Markets: Muddling

Children play in mud, adults get stuck in it. While markets pause for a breather ahead of the US jobs report tomorrow and despite more evidence of progress in US/China trade talks – as President Trump meets China vice-premier Liu at the White House today – or as UK Brexit expectations shift into long delays with new elections, customs union, and second referendum chances. Few look happy to be waiting, as the lack of momentum gives time for economic data, central bank policy, and other politics to matter again. The crushing drop in German factory orders reminds investors that European growth is weak. Italian papers remind them that politics remain ugly. Here are the stories that seemed to grind through the mud of an otherwise volatility-crushing day with emerging markets INR, MXN, TRY moving:

- Italian Politics and Growth– The Italian paper La Stampa reports that the 5-Star movement is ready to sack FinMin Tria and others around the EU elections as the League seems likely to the first party. Di Maio denies he suggested replacing Tria according to Canale 5. May is setting up for trouble as E23bn hole in 2020 budget has automatic VAT trigger as Italian GDP forecasts get downgraded.

- RBI cuts 25bps to 6% as expected – but keeps neutral bias. The vote was 4-2 for the cut and 5-1 on the bias. The new forecasts for FY20 GDP 7.2% from 7.4%, while they also cut the 6M outlook for inflation to 2.4%. Net result was INR lower by 1%

- Mexican Avocados jump 33%. The fear of a border closing moves Hass avocados to MXN390 per 10kg– biggest move since April 2009. Net result MXN off 0.1% still watching 19.1550 support.

- Turkey basted after yesterday’s US VP Pence warnings on the purchase of Russian S-400 missile defense system as “reckless” and “deeply troubling.” Net result TRY off 0.1% today but holding with 5.65 USD resistance

There is some chance for excitement around the US weekly jobless claims and the ECB March policy minutes as they may shed some light on the talk of rate-tiering. FX is barely moving but EUR and GBP remain the focus with EUR 1.12 the pivot for larger troubles today.

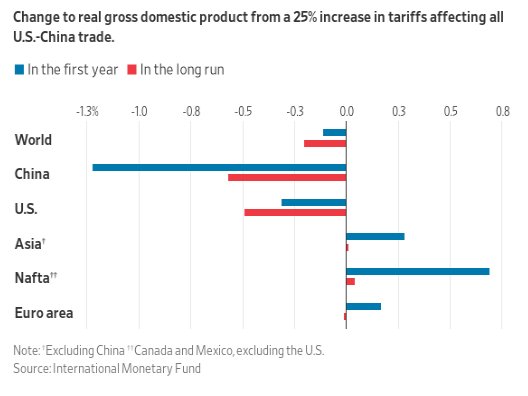

Question for the Day: Is the IMF right about the danger of tariffs on global growth? The report from the IMF yesterday is likely part of the talks today. It argues that a 25% tariff on all Chinese imports would hit US GDP by 0.3-0.6%and hit the world growth by 0.1-0.2%. China GDP would be hardest hit at -0.5-1.5%. The other nations that seem most at risk – Korea and Germany. Markets are quiet and the odds of this report mattering to investors slim in comparison to the jobs report Friday – as that will merit a response to the FOMC outlook, while this tariff story has been like Brexit lingering for months. The IMF chart on the change in growth from the IMF matters as it is clear that the longer it talks for tariffs to be removed, the worse it is for global growth.

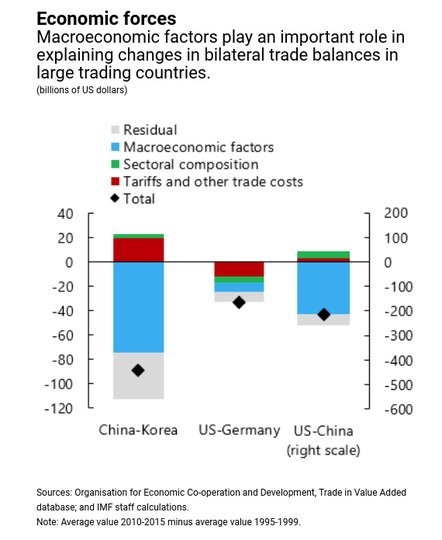

The bigger picture part of the IMF story is about what really drives global trade and its not tariffs but macroeconomics. The issues of monetary policy, fiscal policy, and global supply chains are more important.

What Happened?

