Relationships & Investing

Image Source: PixaBay

When you’re as ancient as I am, you are finally ready to discuss supercycles in an informed manner, owing to the fact that even if you were a lazy business school and/or student in general, you have been around long enough to learn it the hard way, usually punctuated with dollar punishment. Only the gradual onset of partsheimer’s keeps such lessons from being indelible.

This is why supercycle superbubble popping catches most people by surprise; they are too young to have any idea of what happened in previous eras to make a comparison or to understand the underlying fundamentals, and this is underlined by their general attitude that history is not worth studying.

As I grab my oxygen bottle and secure the mask over my face, thus beautifying my overall impression from 2/10 to at least 5/10, the memories from the 1970s come back. My friends and I were young then, so excess testosterone can make any era feel good. New York was in the wake of the wreckage of bankruptcy, so you could get cheap apartments (and cheap dates). Aside from those blessings of youth and a corresponding sense of adventure, things were pretty suckball to the nth degree. Inflation was horrible and about to get worse and to do so for a long time. The subways looked like a junkyard and not one car had air conditioning. The streets looked like what we then called Calcutta (not to be confused with the Broadway show) on a bad day. The stock market sucked, so did the bond market, inflation was rearing its ugly head and Paul Volcker was assuming his role as the bond vigilantes’ chief vigilante and he meant business. I can’t remember if it was a pipe or a cigar but all you had to do was watch this guy smoke to know he was a hawk. It looked like a four alarm fire in the Bronx.

One of the great themes of supercycles is inflation vs. stable money, and the corresponding market action of rotation among industry sectors that play off of the counterpoint between financial assets vs. hard assets and how inflationary costs affect industrial/manufacturing enterprises vs. capital-intensive and financial/tech enterprises.

