I’m in natural world mode this week, like a wildlife documentary maker, desperately seeking out signs of growth and optimism. There were sightings in Europe earlier this year, but both are now on the endangered species list. So, I’ve got my magnifying glass out again as I look ahead to next week.

Image Source: Pexels

THINK Ahead: Is Europe really looking that bad?

As my mind momentarily drifted away from growth numbers and inflation curves, I wondered what a wildlife documentary about economists would look like. Here's the AI-inspired voiceover:

“In the bustling urban jungles of our modern world, we find a unique and fascinating species: the economist. And today, we witness a rare event: a gathering of economists sharing an unusual sense of optimism. These gatherings are becoming increasingly rare, as economists, like all endangered species, face numerous challenges in their environment.”

Endangered species? How dare it. As for optimism, well we do need to cast our minds back to the European spring because there were definite sightings. Unfortunately, this inspired article of mine didn't exactly age well.

Strong jobs numbers in the US have convinced investors that the Fed will now cut rates more gradually and less far than first thought. All the while, there’s renewed negativity about the European outlook. So much so that the European Central Bank is poised to step up its pace of easing next week. US-European yield spreads are wider, and EUR/USD is lower.

But what if markets are overdoing the difference between the US and Europe on growth and interest rates? And is this increased 'divergence' actually justified?

We’ve felt for ages that investors have overdone it with the amount of easing being priced in for the Federal Reserve, more so than the ECB. James Knightley has been highlighting how rates would end up higher in the medium-term than the Fed or markets have been pencilling in. That’s particularly true if Donald Trump wins the Presidency and if he can extend and expand tax cuts.

On economic growth, however, the case for renewed divergence is less clear-cut.

The negative bits of the European growth outlook are far from new. Germany is still grappling with a generational shift away from its low-cost energy export model. Weakness in China doesn’t help, but then Europe probably stands to benefit more than America if the recent stimulus boost succeeds in firing up Chinese growth. Expect more news on this over the weekend.

Either way, Carsten reckons this week’s better industrial production and retail sales figures tell us that Germany is still in a zone of endless stagnation rather than a more severe recession. The situation outside of Germany hasn’t materially changed, either. One upside is that the jobs market, though famously a lagging indicator of economic strength, is proving highly resilient across Europe.

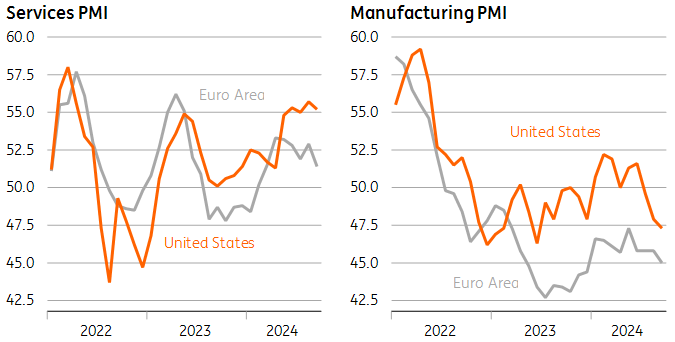

Instead, the fresh wave of negativity that's descended over Europe really stems from a handful of disappointing surveys. The recent purchasing managers indices (PMIs) weren’t great, while Peter Vanden Houte notes that consumers are getting more worried about their job prospects.

Surveys can, of course, be volatile. Don’t forget that the optimism earlier this year came about largely because these same surveys were suddenly looking brighter. That’s why Carsten thinks the case for an ECB rate cut next week isn’t as clear-cut as investors seem to think.

Yes, he’s forecasting a 25bp cut, and yes, officials are getting more worried about the growth outlook. But, they may also reasonably argue against overstating one or two data points.

That’s not to downplay the challenges Europe is facing and, in fact, we’ve revised down our forecasts in our latest ING Monthly. But our numbers for the US this winter don’t look amazing, either.

