Just 2 more trading days remain in 2019 and with that, we are looking forward to the longest expansion cycle in U.S. history continuing... and to be accompanied by the continuation of the bull market. Before we look at what lay ahead we revisit the past, specifically December 17, 2018. In our final Research Report of 2018 we offered Finom Group (for who I am employed) subscribers the following outlook for 2019:

"There is nothing materially wrong with the U.S. economy, despite the S&P 500 YTD performance. Global macro-headwinds along with geopolitical headwinds have combined to increase the level of fear surrounding future corporate earnings, compressing the SPX multiple in much the same way it did from late 2015-2016. Back then and much like today, oil prices plunged and the yuan was steeply devalued. The same permabear rants that proliferated back then are present today. Having said that, the bears only found SPX marching higher thereafter and as earnings growth accelerated into 2017 and beyond. Get ready for a potential bounce in the coming weeks as the calendar year ends and begins a New!"

Moving into 2019, our outlook for 2019 and theme was coined with the acronym "EFG". This thesis was nothing out of the ordinary or outside of normal economists' considerations when delivering a logical outcome for economic growth and financial market probabilities.

- Earnings

- Federal Open Market Committee (FOMC/Central Banks) Policy

- Global Trade Relations.

All that we had analyzed regarding EFG delivered on Finom Group's positive outlook for the U.S. economy as well as the S&P 500 (SPX). As it pertains to global trade relations; it took the bulk of 2019 before U.S./China trade relations cooled and an agreement was found, which should culminate with a phase-1 trade signing in the first week of January. This signing and de-escalation of trade tensions between the world's 2 largest economies may find global trade volumes having trough in 2019 and before bouncing higher in the first half of 2020.

World Industrial Production posted its first negative YoY print in 2019 and since the last recession. With positive developments on the geopolitical front abound, certain of these resolved or climaxed issues may provide a tailwind for global economic growth in 2020. The issues that plagued the global economy in 2019, which have found some level of resolution are as follows:

- In the U.K., Conservatives won a decisive majority in the House of Commons, a vindication for Prime Minister Boris Johnson’s plan to withdraw from the European Union (EU) on January 31, 2020. After withdrawal, the U.K. would then have 11 months under existing trade arrangements to negotiate new trade terms with the EU.

- The leaders of the U.S. House of Representatives announced an agreement in principle with the White House on a revised North American free-trade agreement (the U.S.-Mexico-Canada Agreement, or USMCA).

- President Trump signed off on a “Phase 1” trade deal with China. Although it is limited in scope, the agreement includes important provisions to maintain global economic growth—including suspension of U.S. tariffs threatened for December 15 and possible rollbacks of existing tariff rates by up to 50% on $360 billion of Chinese imports—in exchange for China agreeing to specific amounts of U.S. agricultural purchases.

All 3 of the aforementioned issues were headlines in early December and since that time the equity markets have surged to record high levels.

All Things S&P 500

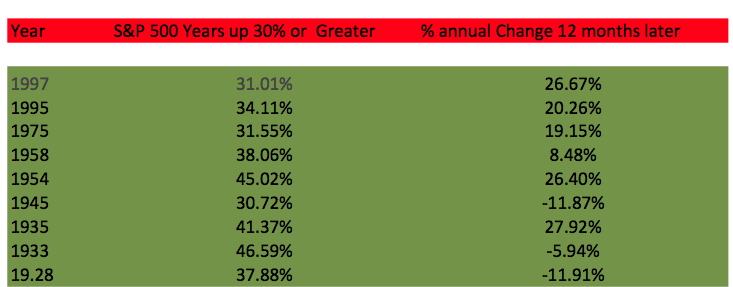

The S&P 500 put in another strong, recording setting performance in the past trading week. For the week, the benchmark index rose .58% and closed the week at 2,940. As it stands and heading into the final 2 trading days of 2019, the S&P 500 is up 29.25% year-to-date and is just 19 points away from gaining 30% in 2019. If in the final 2 days of the trading year the S&P 500 does gain 19 points and 30%, it will be the first time it gained 30% or more since 1997. (Ex-dividend)

While there are many media pundits and Perma bears that will denigrate the 2019 bull market for its multiple expansion centerpiece of growth, one shouldn't be fighting price as price is truth in the market. What we aim to better understand and anticipate is what comes next. We can't change the past any more than we should compensate for it in the future. It's with that in mind and looking forward to 2020 that we recognize what has persisted for the last 2 months or so, overbought and overextended market conditions.