The stock market is all about breadth and major indexes don’t capture this

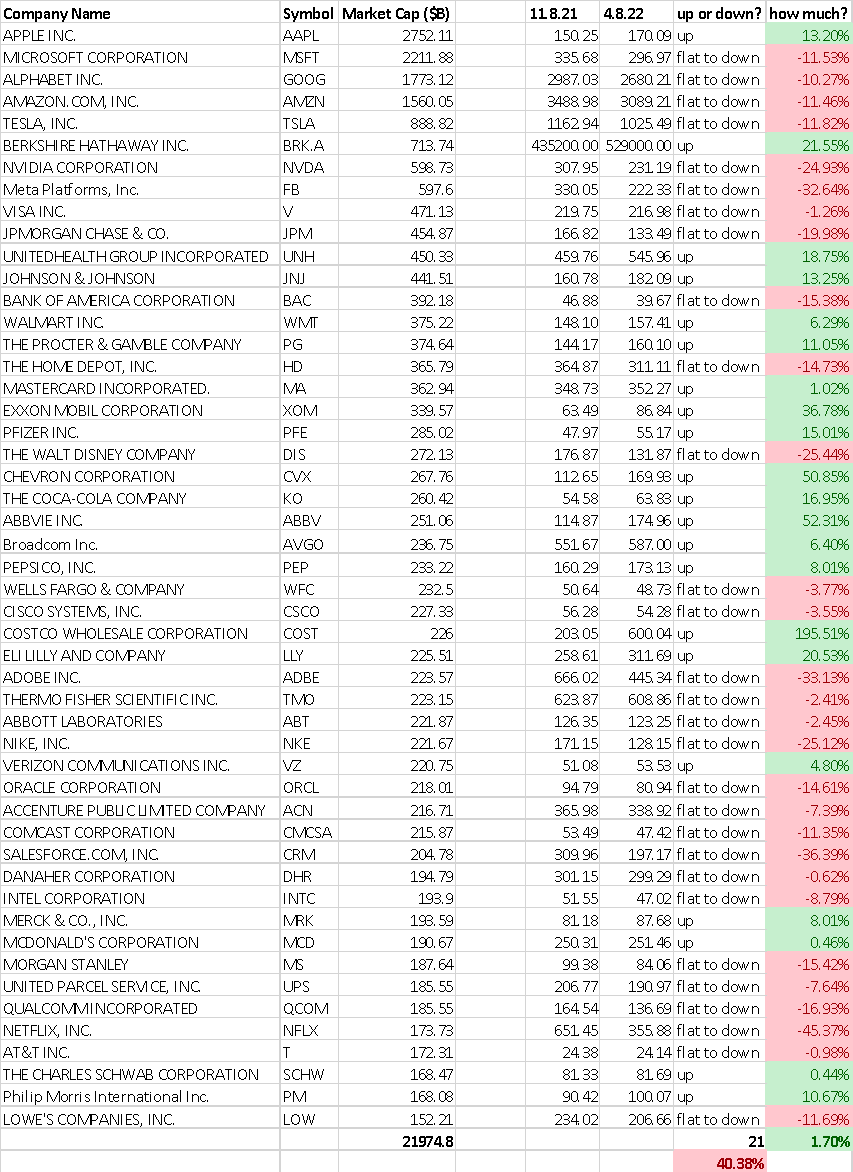

The past six months have not been kind to the stock market and this can be seen from a variety of angles. We know that the popular averages are cap weighted so it stands to reason that if big cap stocks aren’t working then the stock market as measured by these big cap averages is going to reflect a weakening condition.

(Click on image to enlarge)

Substantially fewer than half the big cap stocks on this list that top the market are up over the last six months. These stocks which amount to going on a couple of dozen trillions in dollar market cap drive the big averages have only succeeded in remaining about flat in market value because the minority that have risen have a few names that have done so smartly. This well illustrates the topping process.

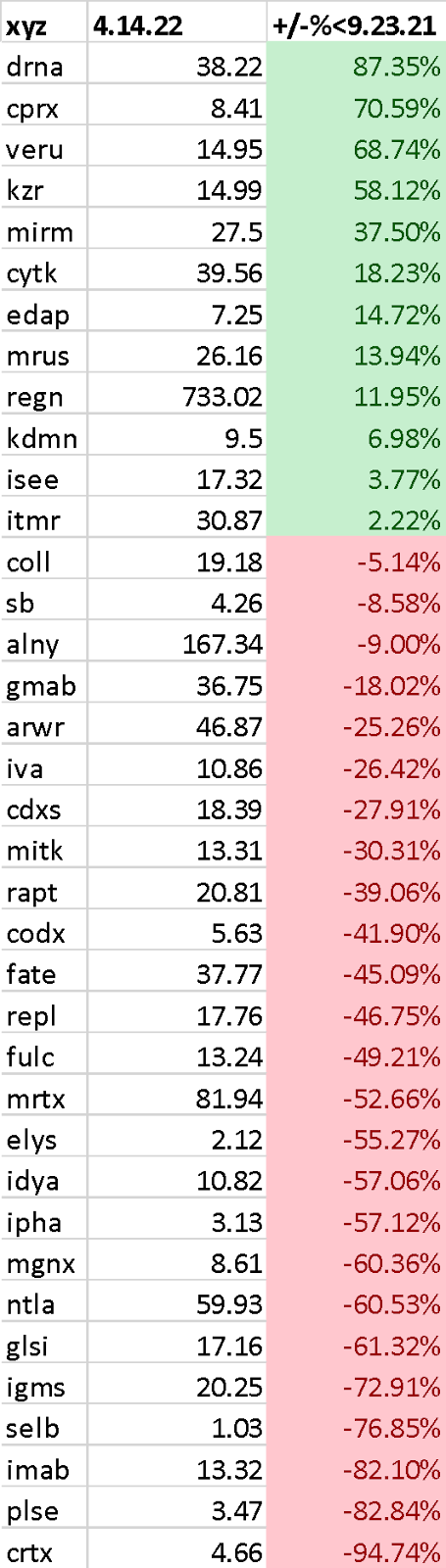

Let’s hone in on some notable examples.

(Click on image to enlarge)

(Click on image to enlarge)

(Click on image to enlarge)

(Click on image to enlarge)

(Click on image to enlarge)

(Click on image to enlarge)

(Click on image to enlarge)

“Time Is Money”

One of the attributes of the topping process I pay close attention to is support levels, and this is a way of “converting” time to money. By that I mean that you can look at especially beat up stocks and see that they are on the verge of coming down to 2017 – 2018 levels, or to 2013 – 2016 levels in some cases.

Here is what that type of average translates to in the S&P 500:

(Click on image to enlarge)

The above “box” of statistics keys off of the current highest intraday high which is 4818.62. The recent close of 4392.59 is nearly nine percent below that. Also shown above are medians for the time frames as indicated, as well as some numbers at various rungs on the ladder all the way down to 1350 and what they would represent in percentage declines from the 4818.62 intraday high.

So, for argument’s sake, what if we came down to 2200? That would be coming down to mean levels of the 2015 – 2018 period. That would be a market cut in half by going back five to seven years. By contrast, when the great crash of 1929 finally bottomed in the midsection of the 1930s great depression decade, that same index had lost 80% of its value and for most stocks it was worse than 90% or just plain disappearance and annihilation. For stocks that remained in existence this was going back to 1880s levels in many cases.