Admittedly, the current data looks fine; the Atlanta Fed’s nowcast is predicting a very respectable 3.2% annualised growth for the third quarter. Next week’s retail sales are likely to be reasonable, too.

Speaking to James K this week, he reckons the bar is pretty high for the Fed to do anything other than a 25bp cut in early November – barring a shocker at the jobs report due a few days before. However, there have been a lot of mixed messages in recent numbers, and James K writes that the risks to US growth are still tilted downwards.

The message is that this narrative of economic divergence might have gone as far as it realistically should for the time being. Who knows, maybe we'll see another rare bout of optimism before too long. In the meantime, I've got a TV show to make. 'Here, kitty kitty'.

Chart of the week: How US and eurozone PMIs compare

THINK Ahead in developed markets

United States (James Knightley)

- Retail sales/Industrial production (Thu): In the wake of the strong September jobs report and the hotter-than-expected core CPI reading, the market has gone from pricing 75bp of rate cuts over the next two FOMC meetings in November and December to just 46bp at the time of writing. We continue to look for 25bp rate cuts at both the November and December policy meetings. The Fed is clearly trying to replicate the success of the 1995 loosening cycle, directed by Alan Greenspan, that achieved a soft landing and cooler inflation. Monetary policy has been restrictive for some time, and now that inflation, in general, is looking better behaved, it makes sense to lower borrowing costs to give the economy a little more breathing space.

Next week’s data highlights are retail sales and industrial production. Strong auto sales points should provide a good baseline, and we look for 0.4%MoM growth given decent consumer credit card borrowing numbers. There is downside risk to industrial production, though, after last month’s big jump and the fact business surveys suggest the sector continues to struggle. The Fed’s Beige Book, released October 23rd, is the next big report to watch for guidance on the likely path for Fed policymaking.

Eurozone (Carsten Brzeski)

- ECB meeting (Thu): We expect the European Central Bank to cut rates by 25bp next week but think that a hawkish surprise cannot be excluded entirely. The main question for the ECB will be how it interprets the distinction between data dependence and data point dependence. If all of the recent data is regarded as one big data point, there is no reason to cut at the October meeting. If it is regarded as one big series of disinflationary data, it is. In any case, if the ECB decides to cut rates next week, this would mark an important change in its own reaction function. It would be a rate cut to bolster growth. The advantage of such a rate cut would be that the ECB would then suddenly be on a meeting-by-meeting rate cut cycle, hoping to be ahead of the curve and lowering the level of monetary restrictiveness just in time before a more economic accident would happen. Read our full preview.

United Kingdom (James Smith)

- Jobs (Tue)/Inflation (Wed): The Bank of England is a relative hawk right now, but that could be about to change. We expect services inflation to undershoot the BoE's most recent forecasts and continue to do so for the remainder of the year. If we get further hints that employment is cooling, particularly in the real-term payroll data due on Tuesday, that would add to the sense that the Bank can speed up the pace of easing. We continue to expect cuts in both November and December, with rates falling back to 3.25% by next summer.

THINK Ahead for Central and Eastern Europe

Poland (Adam Antoniak)

-

Current account (Mon): We forecast August's current account deficit at €521mn, which translates into a 12-month deficit of 1.0% of GDP vs 1.2% after July. According to our estimates, exports in euro-terms fell by 1.9%YoY, while imports contracted by 0.9%YoY, resulting in a trade deficit of €146mn. Imports were probably boosted by the supply of military equipment in August. We project that deficits in primary and secondary income accounts were accompanied by trade deficits and a surplus in the foreign trade in services.

-

September CPI (Tue): The StatOffice should confirm its flash estimate of September CPI inflation at 4.9%YoY. We already know that higher annual growth of energy and food prices contributed to an increase in headline inflation, but detailed data should tell us the scale of the increase in core inflation, which was probably substantial, partially due to base effects.