In suggesting, firstly, the S&P 500 and peer indices are overbought it is done so under the premise of also recognizing a healthy bull market. We can validate the health of the bull market based on the percentage of stocks trading at or above key moving/exponential averages. As such, the following chart not only certifies the broad-based market rally but highlights overbought conditions that usually are found to relieve upward pressure near-term.

Whether its the 20, 50, or 200-EMA we look at, all 3 exponential moving averages find the percentage of stocks trading above these averages at levels that usually coincide with a near-term market pullback. Charts are black and white; they indicate what happened in the past but don't guarantee a repeat of history, even if that history is a single calendar year. Nonetheless, it's the probabilities that loom large and beg of risk management given the market internals/breadth noted in the chart. We need more you say? We "gots" more!

The bull market is intact and should remain intact unless an unforeseeable, exogenous event should undermine consumer sentiment and consumer spending. The aforementioned are the pillars of the U.S. economy. With investors believing the consumer is strong and trade issues are being resolved, the S&P 500 has rallied some 9% above its 50-DMA. It has accomplished this feat of strength with great breadth and strength as well. The S&P 500 is now extremely overbought according to the latest Relative Strength Index reading (RSI > 80).

As shown in the bottom box of the chart, the RSI is now at levels that suggest a pullback, then at least one more push higher possibly. Once again, this is an annual chart of the S&P 500 and daily RSI which does denote the high probability of a pullback near-term. How much of a pullback is the only question that likely remains.

It's been a strong 2019 for the S&P 500 to point out the obvious. But what might not be as obvious is the percentage of days for which the S&P 500 was positive and how that compares to past years. (Chart from Bespoke Investment Group)

As shown in the chart above from Bespoke Investment Group, the index only needed to trade higher on 59.3% of days to generate a 29% gain. But positive days occurring 59.3% of the time in a trading year is actually a rarity. Only 5 other years since 1928 have seen up days more consistently with the most recent coming in 1995 when 61.9% of all trading days were positive. A closer look at the chart tells us that any year that has been found with this percentage of up days (59% or >) is always followed in the next year with a lesser percentage of up days. Something to be aware of as we look forward to 2020.

The final day of the trading year is likely on the mind of the investor/trader community. For the Nasdaq (NDX), it hasn't been a good day over the last 19 years. Last-minute tax-loss sales, a desire to start with a clean slate; who knows exactly the answer, but the last trading day of the year has turned bearish over the last 19 years. (Traders Almanac)

Since 2000, the Nasdaq has the worst record, down 15 of 19 years after advancing every last trading day of the year from 1971 to 1999. The Russell 2000 (RUT) has one additional gain for a record of 14 losses in 19 years. The S&P 500 and Dow Jones Industrial Average (DJIA) are only slightly better. Average declines on the day range from 0.43% to 0.19 percent. As always, the averages speak to probabilities and encourage investors to anticipate a possible negative day for Wall Street on December 31st.

Heading into the coming trading week, markets are overbought, found with strong sentiment and vastly improved positioning/exposure.

Wait a second, the chart from Nomura has no probability of being accurate. Do the math folks. This chart has been popularized through the previous trading week because of the hyperbolic move denoted in CTA positioning off to the left side of the chart. The reality is that if we apply the basic mathematical principles it suggests that this investor community essentially acquired some 17% of the S&P 500 over the last month. That is, by all accounts, an impossibility.

The latest AAII survey identifies bullish sentiment having modestly fallen, but remaining above the historical average of 38.