Would you want to be in the brokerage business now?

Don’t be narrow-minded in your analysis of equity valuations; it’s not just about what stocks and companies they represent are worth. Think of it like buying doughnuts and coffee. When you go into your favorite breakfast haunt and consider if it’s worth your hard earned bucks to shell out for their pastries and java, you may be asking something like, “is $4.00 a cup a fair price for this Sumatran brew? Is two bucks a reasonable tariff for this powdered filled tartlet containing a few grams of very average grape jelly?”

I had an old boss (and that means I had this boss a long time ago, and even at that time he was older than I am now) and he was very good at selling advertising space in trade publications when that business was at its peak. You know why? Because in every action he took in the process of selling, he imagined himself being the other guy listening to his pitch and thinking carefully about whether he would have responded favorably if he were the buyer rather than the seller.

This applies to stocks and bonds, it applies to doughnuts, it applies to advertising sales—it applies to everything. “Put the shoe on the other foot,” he would say. At Easter time, I would consider this the New York rough equivalent to Jesus’s golden rule, “do unto others as you would have them do unto you.” It’s part reality, it’s part business economics, it’s part ethical and theoretic positing and it’s part common sense.

But when systems are at critical stress points, it’s a lot more than that. Because that’s when you see that it doesn’t matter which side of the transaction you’re on. It sucks for BOTH the buyer AND the seller. And that’s bad news for everybody.

Back in 1998 the brokerage business—finance in general—was facing a day of reckoning on Wall Street because cost factors, principally commercial rents, were becoming a big strain on business models. Traditionally partnership models were “a third, a third and a third.” A partner was expected to have a third of his net worth in the firm. A third of business top line contribution was expected to come from commissions on trades, a third was expected to come from investment banking deals and a third was expected to come from the firm trading for its own account and resulting distributions to capital holders.

Rising costs started to break this traditional relationship down, and at first firms dealt with this by leveraging up. Needless to say, nobody gets something for nothing and this meant extra risk and volatility as leverage at some firms doubled and tripled and borrowing costs became significant. It wasn’t long before failures occurred. One noteworthy “canary in the coal mine” was Goldman announcing it would go public during the late 1990s and, as far as stock prices were concerned, 1998 was a year the stock market couldn’t have looked rosier, especially in the hot technology sector at that time when dot com was the name of the game and AOL had gotten so big in capitalization terms, it became the dog that ruled over the mere tail known as Time-Warner. Not too long after that imbalance (that at the time didn’t seem so out of balance), the only shortage downtown was crying towels. So put the shoe on the other foot and think like Jesus debating the Pharisees. For example, I see lately the IPO business YOY ain’t lookin’ so hot, as in off by 70%. Yikes! That should tell you something about life right now, whether you’re buying the doughnuts and coffee or selling them. There is strain on the system.

Here incidentally is what the market looks like at major tops (and major bottoms), and how the brokerage business as represented by the XBD broker-dealer index punctuates the evidence of and visibility of the highs (and lows).

(Click on image to enlarge)

Such a confluence of contradictions and confusions!

I have often said that quantitative analysis is of no value without the counterpoint of qualitative articulation. So at this point I am going to jawbone a bit and get very subjective. If you think that’s what I’ve been doing so far, you ain’t seen nothin’ yet, to coin a phrase! Let’s go back to my opening contextual recount of the 1970s and with particular reference to the decrepit condition of New York that then prevailed. And it really was awful, whether dirt, filth, crime, inflation, declining city services, high unemployment, you name it.

But here’s the curve ball! There were tons of young arrivals, we were excited about being in the city and we were optimistic. Of course we were often depressed by what everyone with rational eyeballs could see all around us, but there was an underlying desire to hustle and a sense that opportunity would come back. Don’t ask me to explain this or why it was, but it was there and I will bet a plate of spaghetti from Little Italy that if you ask my contemporaries about this they will recall that same sense. It was not cut and run.

Here’s my point in bringing this point up. I don’t think that’s the case at all today. As I say above, these are subjective calls and I am not offering hard evidence because I don’t have anything but a gut feeling.

In fact, if there is any evidence to summon, it would indicate the opposite. Rents are still rising. Real estate transaction prices are still rising. Worker shortages are the rule to an extent larger than unemployment was a problem in 1975.

