Image Source: Unsplash

China: MoF meeting and big data dump ahead

China's Ministry of Finance announced a briefing scheduled for 10:00 GMT+8 on Saturday. Markets anticipate potential policy announcements related to special bond issuance, tax relief measures, and additional spending plans. This briefing should have a significant impact on the near-term trajectory for Chinese markets as investors are still eagerly awaiting a fiscal stimulus follow-up to September's big monetary policy moves. We continue to expect fiscal stimulus to roll out in the coming weeks and months.

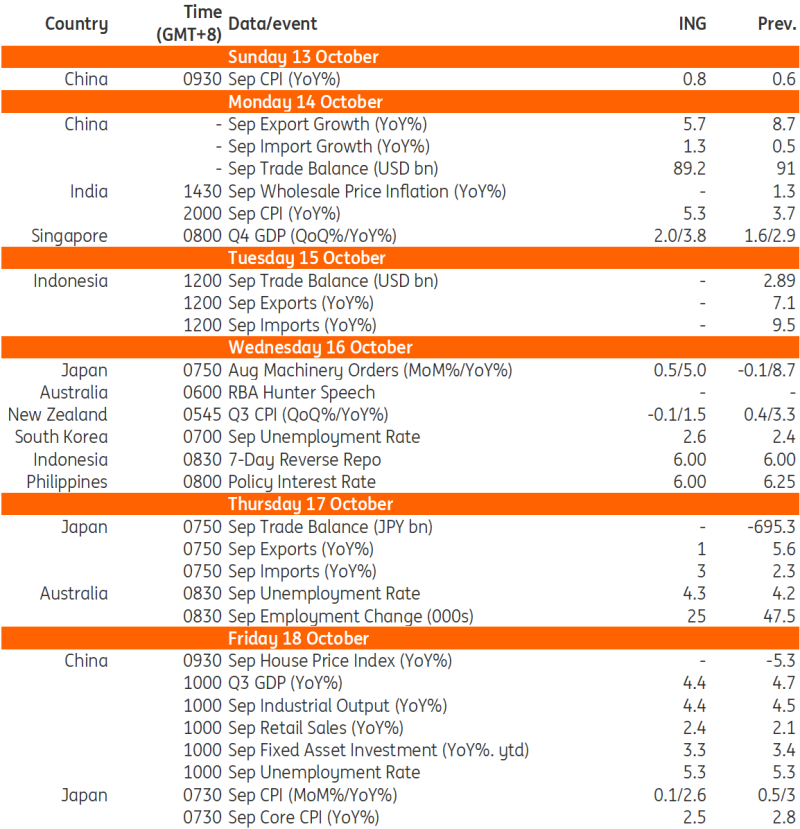

It is a busy week ahead for China’s economic data releases. We have an early start to the week with inflation data coming out on Sunday morning. We expect a slight uptick in the headline CPI inflation rate to 0.8% year-on-year as food prices continue to support the headline level despite increasing signs of non-food deflation risks.

The customs administration will publish August trade data on Monday. We are looking for export growth of around 5.7% YoY and import growth of around 1.3% YoY. One category markets will be closely watching is auto exports, which have come under some recent pressure and are expected to slow further this month. If auto exports turn from tailwind to headwind, it does not bode well for China’s overall export strength.

We get China’s monthly data dump to wrap up the week. This will be headlined by third-quarter GDP. Given weak monthly data to date, we’re on the more cautious side compared to consensus with a 4.4% YoY forecast. We expect September’s activity data to remain weak as well, with the YoY levels for industrial production and FAI likely to remain little changed from the previous month, and retail sales likely to remain sluggish amid weak consumer confidence. After a larger-than-expected decline in property prices for August, we expect a smaller contraction in September, but most of the impact of recent support measures won’t be seen yet in this data.

Central bank action in Singapore, Philippines and Indonesia

It’s a busy week ahead for Singapore. As well as the GDP release for the third quarter of this year, which should show some solid growth of 2.0% quarter-on-quarter and take the annual growth rate up from 2.9% to 3.8% YoY, we also get the Monetary Authority of Singapore’s (MAS) policy statement. We think there is a good chance that it will trim the rate of appreciation of the SGD NEER. 3-month interest rates have fallen by 75bp since July, which indicates that the MAS is having to work hard to keep the SGD NEER from pushing through the top of the current band.

Most forecasters expect the Philippines’ central bank (BSP) to cut rates at its upcoming meeting. The PHP has been quite weak recently, so this could encourage the BSP to be a little more cautious. That said, inflation is very well-behaved, so as long as the PHP doesn’t weaken much more between now and the meeting, a further 25bp cut is on the cards.

After its recent rate cut and some recent softening of the IDR, we don’t expect any further action from Bank Indonesia at its upcoming meeting. The policy rate should remain at 6.0%. Real rates remain high though, so we could still see some more easing before the year-end if the IDR firms.

Japan: Core machinery orders and CPI

The highlight of the week in Japan should be the September Consumer Price Index. Headline CPI inflation is expected to cool sharply to 2.6% YoY in September from 3.0% YoY in August. The renewed utility subsidy should be the main reason for the cooling, and inflation is expected to hover around the 2.5% level for the next few months.

But the key area to watch should be the monthly change in service prices, not the headline rate. We expect service prices to stay flat in September before rising sharply in October. Meanwhile, core machinery orders are expected to rebound 0.5% month-on-month seasonally adjusted in August. Transportation equipment and semiconductor-related equipment orders should lead the gain.

Australia: Labour report lottery

Australia's labour market has been very solid in recent months, averaging close to 85,000 jobs per month over the last three months. Most of this has been full-time employment, though the August data bucked the trend. August’s weak full-time employment growth will likely reverse in September – although we may also see a pull-back in part-time jobs, which could result in a slightly weaker headline employment growth figure. Unemployment has been creeping slowly higher, and we may see the unemployment rate edge up to 4.3% from 4.2%

India: Inflation to rise, but shouldn't last

India's CPI index in September 2023 fell sharply, mainly driven by falling food prices. This year, September food prices are less weak, with seasonal vegetable prices rising. As a result, a 0.5% MoM increase in the CPI index will take the inflation rate up to 5.3% YoY. This will probably not be a lasting increase, as the October and November 2023 CPI indices quickly reversed the September falls, so absent any unexpected price spikes, base effects should work in the opposite direction over the coming months.

Key events in Asia next week

Source: Refinitiv, ING

More By This Author:

Gold Monthly: US Rate Cut Drives Gold RallyTurkey’s Current Account Maintains Its Narrowing Trend

Disinflation Continues In Romania But More Policy Easing Next Month Is Unlikely

Comments

Log in or sign up to join the conversation.