The AAII survey is in the top 90th percentile as of the latest reading. We shouldn't become overly concerned, however, and why? Historically, all the sentiment significance comes from low readings, which are bullish, but the high readings give too many false signals as it pertains to a contrarian market indicator. Based on the chart below from Renaissance Macro, 8 of the 49 sell signals worked on 13-week forward returns. That's a pretty lousy contrarian indicator on a percentage basis (14%).

Of no lesser consideration, the CNN Fear & Greed Index is found with extreme investor sentiment. Combined with the AAII survey, these sentiment readings might lend themselves to agree with our market internals/breadth indicators and suggest a near-term market pullback in early 2020 even if not this coming week. A healthy bull market is not just defined by market internals/breadth, but by intermittent pullbacks/drawdowns.

As we recant the year that was and would appreciate the S&P 500 achieving a 30% gain in 2019, by Tuesday of this coming week we'll see if that is accomplished. Beyond Tuesday, however, we'll also have to wait and see when the market pulls back and by how much. The market liquidity regime has once again proven to defy a countertrend market move in Q4 2019, as it did in Q4 2018. When the calendar year turns a new, investors will again refocus on "valuation" and the economy. Like a market pullback, it's not a matter of "if" valuation matters but "when".

Moreover, the GAPS! Just knowing the market will inevitably consolidate its gains and work off overbought conditions isn't enough. In an algorithmically charged market, predicated upon low liquidity, when a pullback ensues it can be fed by algorithms. These programmed trades are often keyword and/or level seeking. Given the dynamic features and operations of an algorithm, it should be noted that there are 6 open gaps in the S&P 500 chart as shown below:

The first 5 gaps to the downside don't prove too worrisome. If those 5 are filled, the S&P 500 would have retraced back down to roughly 3,050, nearly 190 points lower or roughly 7 percent. We'd likely see the VIX spike up and above 21 during such a drawdown in the S&P 500 This would prove a healthy correction and likely bring about a strong opportunity to pounce for long-term investors whom have missed much of the 2019 rally. The last gap fill would find the S&P 500 fall down to roughly 2,948, or another 100 points. We'd be of the opinion that many investors would start to worry, even panic at the 7 percent drawdown level and possibly provide a self-fulfilling 10% correction that finds all gaps filled. This is not a forecast, but rather an examination of the possible outcomes.

To further develop the "fill the gaps" conversation, as most gaps do indeed get filled, Mark Minnis (Finom Group member) offers the following chart and commentary on gap fill time frames and probabilities.

"Mind the gap! How long do you have to wait for an SPX gap to fill? The average is 33 business days, but the distribution is very skewed. 50% of gaps filled in 7 business days. 75% of gaps filled in 35 days. 9% of gaps currently unfilled. Data from March 29, beg bull market."

As offered, there is a high probability that the majority if not all the gaps in the chart positioned get filled in the not too distant future. "Just be aware... and think of how to best prepare... in order to avoid the scare."

For the coming week, the weekly expected move has risen from $28/points last week to $35/points, with implied volatility (VIX) rising.

Economic Data of the Week

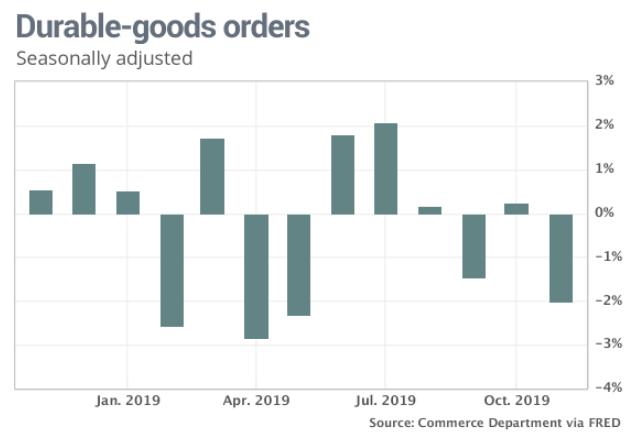

Orders for durable goods fell 2% in November, marking the biggest decline since May. Economists had expected a strong 1% rebound in durable-goods orders in November as a result of the end of the General Motors GM strike. But orders were dragged down by a major decline in defense aircraft combined with a small drop stemming from Boeing’s ongoing issues with the 737 MAX airplane design.