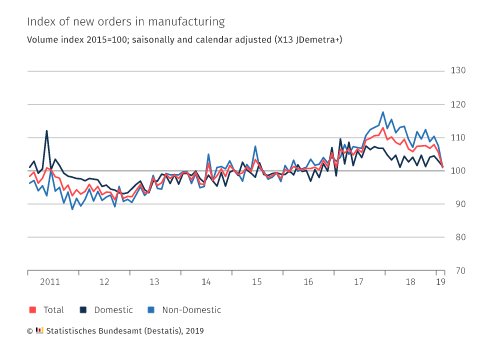

- German February factory orders drop 4.2% m/m, -8.4% y/y after revised -2.1% m/m, -3.6% y/y – weaker than +0.1% m/m expected. January revised stronger from -2.6% m/m. Domestic orders -1.6% m/m, foreign orders -6% m/m with EU orders -2.9% and outside of that -7.9% m/m. Intermediate goods orders -0.9% m/m, capital goods down 6% m/m and consumer goods -3.5% m/m.

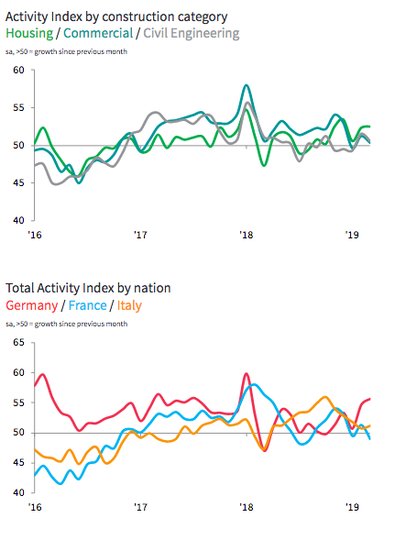

- Eurozone March construction PMI 52.2 from 52.6 – weaker than 52.8 expected. The new orders pace slowed to weakest since August 2018, however, employment was steady holding unchanged from February. France was weaker while Germany and Italy are stronger. Confidence levels were higher, improving from February to June 2018 levels.

- German construction PMI 55.6 from 54.7- better than 54 expected– best in 14-months.

- France construction PMI 49 from 51.3 – weaker than 50.5 expected– biggest fall in orders in 7-months.

- Italy construction PMI 51.2 from 50.7 – better than 50.5 expected– input prices at 1 ½ year lows.

Market Recap:

Equities: The US S&P 500 futures are off 0.05% after a 0.21% gain yesterday. The Stoxx Europe 600 is off 0.25% after 1% gain yesterday. The rival bid for Commerzbank by UniCredit is main story after weaker German factory orders. The MSCI Asia Pacific was up 0.1% in quiet session – China holiday tomorrow.

- Japan Nikkei up 0.05% to 21,724.95

- Korea Kospi up 0.15% to 2,206.53

- Hong Kong Hang Seng off 0.17% to 29,936.32

- China Shanghai Composite up 0.94% to 3,246.57

- Australia ASX off 0.76% to 6,320.40

- India NSE50 off 0.39% to 11,598.00

- UK FTSE so far off 0.4% to 7,387

- German DAX so far up 0.15% to 11,975

- French CAC40 so far off 0.2% to 5,457

- Italian FTSE so far off 0.3% to 21,690

Fixed Income: If you were looking at the data you would be buying US bonds and German ones and that wouldn’t be working. The moves in bonds are modest but point to stability and stable equities more than present economic datapoints. Good demand in France and modest in Spain supply also factors. German 10Y Bund yields up 5bps to 0%, France flat at 0.39%, UK Gilts up 9bps to 1.10% - all about delays. Periphery mixed with Italy up 2bps to 2.55%, Spain flat at 1.14%, Portugal up 1bps to 1.28% and Greece off 2bps to 3.65%.

- France sold E8.998bn of longer duration OATS – at the upper edge of issuance – with strong demand and small tails. E5.49bn of 10Y 0.5% May 2029 OATs at 101.10 with 2.06 cover – previously 1.88; E1.64bn of 15Y 1.25% May 2034 OAT at 106.32 with 3.29 cover – previously 1.94 cover; E1.186bn of 31Y 1.5% May 2050 OAT at 101.10 with 1.94 cover – previously 1.72.

- Spain sold E3.518bn of bonds with strong 3Y and OK 10Y result. E1.19bn of 3Y 0.05% Oct 2021 SPGB at 100.76 with 3.25 cover – up from 2.06 previously. E1.81bn of 10Y 1.45% Apr 2029 SPGB at 103.11 with 1.35 cover – down from 1.55 previously, and E0.52bn of 9Y 0.65% Nov 2027 SGBei at 108.69 with 2.09 cover.

