Netflix: Valuations, Competition, And Questionable Accounting Point To Potential Crash

Netflix (NFLX) may undergo one of the greatest collapses, and even bankruptcies, in stock market history.

It is not only the fierce and increasingly-powerful competition, subscriber growth hurdles, and enormous valuations that could cause Netflix's rapid downfall each on its own; but also, and even more devastating, it is the tremendous (and mostly hidden) debt, extremely weak financials, insider selling, and numerous accounting "red flags" that potentially make Netflix one of the best short opportunities ever.

To be fair, Netflix (NFLX) is an exceptional service and still a top source for video streaming and content. It "disrupted" the media industry and was a leader in this new form of video technology. Netflix should be commended for its revolutionary effects on media and technology as well as its award-winning original content, among other achievements. Partly or mostly due to Netflix, we can now get millions of videos on demand, anywhere we go. Furthermore, the "On Demand" trend in media consumption is relatively still in the early to mid stages, and media companies don't truly know where the future is heading. Many have discussed the trend away from traditional cable, known as "cord-cutting". Interestingly, we may be seeing a shift towards an "a la carte" or "pay per view" model where customers choose specific channels, events, or videos rather than paying for a large package with many channels they don't need.

It is definitely possible for Netflix to succeed. Netflix could very well continue to grow its subscriber base, flourish in its international expansion, and produce more massively-popular and award-winning original content.

Source: SEC, Netflix 10-K

However, just because Netflix is a great service or company doesn't mean it's a great stock. In fact, Netflix (NFLX) is a terrible stock, and here's why:

1) EXTREME VALUATIONS

Netflix has already seen a significant drop its stock price (down over 30% from it's December 2015 high), yet its valuations remain highly inflated and not sustainable.

(Click on image to enlarge)

Source: Finviz

P/E --> With a market capitalization of $39 Billion as of January 31, 2016 (was over $50 Billion), Netflix has a sky-high Price-to-Earnings (P/E) Ratio of 328 and a Forward P/E Ratio of 85. A P/E ratio higher than 30 or 50 is generally too much even for fast-growing technology companies.

P/B and PEG --> Netflix's Price-to-Book (P/B) Ratio is 17.66, and its PEG Ratio is above 10, both extremely high considering these ratios should ideally be closer to 1 or 2. They are exponentially higher due to high investor expectations, but expectations are perhaps too high.

BV/Share --> With a stock price close to $100 per share, Netflix's actual Book Value is far below, at only $5.20 per share. The disparity is huge.

Cash/Share --> Netflix has only $5.40 per share in cash, a very small amount of liquidity and cash needed to run the company or weather a growth slowdown.

2) TINY PROFITS, NEGATIVE CASH FLOW

Though management claims aggressive international expansion and production of original content is to blame for its low Net Income and bottom line, such poor performance cannot continue for much longer without severely hurting the company.

As you can see below, though the number of streaming memberships has grown, this has not translated into higher Net Income.

Source: SEC, Netflix 10-K

Net Income (NI) --> With a $40 Billion market cap and nearly $7 Billion in Revenue, Netflix only generated $122.6 Million in Net Income. It is barely profitable.

Source: Statista

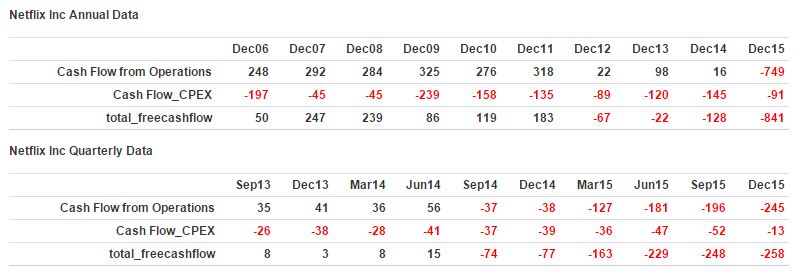

Operating Cash Flow (CFO)--> A well-known "red flag" in accounting and financial analysis, a negative Operating Cash Flow (CFO) is a sign of potential trouble ahead. Netflix's Cash Flow from Operations is -$750 Million (yes, that's NEGATIVE 750 million).

Free Cash Flow (FCF) --> Similarly, Netflix's Free Cash Flow is negative. Another major red flag.

Source: GuruFocus

3) DEBT BURDEN

One of the most disturbing aspects of Netflix's financials is its large and very murky debt accounting.

The company publicly takes pride in its relatively low debt levels (~$2.5 Billion), but mostly fails to acknowledge the massive $10 Billion+ in additional debt that remains in its "Off-Balance-Sheet Liabilities". This means that Netflix actually has a total debt and financial obligations of more than $15 Billion!

(Click on image to enlarge)

Source: SEC, Netflix 10-K, Management’s Discussion and Analysis of Financial Condition and Results of Operations

Management has slyly and cleverly kept the massive debtload off the books in order to make the financial strength and health of Netflix look much better, yet is completely detached from reality. Though management has found clever technical ways to define these liabilities and keep them off the Balance Sheet, such behavior is at the very least questionable if not outright fraudulent.

If Netflix keeps billions of dollars of obligations off the balance sheet, it should likewise also keep its streaming content assets off the balance sheet. But it hasn't; Netflix has managed to hide more than $10 Billion of debt while adding billions of dollars in assets:

(Click on image to enlarge)

Netflix cannot afford new content without taking on more debt. Its debt is growing faster than its profits, and this can't last for long.

4) GROWING COMPETITION

Netflix was the first big winner in the video streaming subscription service, and competition has not yet caught up, but the number of competitors as well as their growth momentum is increasing.

