In recent testimony to Congress’s Joint Economic Committee, Jerome Powell stated:

“The debt is growing faster than the economy — that’s unsustainable. It’s not the Fed’s job to say how the government should cut the deficit, but we need to get the economy to grow faster than the debt. Otherwise, future generations will be paying more of their taxes to cover the government’s debt costs than for other things like health care, etc.

I think the new normal now is low interest rates, low inflation and probably lower growth. Even with the lower interest on its debt, the government still needs to reduce its budget deficit.”

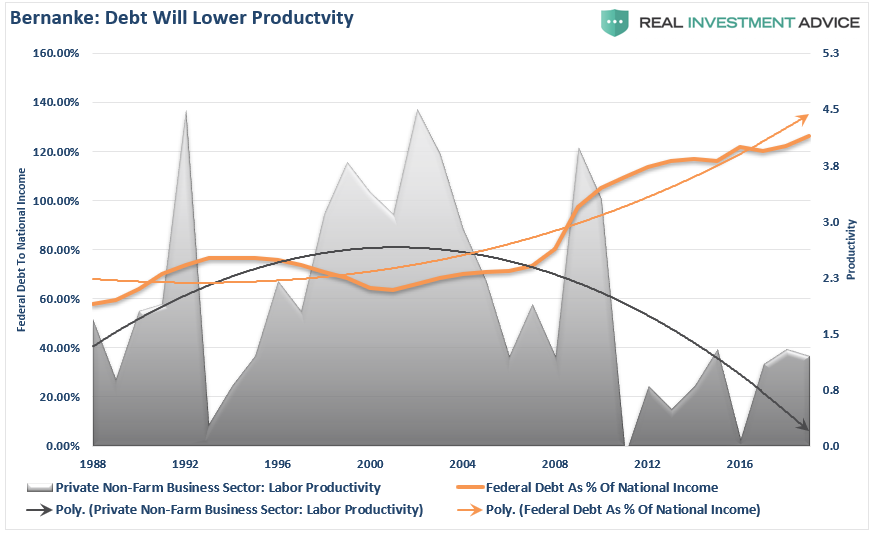

Interestingly, these were not the first time we heard these words. In 2012, then-Fed Chair Ben Bernanke told Congress:

“Rising federal budget deficits are posing a significant threat to the U.S. economy and are likely to cause a crisis if not brought under control. Having a large and increasing level of government debt relative to national income runs the risk of serious economic consequences. Over the longer term, the current trajectory of federal debt threatens to crowd out private capital formation and thus reduce productivity growth.”

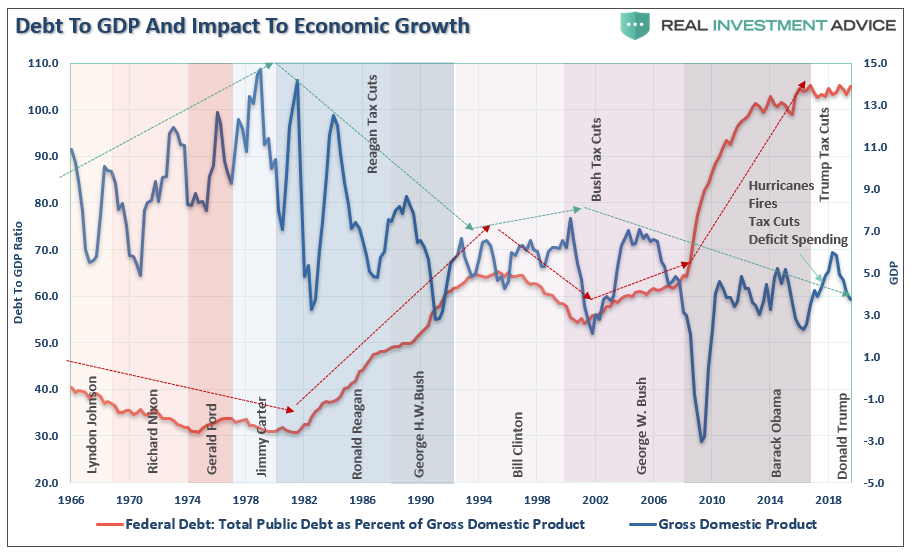

Looking back now, it was clear that Bernanke was correct. Over the last 30-years, the rising level of Federal Debt relative to National Income has retarded Productivity in the U.S.

