November Taper-Trial Balloon Or Reality?

Equities are clawing back Friday’s losses despite weekend rumors that corporate and capital gains taxes may rise under a new Biden proposal. Further, the market appears to be brushing off concerns that a taper timeline aiming for November seems more like reality than a trial balloon. Comments from various Fed speakers early this week will shed more light on any potential change to policy. Crude oil is trading back over $70 a barrel as tropical storm Nicholas threatens already battered gulf coast oil/gas production facilities.

What To Watch Today

Economy

- 2:00 p.m. ET: Monthly budget statement, August (-$175.0 billion expected, -$200.00 billion during prior month)

Earnings

Post-market

- Oracle (ORCL) is expected to report adjusted earnings of 97 cents a share on revenue of $9.77 billion.

Politics

- Congressional Democrats will formally unveil their tax plan as soon as today and a draft has already leaked. The proposal is estimated to raise $2.9 trillion in new taxes from wealthy Americans and corporations and will be discussed in committee hearings today.

- President Biden is headed West today for a two-day trip that will take him to Idaho, California, and Colorado. He’ll be focused on wildfires with a stop at the National Interagency Fire Center as well as politics with a campaign stop for California Gov. Gavin Newsom ahead of the recall election tomorrow.

- U.S. Secretary of State Antony Blinken will be in the hot seat with his first appearance before Congress since the United States’ withdrawal from Afghanistan. Blinken is expected to face some of the most aggressive questioning of his career during a hearing scheduled for 2:00 p.m. ET.

Courtesy of Yahoo

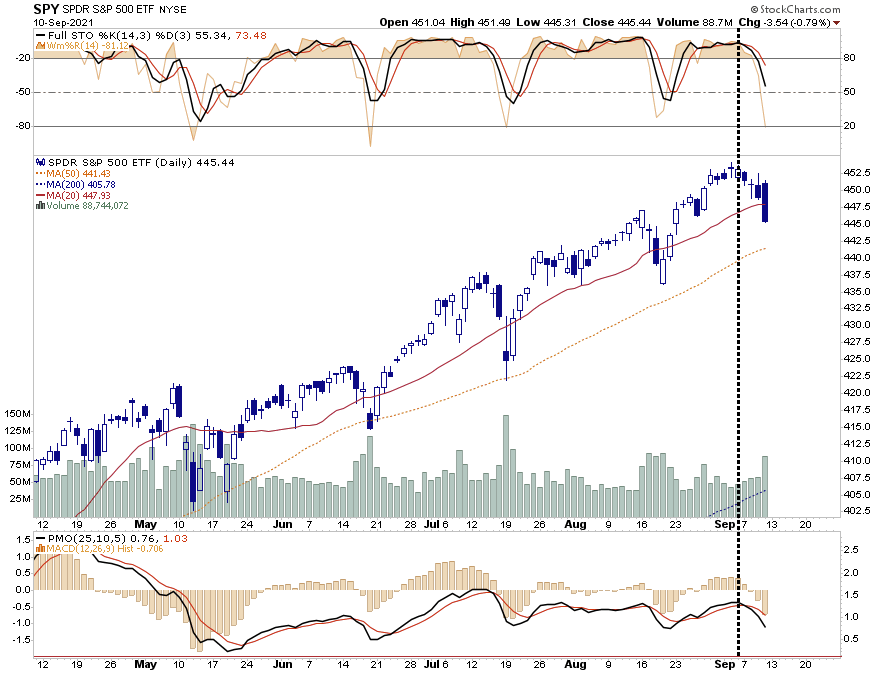

Dead Cat Bounce

Market set to bounce at the open this morning. As we noted in this past weekend’s newsletter:

“That correction started on Monday with the week ending in 5-straight down days which is the worse slide since February.

However, while that sounds terrible, the total decline for the week was just -1.69%. Yes, that’s it, less than 2%. While CNBC probably ran their “Markets In Turmoil” segment, traders huddled over candles and incense chanting incantations at the Fed for more accommodation.“

On a very short-term basis, the market is oversold enough for a tradeable bounce. However, as we concluded:

“With sell signals in place, volume rising, and breadth weak, a retest of the 50-dma early next week will not be a surprise. The question will be whether traders show up again, as they have done every other time over the last 6-months to ‘buy the dip?’”

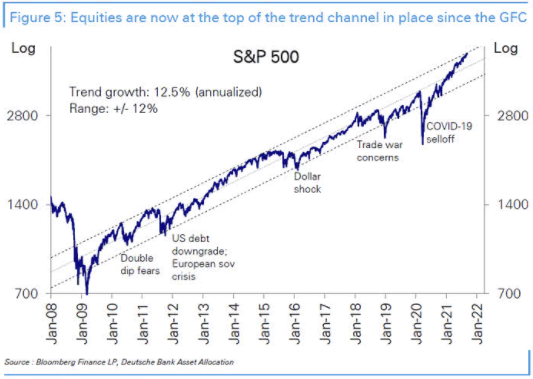

Trend Channel

Since the lows of the “Financial Crisis,” the market has remained confined to a well-defined “trend channel.” As BofA noted on Friday stocks have now retraced from the break of the lower bound to the top of the channel.