Orders in October were lowered to a 0.2% gain from the prior estimate of a .5% increase.

Looking beyond the key issue of the 737 Max, there was a bright spot in the Durable goods data. Orders for core capital goods posted a second straight monthly gain. This is a proxy for business investment. Capital goods orders rose slightly on a 1-yr basis for first time since June.

So does this mean that CAPEX spending will perk back up in 2020? Here's how Renaissance Macro answers that very question given the their data tracking:

"Capex outlook is no great shakes, but looking at our latest tracker of regional PMIs, a bottom might be in place. Expect core durables to pick-up in H1 2020. Note that conditions never got as bad as they were in 2015-16."

Renaissance Macro Research data suggests a pick-up in Durable goods and CAPEX spending in early 2020. Their data tracking dovetails nicely with the CAPEX outlook from Cornerstone Research's Nancy Lazar. She is of the opinion that real CAPEX will likely reaccelerate to 4% by Q4 2020, led by tech. Supports include lagged impacts of lower BAA yields, healthy corporate profit growth, and a softer dollar. Improving business confidence should also help, as the trade war becomes less of a headwind.

From Lazar's chart above, we can see that real CAPEX has moderated lower since late 2017, given the geopolitical climate and trade wars. Looking at several recent PMI and CEO surveys however, their are clear signals that support both noted research firms' outlook for CAPEX gains in 2020.

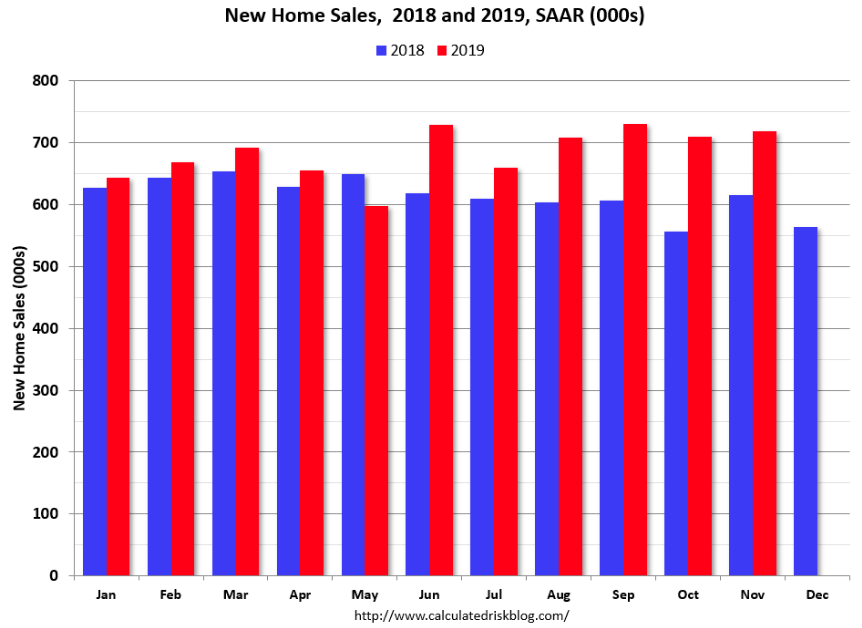

Another key industry report from the housing sector was delivered this past trading week. The housing market has rebounded strongly in 2019. New home sales for November were reported at 719,000. Sales for the previous 3 months were revised down, combined. Sales were above 700K SAAR for four consecutive months, and in 5 of the last 6 months, marking the best 6-month stretch since 2007.

Sales of newly-constructed homes in the U.S. increased 1.3% on a monthly basis in November. Sales in November were up 16.9% year-over-year compared to November 2018. Year-to-date (through November), sales are up 9.8% compared to the same period in 2018. The comparison for December is easy, so sales will likely be up double digits in 2019 compared to 2018 – a solid year for new home sales, according to Bill McBride.