Of course, just as is the case today, Congress didn’t listen then either. Just a couple of months later in July 2012, as Congress was feuding over a “debt ceiling limit funding deal,” Ben Bernanke testified before the Senate Banking committee stating that “fiscal policy” needed to take over for “monetary policy.”

The response from Congress?

“Given the political realities of this year’s election, I believe the Fed is the only game in town. I would urge you, now more than ever, to take whatever actions are warranted. So, get to work, Mr. Chairman.” – Sen. Charles Schumer, D-N.Y.

Almost 8-years later, with the deficit once again approaching $1 Trillion, the Federal Reserve remains the “only game in town.” Such was the case following Jerome Powell’s plea to Congress to enact some responsibility, but all Wall Street heard was: “More QE is coming.”

Such should not be surprising. Regardless of political affiliation, the idea of “fiscal responsibility” in Washington has been replaced by all-out “socialist” leanings. However, you are mistaken if you believe this to be a new mentality in Washington.

It isn’t.

Like a “frog being boiled in water,” the temperature has been slowly rising for the last 20+ years as deficits grew to support unbridled largesse in Washington.

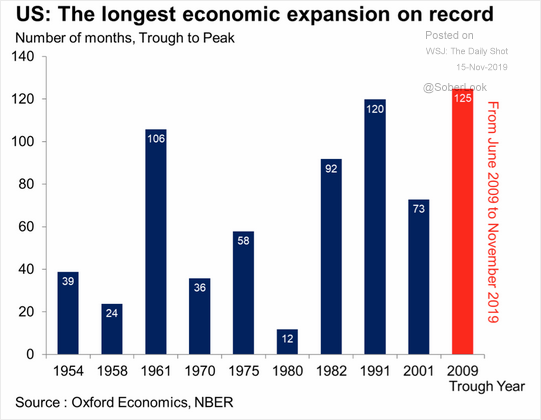

What is most important to understand is that this surging deficit is occurring during the longest economic expansion on record. Naturally, given the lack of immediate negative consequences, many have come to believe that debts, and deficits, don’t matter.

However, the evidence, should those in Washington D.C. care to examine, is using debt to “pull forward consumption” has had long-term negative effects on economic prosperity.

The current expansion is the weakest in U.S. history.

