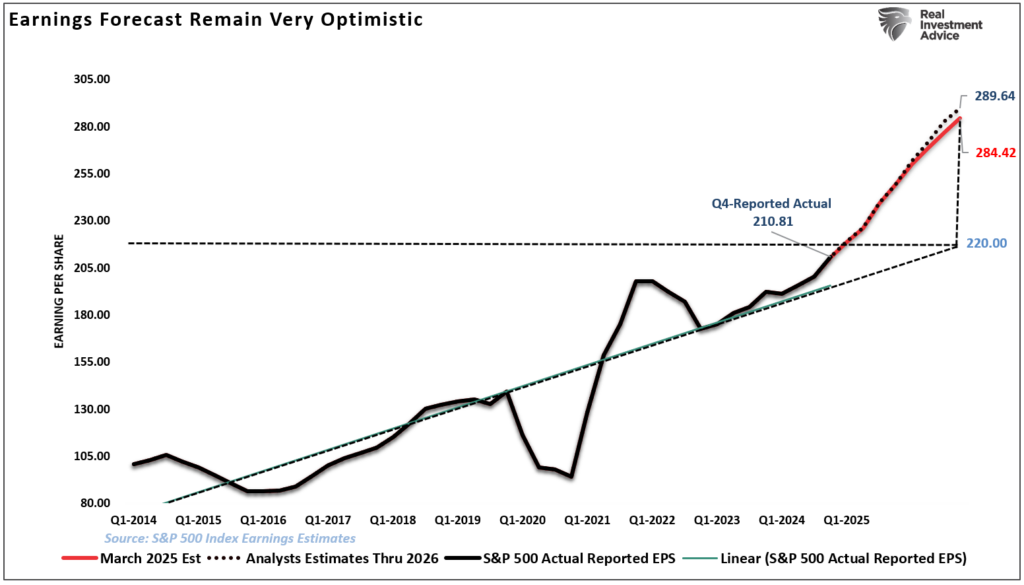

With the current Administration pushing hard on its agenda, on-again, off-again tariffs, spending cuts, and potential increases in unemployment make it difficult for Wall Street to estimate the future impact on earnings. As we have discussed since last year, forward estimates for the economy and earnings were far too optimistic, and now Wall Street has to pare those outlooks back. That process has been slowly in the works over the last two months.

(Click on image to enlarge)

In the future, investors must determine when valuations have re-aligned with economic realities. As such, we continue to expect further bouts of market volatility.

“If economic growth slows in 2025, it could dampen corporate revenue, reduce investment activity, and impact stock prices. Much like a “Curb Your Enthusiasm” episode where things take an unexpected turn, the risk of weaker growth looms large, potentially catching overconfident investors off guard.”

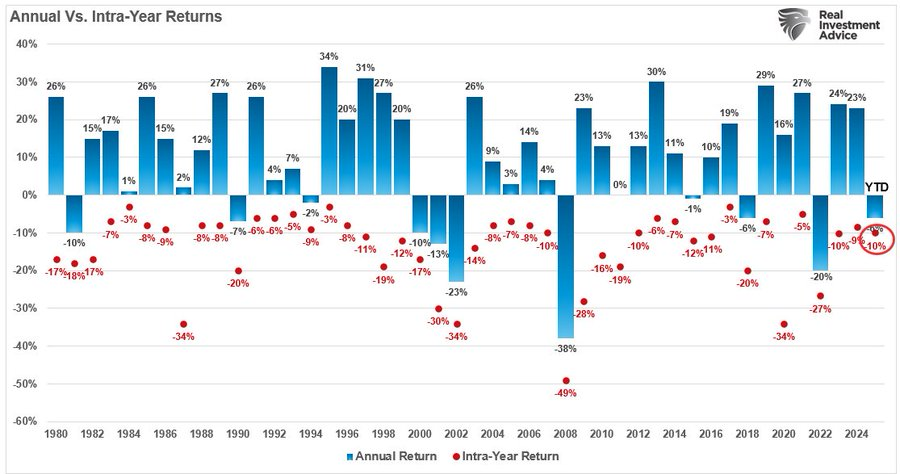

The current market sell off is part of that process of realigning valuations. While the correction has undoubtedly woken up more complacent investors, the decline is well within the confines of a regular annual market correction. We expect similar declines this summer and/or later in the year.

(Click on image to enlarge)

Since valuations have likely not been discounted enough for a slower-growth economic environment, investors need to be prepared for a more frustrating market as forward earnings growth is reassessed. Does that mean a bear market is inevitable? No. But it does not rule out the possibility. Such is why we must remain focused on managing risk and allocations accordingly.