-

Core inflation (Wed): Our estimate indicates that core inflation probably increased to 4.2-4.3%YoY in September from 3.7% in August. In September last year, we had a sharp price decline in pharmaceuticals as a new list of refunded drugs was introduced and the list of free medicines for the elderly and children was expanded. Without a similar move this year, annual core inflation increased, probably boosted additionally by a robust increase in education prices, following earlier increases in teachers’ wages.

Czech Republic (David Havrlant)

- Current account (Mon): The current account is expected to have remained in deficit in August, reflecting subdued demand from the main European trading partners. Still, the deficit likely narrowed compared to the previous reading. The headwinds to European and Czech industries are also evident in price competition and, hence, more tepid pricing in manufacturing. We assume that the growth of industrial producer prices softened to below 1% in September.

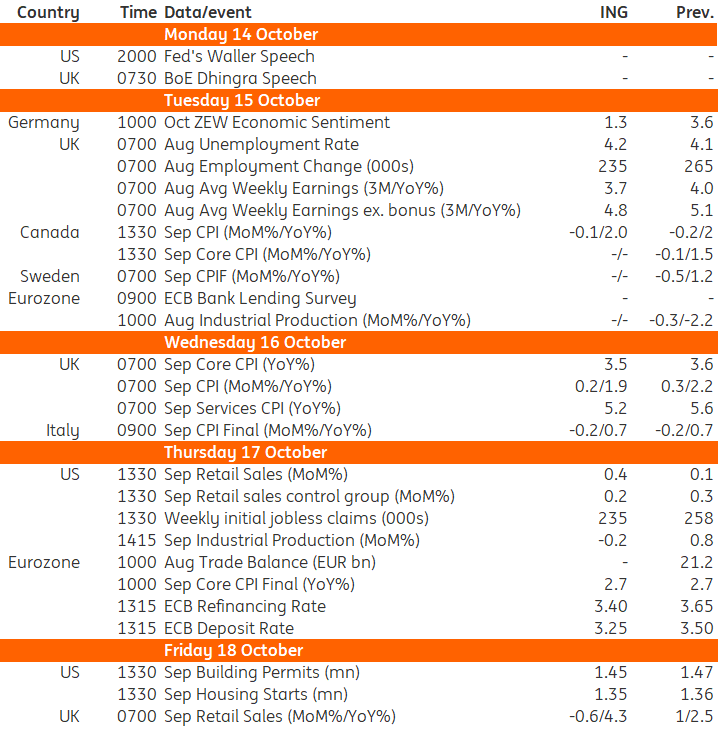

Key events in developed markets

(Click on image to enlarge)

Source: Refinitiv, ING

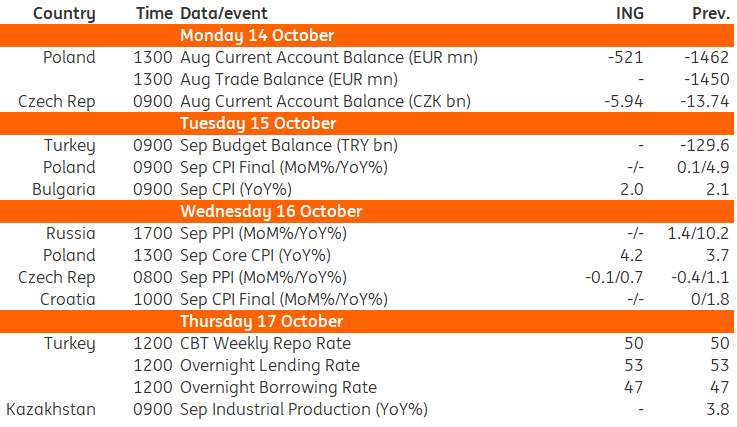

Key events in EMEA

(Click on image to enlarge)

Source: Refinitiv, ING

More By This Author:

Asia Week Ahead: Central Bank Meetings, Inflation Releases And A Data Flood From China

Gold Monthly: US Rate Cut Drives Gold Rally

Turkey’s Current Account Maintains Its Narrowing Trend

Comments

Log in or sign up to join the conversation.