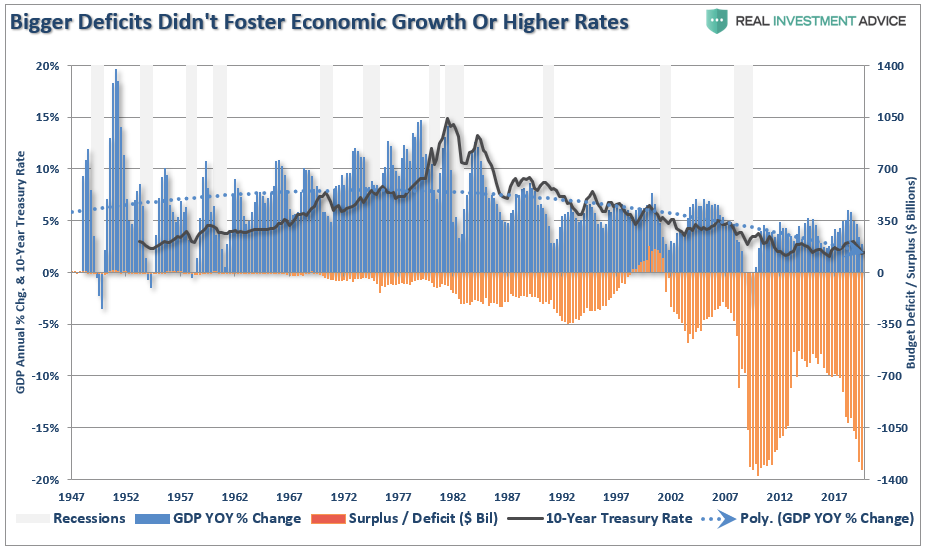

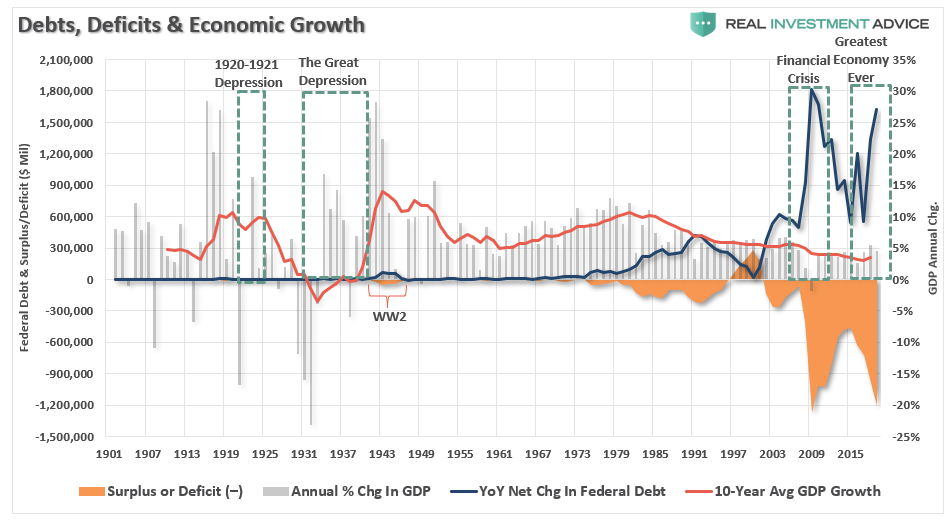

Here is a little different way to look at it. The chart below shows the deficit, 10-year average GDP growth, and the annual change in Federal Debt.

The problem should be obvious. Since the Federal government began ramping up debt, and running an annual deficit, economic growth has continued to deteriorate. This is not just a coincidence.

With the government already running a massive deficit and expected to issue another $1.5-2 Trillion in debt during the next fiscal year, the efficacy of “deficit spending” in terms of its impact to economic growth has been greatly marginalized.

John Maynard Keynes’ was correct in his economic theory. In order for deficit spending to be effective, the “payback” from investments being made must yield a higher rate of return than the debt used to fund it.

The problem has been two-fold.

- “Deficit spending” was only supposed to be used during a recessionary period, and reversed to a surplus during the ensuing expansion. However, beginning in the early ’80s, those in power only adhered to “deficit spending part” after all “if a little deficit spending is good, a lot should be better,” right?

- Secondly, deficit spending shifted away from productive investments, which create jobs (infrastructure and development,) to primarily social welfare and debt service. Money used in this manner has a negative rate of return.

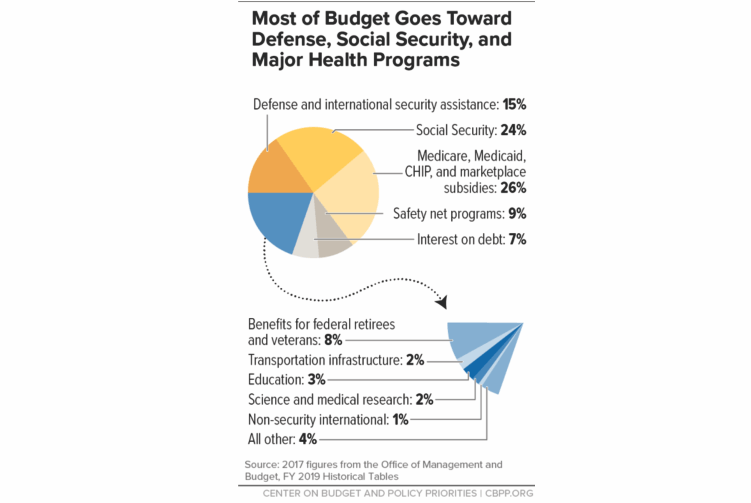

According to the Center On Budget & Policy Priorities, roughly 75% of every tax dollar goes to non-productive spending.

Here is the real kicker. In 2018, the Federal Government spent $4.48 Trillion, which was equivalent to 22% of the nation’s entire nominal GDP. Of that total spending, ONLY $3.5 Trillion was financed by Federal revenues and $986 billion was financed through debt.