Netflix is a small player in comparison to the other major players in this space - giants like Amazon (AMZN), Google / Alphabet (GOOG)(GOOGL), Disney (DIS), CBS Corp (CBS), Apple (AAPL), and Time Warner (TWX), with Hulu gaining steam and with Facebook (FB) increasingly interested in video content.

Not only does the competition take away some of Netflix's subscriber base, but it creates large bidding wars and increased prices for the video content, which Netflix can barely afford in the first place. On the other hand, giant companies like Amazon (AMZN), with sufficient resources at their disposal can better afford the content and may be able to price Netflix out.

![]()

![]()

![]()

Netflix is left with a big and perhaps insurmountable hurdle: Either it pays exorbitant sums for content and puts itself further into financial distress, or it stays on the sidelines while its content library dwindles or becomes stagnant, leading to loss of subscribers or much slower growth. Lose-lose situation.

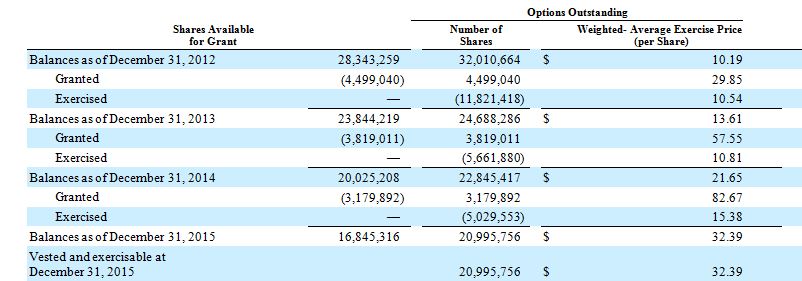

5) MASSIVE INSIDER SELLING & QUESTIONABLE EMPLOYEE OPTIONS COMPENSATION

While Netflix has hovered at or near all-time highs, insiders and very important directors and officers have sold millions upon millions of dollars in stock (see here). Sometimes this is just profit taking, but sometimes it is a sign of a lack of faith in a continued rise in the stock price. If those on the inside, who have a better view of the company's operations and growth opportunities, don't have faith in the stock, why should other investors?

Source: Forbes

Moreover, the insider selling is further muddled by a confusing employee compensation arrangement. Employees and directors are given options as compensation, but somehow those options are being quickly exercised at a cost of nearly a tenth of the share price on the open market and sold for millions of dollars. It's as if the company is creating shares out of thin air and giving them to employees to sell on the open market for ten times the profit.

(Click on image to enlarge)

Management has attempted to appear fair and sacrificing for the good of the company by accepting reduced salaries. But if this options compensation is as shady as it seems, there could be major trouble ahead.

6) WEAK TECHNICALS

After soaring by more than 1000% from its 2012 lows and also being the best-performing S&P 500 stock of 2015, Netflix's (NFLX) parabolic rise is dangerously close to collapsing on itself.

On the long-term monthly chart below, you can see the giant increase in the stock price as well as the significant drop since reaching the all-time high in late 2015. Though it is still uncertain, this looks like it could be a long-term peak or all-time high never to be reached again.

Source: Finviz

On the weekly chart, a similar ominous signal is emerging - what appears to be a topping pattern. In the chart below, you can see a significant support level of $85-90. If NFLX falls below that level, there is plenty of space below. Moreover, though this pattern could bottom out here and continue the uptrend, it is very possible that Netflix (NFLX) is currently undergoing one of two major topping patterns - either a "Double Top" or a "Head and Shoulders". Additionally, the recent top in the stock at around $130 was accompanied by a major "divergence" in momentum. While the stock price was making new highs, the momentum (signaled by the Relative Strength Indicator (RSI) and MACD) was not matching those highs. Such a negative divergence is many times visible near major peaks, right before a big plunge.

Source: StockCharts.com

Conclusion

At the very best, Netflix (NFLX) is highly overvalued with huge expectations to live up to and the best stock performance already behind it.

At worst, it is a company rapidly losing to competition, financially unsustainable, overloaded with debt and a toxic balance sheet, and is potentially manipulating its numbers.

Though I am not calling Netflix a fraud, I am definitely seeing many "red flags" and questionable accounting. At the very least, investors deserve sufficient answers to these major concerns which could quickly drag Netflix into a death-spiral

Simply put, an investment in Netflix (NFLX) is not worth the risk, and the stock is instead a great short candidate. The next few fiscal quarters are critical in the growth or demise of Netflix.

Disclosure: None.

Yoni, you certainly make some valid points here. Seeing the once invincible stock drop 28% year to date is somewhat worrying, but I dont think we've heard the last from this company. What is encouraging is the upgrade from Piper Jaffray this week (Feb 2nd) going from neutral to overweight with a price target of $122 (approximately a 33% in upside based on Tuesday's close). Jaffray shows that too win at stocks sometimes you have to go against the tide.

Excellent post on $NFLX that gives me much to think about. I agree with much of what you said but I think there are some emotional factors that you left out which should not be negated.

1. I think on average, Netflix customers are fiercely loyal compared to other companies.

2. Netflix has a great product which they keep improving upon. Netflix is actually more reliable than my cable provider.

3. Netflix has the first movers advantage. Even $AMZN hasn't made much of a dent and they are giving away their video on demand service free to their millions of prime customers. I get Amazon instant video free, yet I still prefer Netflix.

Really interesting read and though I'm new to this, it's making me think Netflix may not be the sure bet that I thought. That being said, I am one of those fiercely loyal customers you mentioned and I think many others are as well.