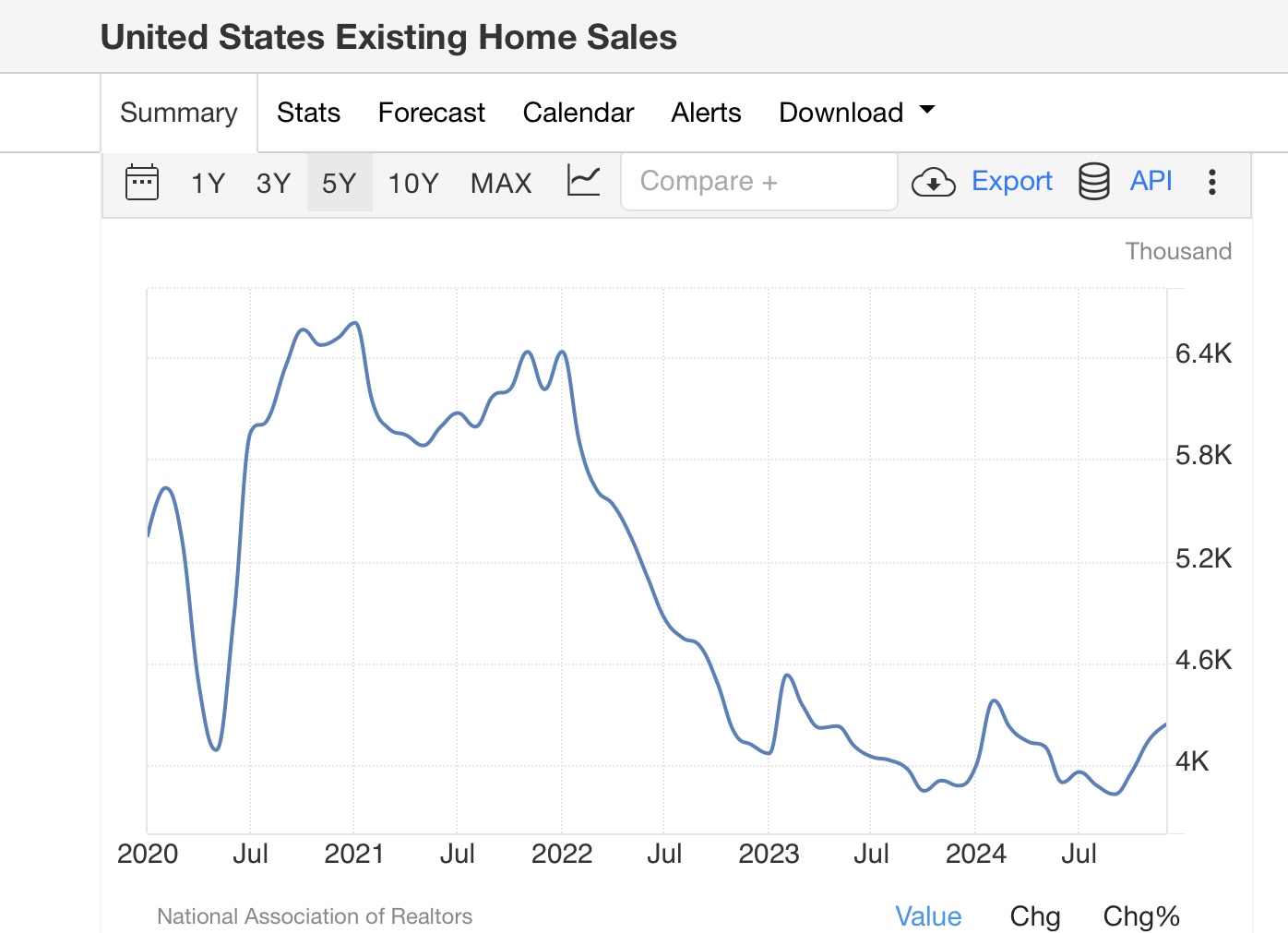

There was some tepid good news as to existing home sales in December, which have been flat in the general range of 3.85 -4.10 million annualized for almost two years. Three months ago they made a 10+ year record low of 3.83 million. They have increased in each month since, and in December they rose to 424.4 million annualized, a 9 month high:

(Click on image to enlarge)

This is likely secondary to the relatively low mortgage rates we saw several months ago in September.

The bad news is that the moderation in the YoY% change in prices from the earlier this year has reversed in the past several month, and in December was up 6.0% (below graph shows non-seasonally adjusted data):

(Click on image to enlarge)

On a YoY basis, in response to the longer term decline in inventory, existing home prices have risen consistently since 2014, and accelerated during the COVID shutdowns. After briefly turning negative YoY in early 2023, troughing at -3.0% in May, comparisons accelerated almost relentlessly to a YoY peak of 5.8% in May of this year. Thereafter the YoY% comparisons declined to 2.9% in September, but here the comparisons since:

October 4.0%

November 4.7%

December 6.0%

Finally, while inventory declined seasonally in December (along with January, typically the lowest level of the year) to 1.15 million, it is the highest inventory for that month since 2019 (note: December data is not shown):

(Click on image to enlarge)

This contrasts with the low of 880,000 in December 2021, vs. the best December level in the past 10 years of 1.86 million in 2014.

In summary, on a non-seasonally adjusted basis sales, prices, and inventory were all up from one year ago. This tells us that the market is continuing to slowly recover from the pandemic collapse, but the re-acceleration of YoY price growth indicates that the now-chronic overall shortage of supply in the housing market continues.

More By This Author:

Jobless Claims: Seasonality And Neutrality Continue

The New Administration And The Return To An Inflationary Era

The Economic Reasons Why The Democrats Lost In 2024

Comments

Log in or sign up to join the conversation.