At some point, the market will violate this trend channel in one direction or the other. Given the length of the bull market advance from the “GFC” lows, current valuations, and slowing economic growth, logic would suggest it will be to the downside. However, the markets have a very interesting way of surprising everyone.

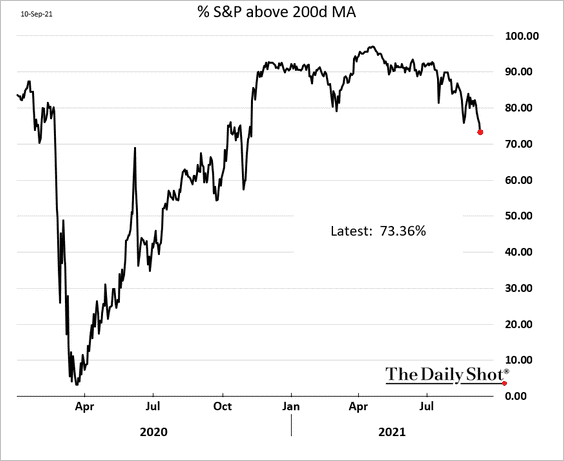

A 10% Correction Call Is Broadening

“You should always be expecting a 10% correction. If you’re investing in equities, you should be prepared for that at any time,” Morgan Stanley‘s Chief Investment Officer Mike Wilson told Yahoo Finance Live. “The bottom line for us… is the risk reward is not particularly great at the index level from here, no matter what the outcome is. That’s why we don’t have any upside to the S&P for the rest of the year.” – Yahoo

There is clear evidence of deterioration in the markets as of late. With markets extended and market breadth weakening the risk of a 10% correction has clearly risen.

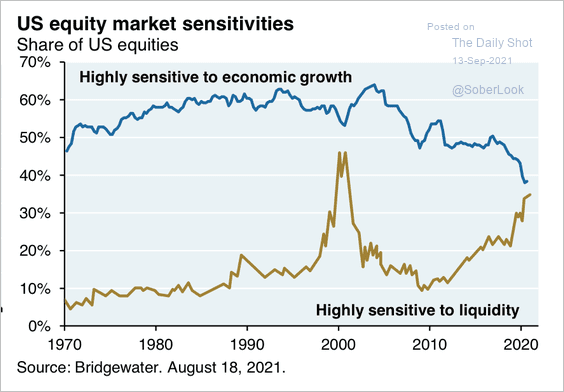

But the biggest risk is in the contraction of liquidity which stocks have been more sensitive to over the last decade rather than economic and earnings growth.

That liquidity flow is now at risk.

The Fed Has Spoken

Often the Fed leaks policy changes or sends trial balloons via the media. They tend to have their favorite media outlets and authors in which to do it. Nick Timiraos from the Wall Street Journal is a current favorite. His latest article, Fed Officials Prepare For November Reduction in Bond Buying, lays out a timeline for the Fed to taper QE. While the article is not an official declaration, it will become the market assumption until we learn more at the September 22nd Fed meeting.

Per the article:

While they are unlikely to do so at their meeting on Sept. 21-22, Fed Chairman Jerome Powell could use that gathering to signal they are likely to start the process at their following session, on Nov. 2-3.

Under the plans taking shape, officials could reduce those purchases at a pace that allows them to conclude asset buying by the middle of next year.

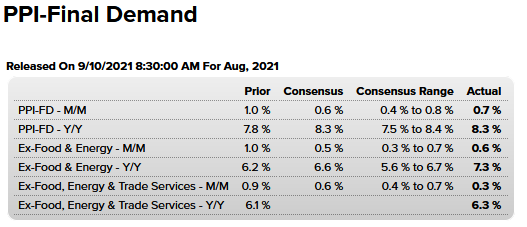

PPI

The producer price index (PPI) is slightly higher than expectations. PPI, while not as well followed as PCE or CPI provides unique insights. First, PPI tends to lead CPI. Higher or lower input prices often eventually make their way to changes in the prices of goods companies sell, i.e. CPI. Second, other than labor, input costs are often the second largest expense for companies. Given rising wages and PPI, producers and other companies dependent on labor and commodities are likely to feel margin pressure.