In other words, if 75% of all expenditures is social welfare and interest on the debt, those payments required $3.36 Trillion of the $3.5 Trillion (or 96%) of revenue coming in.

Do you see the problem here? (In the financial markets, when you borrow from others to pay obligations you can’t afford it is known as a “Ponzi-scheme.”)

Debt Is The Cause, Not The Cure

I am not saying that all debt is bad.

Debt, if used for productive investments, can be a solution to stimulating economic growth in the short-term and provide a long-term benefit.

The current surge in unbridled deficit spending only succeeds in providing a temporary illusion of economic growth by “pulling forward” future consumption, leaving a void that must be filled.

Since the bulk of the debt issued by the U.S. has been squandered on increases in social welfare programs and debt service, there is a negative return on investment. Therefore, the larger the balance of debt becomes, the more economically destructive it is by diverting an ever-growing amount of dollars away from productive investments to service payments.

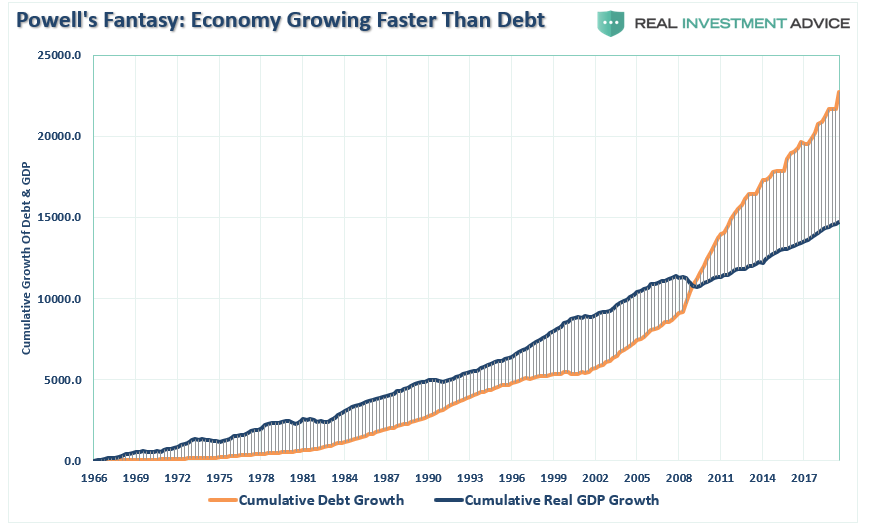

In other words, Powell is hoping for a “fantasy” the economy can grow faster than the debt.

The relevance of debt growth versus economic growth is all too evident as shown below. Since 1980, the overall increase in debt has surged to levels that currently usurp the entirety of economic growth. With economic growth rates now at the lowest levels on record, the growth in debt continues to divert more tax dollars away from productive investments into the service of debt and social welfare.

However, simply looking at Federal debt levels is misleading.