The government estimated there was a 5.4-month supply of new homes available for sale, up slightly from October’s 5.3-month supply. The supply of new homes last peaked at the 7-month level back in December 2018.

Housing sector data has remained very healthy/strong since the spring and it looks like the strength has the ability to persist into the 1H2020 period, and as long as mortgage rates and the unemployment rate remain low while wages are rising. But for a greater outlook on the housing sector in 2020, we encourage Finom Group members to take their lead from Logan Mohtashami. Mr. Hohtashami has had a consistently strong track record when it comes to forecasting yields/rates and housing sector data on a YoY basis.

"The monthly supply spike in housing last year that created excess inventory has been coming down to a more acceptable level, which will facilitate growth in housing starts in 2020. Lower mortgage rates did their thing as new home sales picked up. In fact, in May of 2019, I took the housing market out of the penalty box, which means we are back to the same slow and steady cycle for housing.

Existing Homes Sales

- For 2020, I am looking for sales to stay with a range of 5,210,000 – 5,470,000 with not much changing on the inventory or sales front unless the 10-year yield breaks over 2.62%. The housing market has a rate of growth issue when the 10-year yield gets above 2.62%, as we have seen twice in this expansion. The good news is that this means the economy is better.

New Home Sales & Housing Starts

- The most critical housing data line we have in America got a lot better in 2019.

- Monthly Supply, which looked headline recessionary, got back down to a level that can promote slight growth for housing starts. It wasn’t just higher mortgage rates in 2018 that slowed growth. We also had a lot of uncertainty with the trade war tap dance and the Fed back then.

- For the new home sales market, I expect a 2.3% – 4.7% growth next year. Everyone needs to be mindful of rising yields in this sector.

- Unlike the existing home sales market, which didn’t see a monthly supply shock spike, the new home sales market is sensitive to higher yields.

- Unlike in the earlier years of the expansion, when the housing market had a low bar with which to compare future sales and starts, that low bar is rising.

- If you want growth in housing starts, we will need a combination of more new home sales and monthly supply to stay below 6.5 months. For 2020, as long as yields remain low, this can happen in a slow but steady fashion.

With a positive outlook on the housing sector, as rates remain low and productive for economic growth, jobless claims remain quite low historically and were adjusted lower last week once again. Initial jobless claims fell by 13K to a seasonally adjusted 222K in the week ended Dec. 21, the government said Thursday.

While seasonally adjusted claims have moved lower over the past couple of weeks, the four-week moving average has continued to grind higher for its third consecutive week. With a reading of 213K rolling off the average and replaced by this week’s 222K reading, the four-week moving average now sits at 228K. That is the highest level for the moving average since mid-February when it was 229.5K. While just 1.5K off of the 52-week highs for the moving average, it is also 26.5K off of the 52-week low of 201.5K from April. That is the furthest from the 52-week low that the moving average has been since September of 2017 when it was 37K above its 52-week low.

