The Fed's minutes were unanimous on the hike delivered, but there doesn't appear to be quite as much clarity on what to do next. That's reflected in where the market discount is. The minutes also delve into the murky world of liquidity and the banks, striking a cautionary but constructive tone. A debt ceiling resolution would help to clear things up.

Federal Reserve minutes comment heavily on liquidity and the banks, and there is a debt ceiling tinge there too

While the Fed minutes highlighted the split in the Federal Open Market Committee (FOMC) and the desire to keep as much optionality as possible, there was also quite some commentary on liquidity conditions and banking circumstances. The Fed struck a confident tone on the banks in general, noting a tightening in lending standards in small to medium-sized banks ($50-250bn in the balance sheet). At the same time, they noted correctly that deposit outflow had been limited to a small number of banks, and typically to smaller banks. Overall, banks in general remain in a healthy state. Specific mention of exposure to commercial real estate also featured, noting that some downsizing in valuations here poses risks ahead.

The Fed also points out that flows seen from deposits to money market funds are not a response to their policies per se. The link here is with the reverse repo facility, as many government money market funds will use this facility, and the rate at the facility is clearly set by the Fed. But the Fed notes that the rate on the reverse repo facility is doing its job, helping to set a floor for official rates – and in turn helping to steer the funds rate to an appropriate level.

The Fed also notes that volumes in the reverse repo facility are likely to climb further in the months ahead, which would be the case where flows into money market funds continue. The other factor here is the dearth of bills supply, related to the struggles with the debt ceiling. This limits the opportunity for money market funds in terms of alternatives to the reverse repo facility. The Fed does expect to see reverse repo volumes ease lower later in the year, which makes sense.

Once the debt ceiling is raised or suspended, we should see considerable bills issuance, providing money funds with an alternative to the reverse repo facility. No surprise that the Fed highlighted the importance of taking action on the debt ceiling. Any worries that they had at their meeting on 3 May have no doubt been elevated further since.

Meanwhile, we've seen two stellar auctions in the past couple of days in the 2Y and 5Y T-notes. We don't see this as a debt ceiling play, as the outcome cuts in the same direction. A resolution means more supply, while no resolution heightens the risk of a buyers' strike. Both in fact push for upward pressure on yields. So, view the strong bid at auction as value hunters within the rates cycle rather than positioning on the debt ceiling outcome.

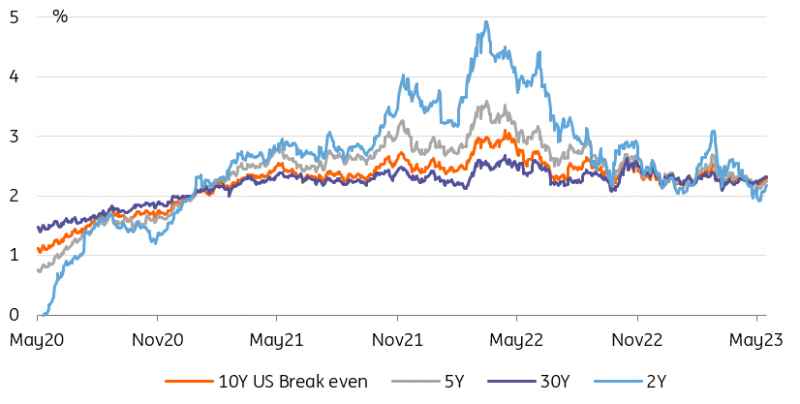

An uptick in US inflation break-evens add to the sense of unease at the Fed

Source: Refinitiv, ING

Bank of England path repriced to at least three more rate hikes

The European session ahead of the FOMC minutes was marked by a significant shift higher in Sterling rates, following an inflation reading that came in higher than all forecasts. A repricing of Bank of England hike expectations pushed 2y Gilt yields up by 23bp by the end of the day. Essentially the market is now seeing a good chance that the Bank of England could push up interest rates to 5.5% before the year ends. A hike next month is a done deal with respective forwards 31bp above current levels. While the long end initially jumped 20bp as well, 10y yields ended the day only about 5bp higher, leaving the curve to flatten a substantial 18bp.

BoE Governor Andrew Bailey struck a more sanguine tone in reaction to the new inflation data. One reason he gave was that he estimated that only about one-third of the rate hikes so far had actually hit the economy by now – a lot of the tightening impact is still in the pipeline. Our economist also cautions that we will still get another set of data before the June meeting, and points out that jobs/wages data has been moving in the right direction, as have broader survey measures of price-setting behavior.

In any case, the UK inflation surprise has hit a nerve amid concerns that central banks’ jobs are far from over. In Europe, front end rates are also pushing higher. Not as violently, but the concern around stickier underlying inflation is being shared. Services inflation is the flashpoint here with recent PMIs underscoring the growing bifurcation in the economy between the services and manufacturing sector. That certainly does not make the European Central Bank's job any easier, but when even the doves at the ECB like Spain’s de Cos see the central bank not done yet with hiking it suggests that the consensus around higher rates is strengthening. Parsing market indicators of inflation expectations the trending higher of the 5y5y forward inflation swap could also raise concerns that the grip on inflation is loosening again.

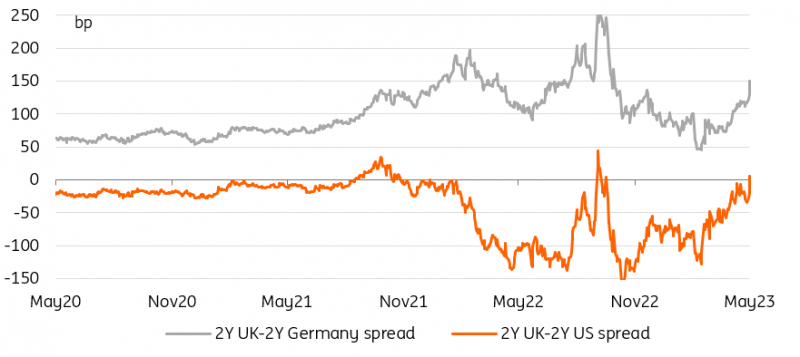

2Y UK rates shoot up on a hotter than expected CPI report

Source: Refinitiv, ING

More By This Author:

A Challenging Year Ahead For Dutch Hospitality

UK Inflation Shock Raises Chance Of June Rate Hike

FX Daily: Dollar Grinding Higher

Comments

Log in or sign up to join the conversation.