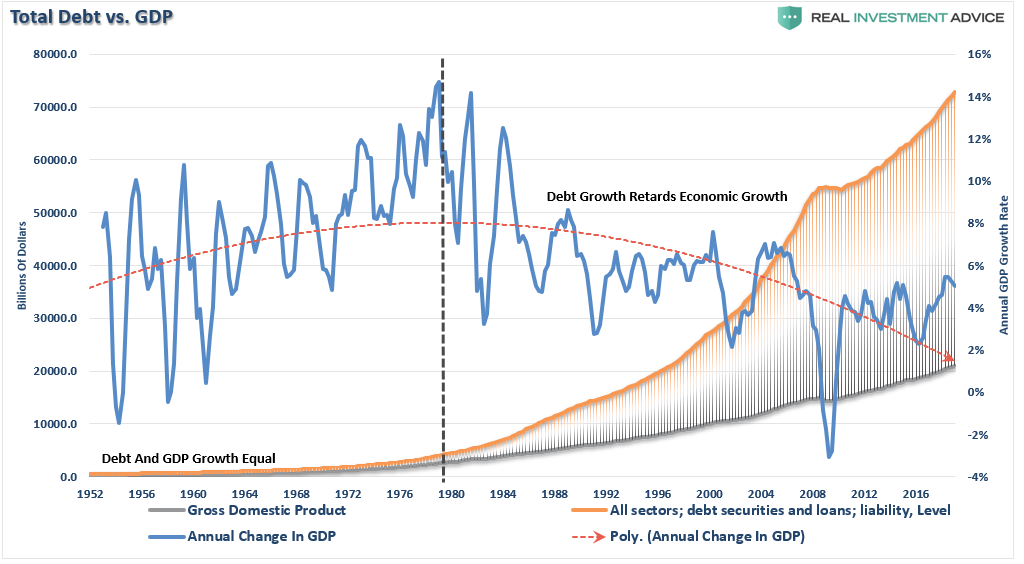

It is the total debt that weighs on the economy.

It now requires nearly $3.00 of debt to create $1 of economic growth.

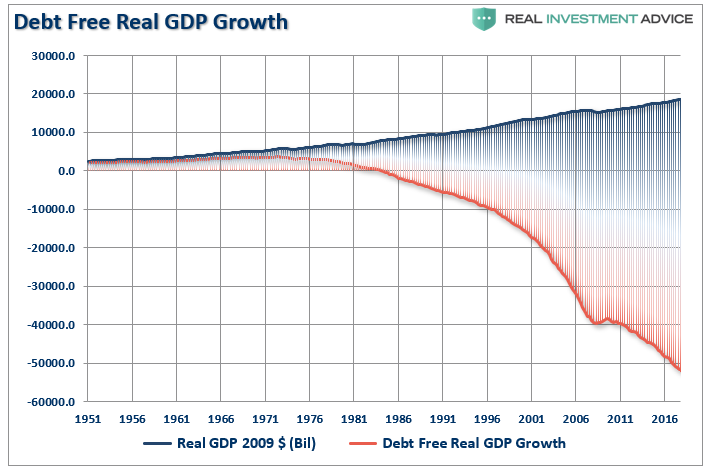

Another way to view the impact of debt on the economy is to look at what “debt-free” economic growth would be. In other words, without debt, there has actually been no organic economic growth.

In fact, the economic deficit has never been greater. For the 30-year period from 1952 to 1982, the economic surplus fostered a rising economic growth rate which averaged roughly 8% during that period. Today, with the economy expected to grow at just 2% over the long-term, the economic deficit has never been greater.

This is why Jerome Powell is “wishing for a Unicorn.”

Interest rates MUST remain low, and debt MUST grow faster than the economy, just to keep the economy from stalling out.

This is the very essence of a “liquidity trap.”

Debt Doesn’t Create Real Growth

The massive indulgence in debt has simply created a “credit-induced boom” which has now reached its inevitable conclusion. While the Federal Reserve believed that creating a “wealth effect” by suppressing interest rates to allow cheaper debt creation would repair the economic ills of the “Great Recession,” it only succeeded in creating an even bigger “debt bubble” a decade later.

This unsustainable credit-sourced boom led to artificially stimulated borrowing which pushed money into diminishing investment opportunities and widespread mal-investments. In 2007, we clearly saw it play out “real-time” in everything from sub-prime mortgages to derivative instruments which were only for the purpose of milking the system of every potential penny regardless of the apparent underlying risk. Today, we see it again in accelerated stock buybacks, low-quality debt issuance, debt-funded dividends, and speculative investments.

When credit creation can no longer be sustained, the markets must clear the excesses before the next cycle can begin. It is only then, and must be allowed to happen, can resources be reallocated back towards more efficient uses. This is why all the efforts of Keynesian policies to stimulate growth in the economy have ultimately failed. Those fiscal and monetary policies, from TARP and QE, to tax cuts, only delay the clearing process. Ultimately, that delay only deepens the process when it begins.

The biggest risk in the coming recession is the potential depth of that clearing process.

Despite Powell’s wishes that Congress will become adults and begin to reduce the Federal debt burden, the reality is the economy can not sustain itself without the debt.

While we do have the ability to choose our future path, taking action today would require more economic pain and sacrifice than elected politicians are willing to inflict upon their constituents. This is why throughout the entirety of history, every empire collapsed eventually collapsed under the weight of its own debt.

Eventually, the opportunity to make tough choices for future prosperity will result in those choices being forced upon us.

Comments

Log in or sign up to join the conversation.