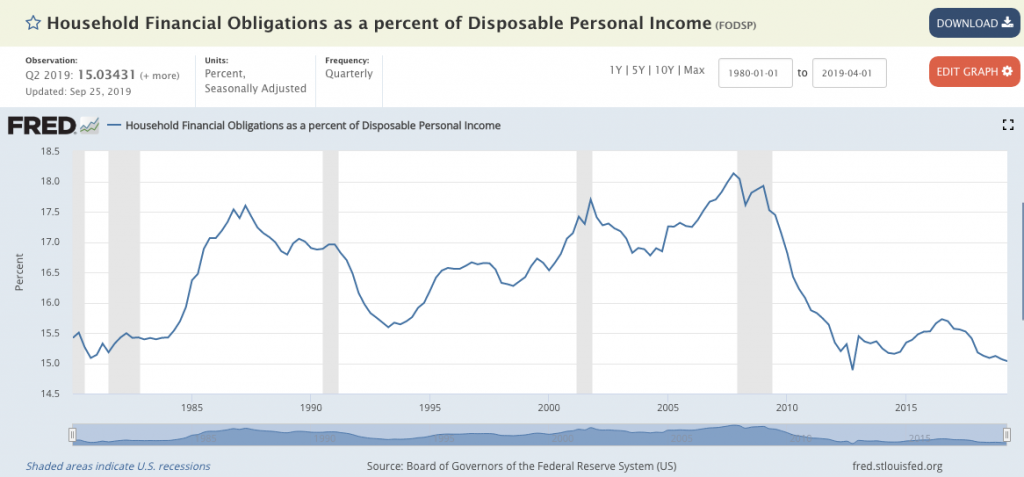

Despite the recent rise in the 4-week moving average of initial jobless claims, the overall picture of the labor and employment market remains one of strength. This continues to provide the backdrop or fuel for increased consumer spending going into 2020. Rates remain low, wages remain on the rise and especially amongst the lower-income level employee demographic. But as it pertains to Finom Group's economic outlook, one chart/metric stands tall and above all others. Recall from our December 15, 2019, Research Report the following:

"The chart below is possibly the most important and relevant chart that defines the strength of the consumer and underlying support of economic growth for the foreseeable future."

"Household financial obligations (debt) as a percent of disposable income is at 60-year lows. The consumers balance sheet is strong and found with rising wages in a low inflation environment where credit is free-flowing."

While we have offered this economic metric on the household balance sheet throughout 2019, it is only recently that others have taken notice of its great importance. Chris Ciovacco of Ciovacco Capital recently featured household debt as a percentage of disposable income in his latest YouTube video. In the half-hour-long video he discusses how the average household has deleveraged their balance sheet since the Great Financial Crisis. The following two charts/slides were peppered throughout the video:

Based solely on this key economic metric surrounding disposable income and the consumer, bull markets have a tendency to be strong and lasting, without a recession. The period from 1982-1987 found a strong bull market and a recession did not take place until 1991. In the mid-90s disposable income was high compared to debt service again and found with the market surging as shown in the following chart:

We can't say enough about the strength of the consumer balance sheet and its typical correlation with a bull market. Having said that, in order to find consumer spending even stronger in 2020, the Personal Savings rate will likely need to moderate lower. We know that sounds like heresy, but the reality is that it can be afforded based on the household/consumer balance sheet data throughout much of this expansion cycle.

For the coming week, the economic data calendar intensifies.

Consumer Confidence and the latest reading on ISM manufacturing are likely to be the standout data points of the week. After a disappointing ISM and Consumer Confidence reading last month, investors would probably like to see a rebound in both metrics to solidify their outlook for 1H2020.

Fund Flows

Due to the holiday-shortened week last week, Lipper Weekly FundFlow Insights data has yet to be published. Having said that, there are other fund flow points of interest to discuss. Much of what we aim to discover from fund flows at the end of 2019 can be found in the latest Bank of America fund flow tracking.

Additionally, the latest from Lipper and the Wall Street Journal on equity fund flows in 2019 was not a net positive, as we would surmise given the YTD outflows we've consistently tracked. In 2019, there was $135.5 billion in equity outflows from ETF’s & mutual funds. A key takeaway from this statistic is that there is a great deal of capital on the sidelines or in other asset classes that could seep into the equity markets in 2020.

Typically, bull markets don't end with such outflows. Bull markets end when fund flows are overwhelmingly positive.

More recently, retail investors posted a positive inflow to equity funds during the week ended Dec. 26, only the third since late in the second quarter of 2017, according to data from EPFR. The move came amid apparent profit-taking on the part of institutional investors who posted their largest weekly outflows from U.S. equity funds in more than a year, one week after posting the largest inflow in three months.

“While the latest outflows from US Equity Funds were eye-catchingly large, the fact this group recorded its second retail inflow in the past two months is more significant,” given the consistent retail outflows seen in recent quarters, according to Cameron Brandt, director of research at EPFR Global.

"There’s still a lot of money on the sidelines,” Jeffrey Kravetz, regional investment director at U.S. Bank Private Client Reserve. “Retail investors have been cautious this year,” he said, adding that last December’s sharp downturn drove this caution.