But is there optimism like there was 40 or 50 years ago? No there isn’t, not in my view. Most people are not happy about being in the city. Most people are overwhelmed just by “the little things,” meaning, as one example, the experience you have riding the subway, or walking half a dozen blocks to your favorite grocer for your dinner ingredients…an experience I always treasured.

And yet this is not translating to a negative view of capital markets. Just the opposite. The most common view I hear in response to market pessimism is “I keep hearing about this huge crash we are going to have, I’ve been hearing this negative talk for years, and it hasn’t happened. My net worth is increasing. It’s all valueless whining.”

The Question is, is this rejection of “the sky is falling” consistent with portfolio manager positioning?

No it is not. Managers all over town are positioning for “the sky is falling,” and they are not admitting it to anybody. The most charitable thing that can be said about this is that they are hedging “just in case.”

Only that’s not exactly what’s going on either.

What’s really going on is that they are loading up in healthcare which, as a consequence, as well as the fact that this sector already had a huge capitalization presence in the first place and then had this presence redoubled by the policy response to covid, is still going to the moon and has near-perfect looking charts. In the stock market you can hedge in a number of different ways. One way to hedge is to be long some stocks and short other stocks. Another way to hedge is to have derivatives that capitalize on tail-risk expectations and especially clever practitioners of this game have very sophisticated mathematics and strategies that key on how far out of the money you position so as to acquire enormous amounts of hedging protection very cheaply that kicks in super big time with enormous wrong-way moves. Still a third way to hedge is to go the so-called low beta route, to have a percentage of commitment in stocks that consistently do well but which for every dollar move in the index their beta is measured against as a benchmark, move less than that benchmark. The favorite sector in this regard is healthcare, and here is why:

(Click on image to enlarge)

(Click on image to enlarge)

(Click on image to enlarge)

What’s going on is NOT that stocks like Humana, United Health and Anthem are low beta stocks that make good hedges when markets go south; what’s going on is that these stocks are depended upon as huge long positions that contribute heavily to manager performance when it’s sunny skies every day and everything is fine and dandy. This is not defensive positioning at all, it’s what managers want to be long.

This is why I call the health care sector the gender fluid sector. Because all kinds of things fit into it. Stocks of companies that are hospital chains. Stocks of companies that make prescription drugs. Stocks of companies that are insurance policy underwriters and distributor/marketers/servicers.

Companies that crack and manipulate the human genome, or modify the RNA of viruses, or provide technological assistance to mRNA innovators.

You can be in all kinds of businesses in this sector, many of which bear no resemblance to one another, and still call yourself “healthcare.”

And many of these companies are not low risk or low beta at all. They are straight out of the mold of the go-go stocks of the 1960s. And if you want to know how that goes, watch the documentary on Carl Icahn and let him explain to you himself what happens when you reject your boss’s experience and friendly advice, think you are God, and thus lose your money, your girlfriend and your fancy car

Here’s what “healthcare” stocks also look like—a very far cry from those beautiful charts above:

(Click on image to enlarge)

These are not low beta stocks at all. These are companies managers are up to their ears in that are making excellent contributions to far reaching advances in how we treat diseases and save and extend lives and quality of life. But they are more like private equity bets, where a few do great and most get killed. But they are all “healthcare.” And these results in this compilation are just since last September.

One of the huge innovations that has occurred and mostly been adopted in big money style since the mortgage meltdown is the ETF craze which State Street has done extraordinarily well with by emphasizing “why take single stock risk?”