- US Bonds are lower across the curve– 2Y up 3bps to 2.32%, 5Y off 1bps to 2.31%, 10Y up 4bps to 2.50%, 30Y up 4bps to 2.93%.

- Japan JGBs lower chasing US, despite good 30Y sale– 2Y flat at -0.15%, 5Y up 1bps to -0.16%, 10Y up 1bps to -0.04%, 30Y up 1bps to 0.52%. MOF sold Y700bn of 30Y with 4.55 cover.

- Australian bonds lower across the curve with focus on US/China talks– 3Y up 2bps to 1.44%, 10Y up 4bpsto 1.88%, NZ 10Y up 10bps to 2.03%.

- China PBOC skips open market operations for 12thday, net leaves liquidity neutral. For the week (as tomorrow is holiday) liquidity was flat against the CNY110bn drain last week. Bonds continue lower – 2Y up 2bps to 2.64%, 5Y up 2bps to 3.03%, 10Y up 1bps to 3.25%.

Foreign Exchange: The US dollar index up 0.1% to 97.18. Emerging markets are USD bid with EMEA: RUB off 0.2% to 65.341, ZAR flat at 14.138, TRY off 0.1% to 5.625; ASIA: INR off 1.05% to 69.16, KRW off 0.3% to 1136.75.

- EUR: 1.1230 off 0.1%. Range 1.1221-1.1248 with focus on German factory orders, ECB minutes and US data – 1.12 pivotal like 1.1260.

- JPY: 111.40 flat. Range 111.33-111.52 with EUR/JPY 125.10 off 0.1%. Dead calm with 110-112 holding and focus on US rates.

- GBP: 1.3135 off 0.15%. Range 1.3134-1.3191 with EUR/GBP .8545 up 0.1% - all about Brexit delays and elections with 1.30-1.33 prison.

- AUD: .7115 flat. Range .7105-.7127 with NZD .6770 off 0.1% with AUD/NZD interesting mover. Watching China/US stories.

- CAD: 1.3355 up 0.1%. Range 1.3336-1.3365 with focus on oil, rates, and 1.3250-1.3450 prison.

- CHF: .9985 flat. Range .9967-.9988 with EUR/CHF 1.1210 flat. Watching BTPs and ECB policy for risks – 1.00 pivot still.

- CNY: 6.7145 up 0.1%. Range 6.7060-6.7200 with PBOC fixed 6.7055 from 6.7194. Stuck in waiting mode for US talks and more data.

Commodities: Oil up 0.4%, Gold flat, Copper off 0.4% to $2.9345.

- Oil: $62.71 up 0.4%.Range $62.12-$62.72 with focus on Libya story developing and global demand – with $62 base building for $63.50. Brent $69.564 up 0.3% with $70 resistance.

- Gold: $1294.90 flat. Range $1293.5-$1297.90 – nothing going on – focus is on $1286-$1302 with USD and equities mood drivers. Sivler off 0.4% to $15.04, Platinum up 2.3% to $894.30 and Palladium up 0.1% to $1379.20.

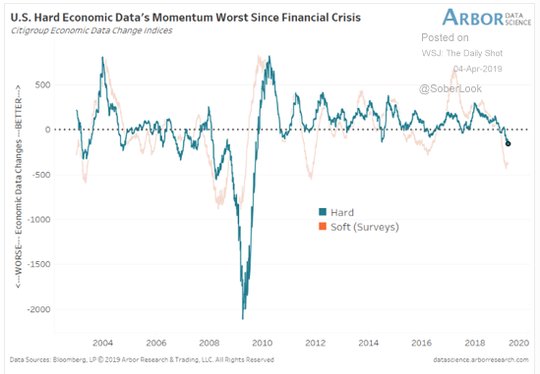

Conclusions: Is the US data weaker than the mood? The weaker Service ISM and ADP employment change yesterday add to fears about Friday’s non-Farm Payrolls report. The S&P500 rally for 5 days in a row and return to 6-month highs makes many analysts comfortable with the “Goldilocks” story of the FOMC and a late-stage economic cycle risk rally. The inversion of the yield curve, the drop in growth indicators, all are pushed aside by technical momentum factors. This clash started the week and seems likely to end it. The data on jobless claims today maybe the most important as that has been the flash signal for trouble in other times of uncertainty.

Economic Calendar:

- 0830 am US weekly jobless claims 211k p 215k e

- 1000 am Canada Mar Ivey PMI 50.6p 51.4e

- 0100 pm Cleveland Fed Mester speech

- 0400 pm NY Fed Williams speech

View TrackResearch.com, the global marketplace for stock, commodity and macro ideas here.