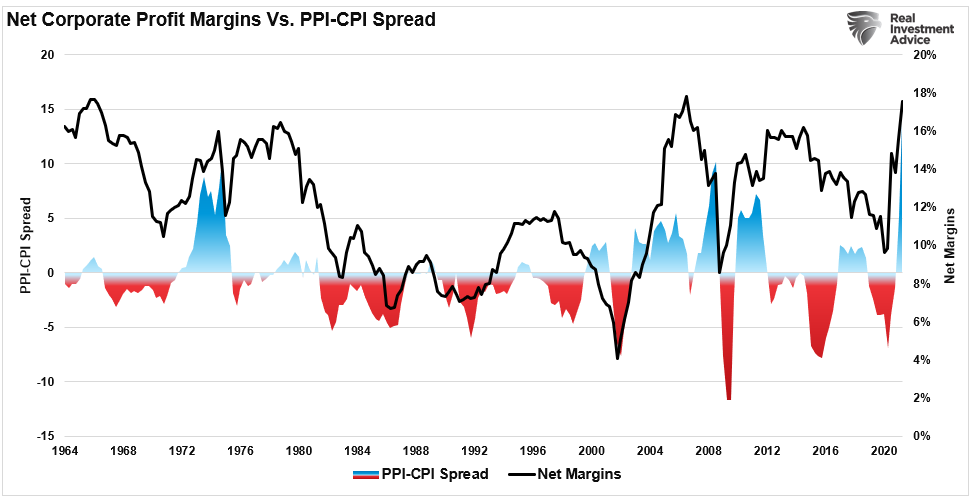

Inflation is becoming problematic for the Fed mainly if these pressures are not as “transient” as hoped. Higher wages are corrosive to both earnings and margins. As shown below, strongly rising producer prices are initially good for profit margins until inflation can not get passed along to consumers. Such is the case currently, with the most significant historical spread between PPI and CPI.

With supply chain disruptions looking to last longer than expected, the Fed is trapped between supporting a slowing economy and fighting inflation.

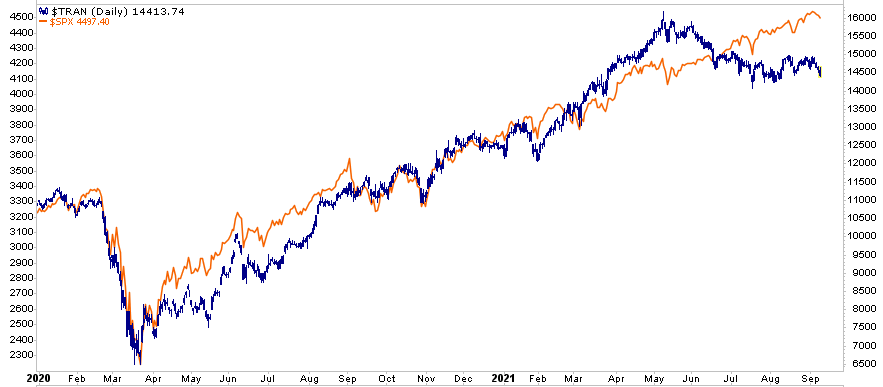

Dow Theory

Dow Theory, a once-popular way of evaluating the market, is well over 100 years. The theory follows that transportation stocks lead the broader markets. Per Business Insider: “The general idea is that both averages, over time, should move in tandem, given that the transportation average represents companies responsible for the movement of goods across the country. For that reason, it should serve as a leading indicator.” Many question the value of the theory today due to the tremendous technological progress. However, the fact of the matter is we still consume goods that must be shipped.

The graph below shows the Dow Transportation Index is down nearly 10% since May. At the same time, the broad market S&P 500 has steadily risen by 10%. For those following Dow Theory, this is a warning.

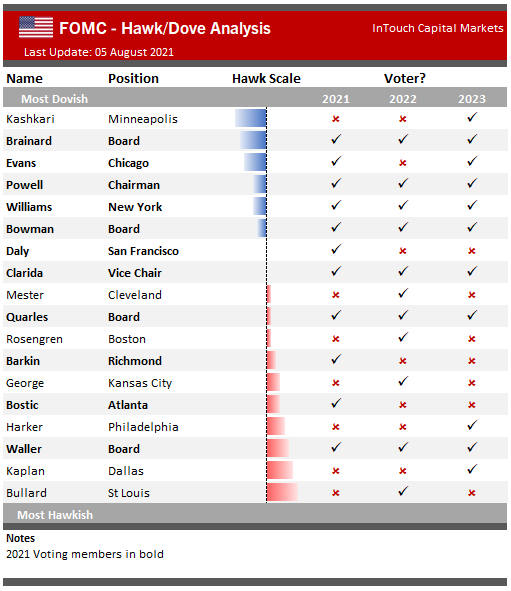

Will They Taper?

The chart below, courtesy of InTouch Capital Markets, breaks down the Federal Reserve Board by the degree to which they are policy hawks or doves. The graph also shows their respective voting eligibility by year. There are about twice as many hawks as doves, but three of the four most influential voters are dovish (Powell, Williams, and Brainard). The other, Vice-Chair, Richard Clarida, is neutral. Five of the six doves vote in 2021, while only four of the ten hawks vote in 2021. Despite the hawkish overtone from many Fed speakers, this chart points to a more dovish policy stance going forward. We will have much more on this graph and its implications in our next article this coming Wednesday.

Disclaimer: Click here to read the full disclaimer.