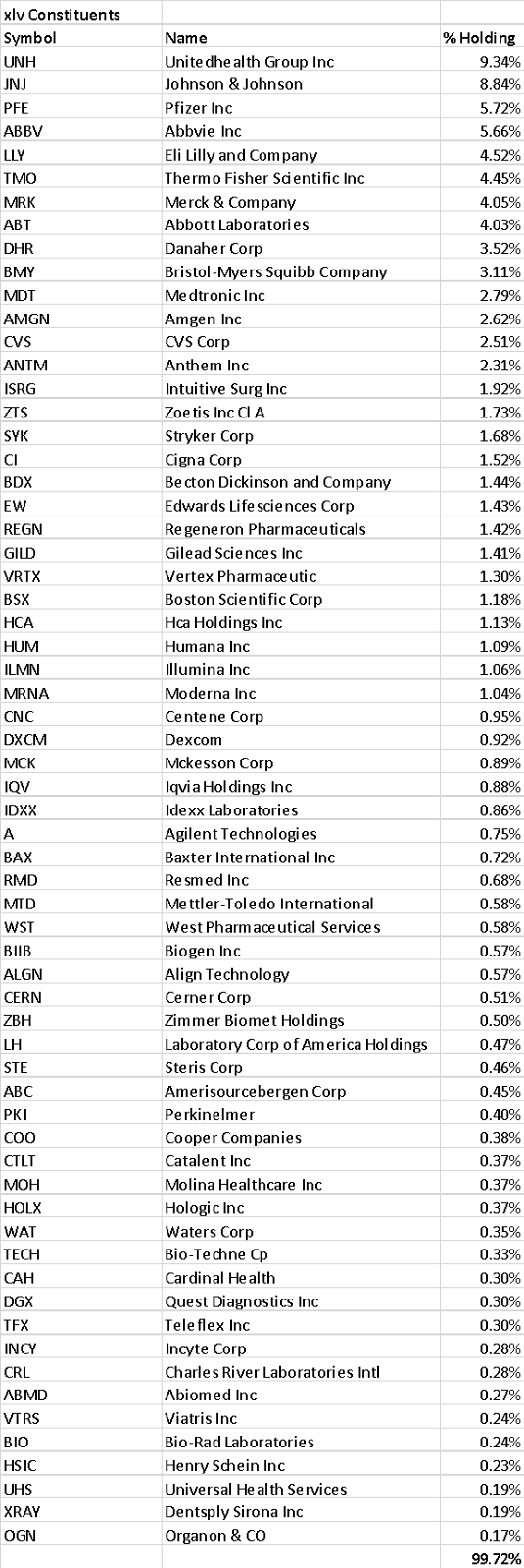

Now let’s look at the XLV health care sector ETF:

(Click on image to enlarge)

All of these companies are in healthcare, to be sure, and there is no question that single stock risk is being avoided. But if you are saying that being in the dental supply business is the same thing as packaging and selling insurance policies, I would respectfully beg to differ. To analogize back to the doughnut discussion, some doughnuts have a hole in them and some do not. They are very different kinds of doughnuts. Gender fluidity is a nice concept designed to lend widespread compassion and alleviate dysphoria but in portfolio management you need to have a bit more focus and take a stand. And when you say you are hedging when in fact you are loading up on what performs well as an outperforming long during up markets, you are trying to have it both ways. So I guess you would have to say management is more of a binary game.

I might add that the RLH Volatility Model is decidedly bearish on healthcare and has been for some time. I think this sector and how it is (mis)conceived of may turn out to be one helluva big black swan.

Concluding thoughts

When I pointed out that AOL once ruled over Time-Warner and that traditional partnership squeamishness over overblown leverage led to people in the business deciding to cash out and go public, those are the signs you see three levels up from the nitty gritty of looking at charts. There are others. The biggest of these is when a supercycle coming to an end is so long that nobody has lived long enough to have personally experienced it from end to end. Others include observations of huge career shifts: large numbers of doctors and lawyers getting into the finance business. I really wonder what folks like that are expecting to get away with. Or the crypto craze? I will save a discussion of crypto for another piece but you can’t deny that this incredibly large phenomenon has attracted orders of magnitude measured in trillions of dollars and done so in a remarkably short period of time. Finally, there is this very thorny issue(s) of inflation, monetary integrity (which the crypto craze plays off of) and some very practical arithmetic of what is a central bank neutral rate and how high is up when it comes to taming double digit inflation. Even a miniature poodle at the dog show is smart enough to know that when you have an interest only loan that’s the size of the budget for the pentagon…if the average rate on that has to quadruple in order to get inflation down, that “interest only” is going to break the U.S. Treasury’s and the taxpayers’ collective back…and also lead to enormous amounts of incremental debt issuance at the higher level. So then what? The fed switches horses in midstream, calls it quits and lets inflation rage on? How does that turn out well? Tony Blinken is telling us that the Ukraine situation is going to go on full bore for at least the remainder of the year. So will inflation abate on its own with that kind of background factor in play? And why the heck is this war raging in the first place, with an alleged actor/comedian at the helm of a so-called victim nation who just happens to be worth going on $700 million? How did that happen? And if you think the covid policy response had something to do with giveaways to big pharma, including protection from liability on vaccines, is it farfetched to see Ukraine as a preemptive Marshall Plan for landlords and developers that got locked down into rent starvation? You may think I’m insane for raising questions like this but if I am, I’d love to hear the sane explanations. I see a bond/equity meltdown that gets these two asset classes back to their traditional relationships (and a lot lower in doing so), and I also see a black swan in healthcare that kicks the teeth out of folks who think this is a hedge.