However, the good news is that once that revaluation process is completed, the markets will rise again. The timing of the bull market’s return remains uncertain, but one thing remains true: “This period will end.”

What is critical for investors is not to extrapolate the current market environment into a never-ending cycle. Corrections and bear markets occur regularly, but they end. As investors, we must set aside the narratives and focus on the underlying fundamentals. Crucially, we must be willing to buy when it feels the worst.

(Click on image to enlarge)

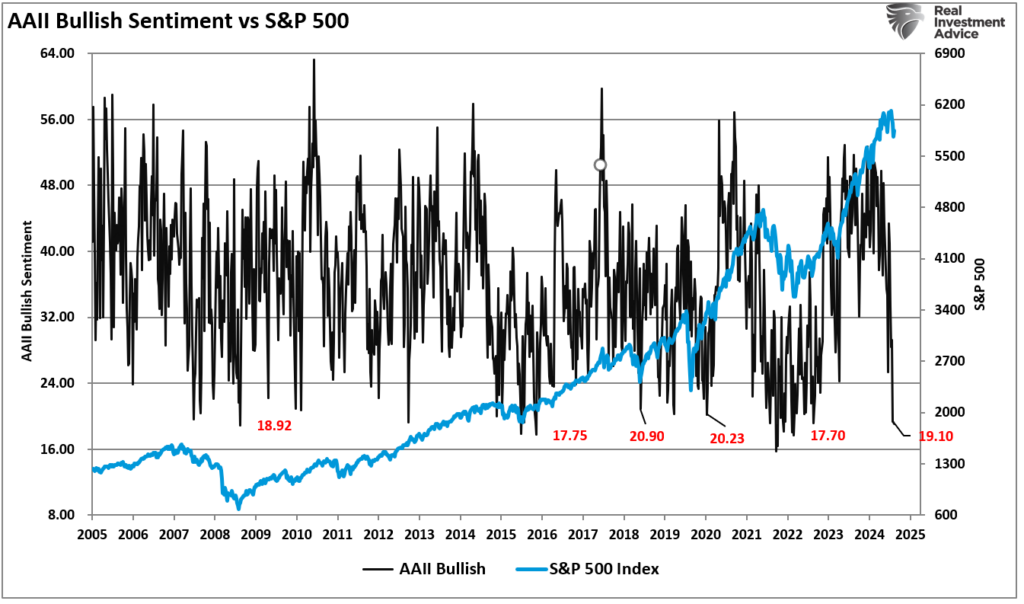

Currently, investors are certainly feeling about as negative as ever. From a contrarian investing viewpoint, such negativity has often provided the best money-making opportunities for those willing to turn against the herd.

Does that mean there is no risk of further downside? No.

This is why we do not suggest going “all in.” A better approach is taking small bites of fundamentally compelling stocks. Look for companies with superior earnings growth that are trading at a discount to the market. Also, the recent correction provides an opportune time to add new capital to portfolios, rebalance current holdings that are underweight targets, and reduce overweights.

Most critical to long-term investing success is not letting market volatility derail you from following your investment strategy.

How We Are Trading It

Let me repeat what we wrote last week, as it remains even more compelling this week.

“We don’t have much history regarding tariffs and the stock market. However, it is likely best to avoid media-driven narratives and focus on managing your portfolio. As we warned previously, media headlines are often wrong.”

“That does not mean that things won’t change in the future. However, using media headlines to make portfolio decisions has repeatedly turned out poorly. If the recent market volatility is weighing on you, and you “feel” you must “do something,” take very small steps.”

- Tighten up stop-loss levels to current support levels for each position.

- Hedge portfolios against significant market declines.

- Take profits in positions that have been big winners

- Sell laggards and losers

- Raise cash and rebalance portfolios to target weightings.

“Remembering that portfolio management is not an “all or none” process is crucial. It is about positioning yourself to minimize emotional decisions so you can find the “opportunity that exists in crisis.”

The markets are deeply oversold, sentiment is bearish, and sellers are exhausted. Such is historically a good setup for a rally to sell into, reduce risk, and prepare for what might be a more volatile market.

(Click on image to enlarge)

More By This Author:

The Rotation To Value From Growth: What Comes Next?

Stupidity And The 5-Laws Not To Follow

The Importance Of Asset Allocation In Building A Resilient Investment Portfolio

Comments

Log in or sign up to join the conversation.