The fund flows you’re seeing is that they’re probably looking at their portfolios and statements and realizing that it’s been a good year and not wanting to miss out."

Earnings Outlook: Q4 2019 & Beyond

On a week-to-week basis, not much has changed or been updated for the Q4 2019 earnings season by FactSet. However, when we look at the firm's FY2019 EPS growth for the S&P 500 it shows a positive year for EPS growth, even if only at .3 percent.

Despite the flat earnings growth, 2019 revenue Growth will come in at +3.8 percent, according to FactSet. That is above the 10-year average annual revenue growth rate of 3.3%. This is an important fact that didn’t get much attention in 2019, and a reminder to look at all demand-side data before making capital allocation decisions.

FactSet still holds to an outlook of -1.3% YoY EPS declines in the Q4 2019 period. For 2019, the Energy sector is expected to report the highest (year-over-year) earnings decline of all eleven sectors at -27.7 percent. Lower oil prices are helping to drive the decline in earnings for the sector, as the average price of oil in CY 2019 to date ($56.85) is 12% lower than the average price of oil in CY2018 ($64.95). At the sub-industry level, four of the six sub-industries in the sector are projected to report a decline in earnings: Integrated Oil & Gas (-36%), Oil & Gas Refining & Marketing (-30%), Oil & Gas Exploration & Production (-21%), and Oil & Gas Equipment & Services (-8%). On the other hand, the other two sub-industries in the sector are expected to report earnings growth: Oil & Gas Drilling (163%) and Oil & Gas Storage & Transportation (12%).

Possibly more importantly, however, is the outlook for 2020 EPS growth. FactSet expects EPS to rebound strongly in 2020.

- For Q1 2020, analysts are projecting earnings growth of 5.4% and revenue growth of 4.4%.

- For Q2 2020, analysts are projecting earnings growth of 6.9% and revenue growth of 4.9%.

- For CY 2020, analysts are projecting earnings growth of 9.7% and revenue growth of 5.5%.

What has changed in Refinitiv's Q4 2019 EPS growth forecast? Unfortunately, it has worsened ever so slightly. Last week, Refinitiv’s forecast called for Q4 EPS to decline by .2% YoY. Here's there latest update as follows:

- The estimated earnings growth rate for the S&P 500 for 19Q4 is -0.3%.

- If the energy sector is excluded, the growth rate improves to 2.0%.

- The S&P 500 expects to see share-weighted earnings of $334.2B in 19Q4, compared to share-weighted earnings of $336.2B (based on the year-ago earnings of the current 505 constituents) in 18Q4.

Refinitiv, like FactSet, denotes the drag on EPS growth from the energy sector. The energy sector has the lowest earnings growth rate (-34.7%) of any sector. It is expected to earn $13.6B in 19Q4, compared to earnings of $20.8B in 18Q4. Four of the 6 sub-industries in the sector are anticipated to see lower earnings than a year ago. The oil & gas drilling (-81.5%) and oil & gas refining & marketing (-44.7%) sub-industries have the lowest earnings growth in the sector. If these sub-industries are removed, the growth rate declines to -31.5 percent.

We've questioned the revisions of these firms recently and given the surge in crude oil prices from November through December. The current price per barrel of crude is now some 20% above the same period a year ago, which should prove a tailwind for the energy sector Q4 EPS and revenue results.

Investor Takeaways

Wall Street strategists' and analysts' forecast are littered with errand statements and often prove unreliable or even useless. If we can offer one suggestion to our members it's this: "Don't get into this business of forecasting the market over the next 12-month period." Having said that, also keep in mind that just because a forecast can prove accurate, the path toward the end-result/target may prove altogether problematic and therefore no more relevant than if the forecast had been wrong.

Based on some calculations from Paul Hickey of Bespoke Investment Group, he summarizes the median forecasts and market returns since 2000.

- The median forecast was that the stock index would rise 9.8 percent in the next calendar year. The S&P 500 actually rose 5.5 percent.

- The gap between the median forecast and the market return was 4.31 percentage points, an error of almost 45 percent.

- The median forecast was that stocks would rise every year for the last 20 years, but they fell in six years. The consensus was wrong about the basic direction of the market 30 percent of the time.

- Mr. Hickey found that the forecasts were often off by staggering amounts, especially when an accurate forecast would have mattered most. In 2008, for example, when stocks fell 38.5 percent, the median forecast was typically cheery, calling for an 11.1 percent stock market rise. That Wall Street consensus forecast was wrong by 49.6 percentage points, and it had disastrous consequences for anyone who relied on it.

After such a strong market performance in 2019, indications are that the market has overheated and will probably enter 2020 in a similar manner as it entered 2018. When we compare the optimism in market sentiment concluding 2019 and compare it with the pessimism of 2018's conclusion, we can see they are close to even.

As noted previously, the risk of a correction remains elevated, as we move into the New Year. That risk would only increase should the market march higher in the coming weeks. Price momentum has accelerated to levels that usually produce a corrective period. Again, this is not a positioned statement that should frighten investors, but rather prove to accelerate the risk management and planning process for the coming year.

Beneath the surface, the 2019 equity market rally is seemingly being driven by a handful of factors offered in the following bullet points:

- Fed easing

- Ebbing fears of recessions

- Trade truce of sorts.

It is unclear how long these factors will remain in play, as it seems difficult for all 3 to coexist. Fed easing was driven by escalating trade tensions and concerns about growth earlier this year, while the bar for a shift in Fed policy is high, a sustained trade truce against a backdrop of moderate growth could potentially lead the parties at play to change their tune.

One other driver of this rally that achieves little attention has been an increase in liquidity. M2 money supply growth, which includes cash and checking deposits, as well as savings deposits, money market funds, and other time deposits, has been steadily accelerating since the end of the summer.

Equity markets are forward-looking, and pricing in the acceleration in economic and profit growth tend to accompany an expanding money supply. Furthermore, an expanding money supply oftentimes coincides with easier central bank policy, making equities an increasingly attractive investment relative to bonds.

The year ahead will be a politically charged year. For the economy, that may prove a benefit as the incumbency desires reelection. Given this base desire, a recession is highly unlikely. Only 2 presidents since World War II, Democrats Harry Truman and Jimmy Carter, have run for reelection in the same year as a recession. While Truman won and Carter lost, history suggests an economic slump would damage President Trump’s chances in what will already be a tough 2020 race.

Since 1928, only 4 of the 23 presidential election years have coincided with negative S&P 500 Index returns (Table below). Two of those 4 years occurred during U.S. economic depression (1932) or recession (2008). A third occurred in 1940, while the U.S. was still recovering from the Great Depression. This suggests that as long as the U.S. economy is expanding and international events do not interfere, equity markets can rise during presidential election years.

Equity markets may become more volatile during the lead up and through Super Tuesday, which is March 3, 2020. Democrat primaries will aid in the surveying the landscape of the presidential election cycle by investors, who will aim to price in the probabilities from the primary season. Having said that, even if you did know who’s going to be president, you don’t know who’s going to control Congress. This branch of government, Congress, plays a pivotal role in shaping the economy. Keep in mind all 435 House seats and roughly a third of Senate seats are on the ballot in November 2020.

We believe there are 3 potential scenarios for the markets in 2020:

- Melt-up’ scenario, which could significantly benefit riskier assets like equities. This is statistically the most likely scenario.

- Balanced view that mixes growth optimism with election uncertainty over the summer. This is the most likely of the 3 market scenarios based on the outsized gains in 2019.

- Negative performance scenario where growth falters and geopolitical risks rise. We believe this is the least likely of the 3 market scenarios.

And while we have asked investors/traders to look beyond the exercise of forecasting the next 12-month period in favor of longer-term market and economic trends, here are the Wall Street price targets for the S&P 500 in 2020.

Thank you for tuning into this week's Research Report and we hope that you have a safe, fun-filled New Year. We look forward to what 2020 has in store for the economy and markets, as we deliver your financial market analysis on a weekly basis.

Comments

Log in or sign up to join the conversation.