Markets Continue To Signal A Risk-On Bias Prevails

The recent rally in risk assets has confounded some analysts, but right or wrong the revival in animal spirits still has momentum, based on several proxies of market behavior via ETF pairs through yesterday’s close (Aug. 8)

For context, nearly a month ago CapitalSpectator.com noted that risk-on signaling had strengthened. Today’s update still finds markets reflecting a bullish profile overall. Markets are hardly flawless and so the analysis below should be viewed cautiously. But for the moment it’s not obvious that the “wisdom” of the crowd has abandoned the recent renewal in bullish expectations.

Let’s start with a comparison of so-called high beta (i.e., high-risk) stocks (SPHB) vs. low-volatility (low risk) shares (SPLV), a proxy for assessing the appetite for higher/lower risk positioning in US equities. This ratio has shot higher in recent months and is approaching the previous high in late-2021, just before last year’s sharp correction started. It’s debatable if the recent bull run has run out of road or if the latest pause is a temporary pullback before pushing on to new highs. This much is clear: if and when SPHB:SPLV tumbles, that would be a sign that the bulls are getting cold feet.

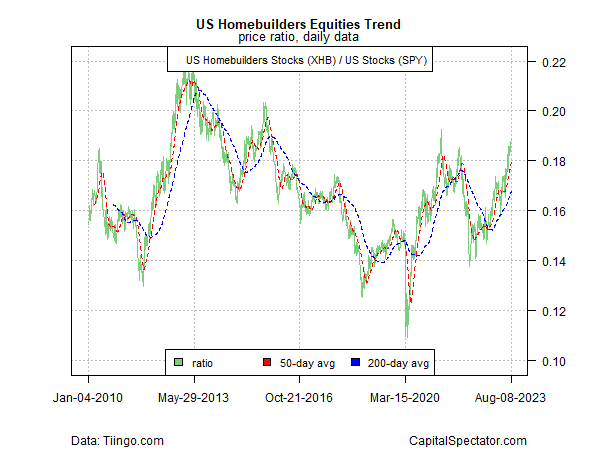

In another encouraging sign for the bulls, the rally in homebuilder stocks (XHB) is still signaling ongoing strength for this cyclically sensitive sector as it recovers in relative terms vs. the broad US stock market (SPY).

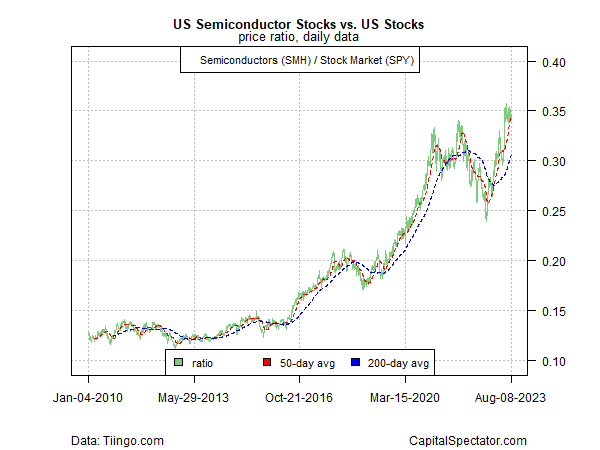

Semiconductor shares (SMH), widely seen as a proxy for the risk appetite and the business cycle, continue to show strength relative to equities generally (SPY).

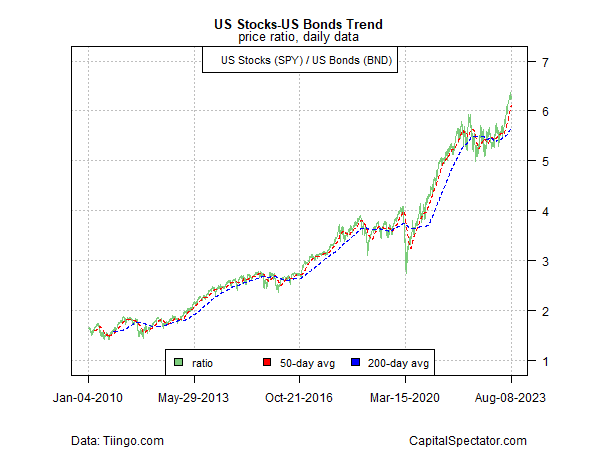

The ratio of stocks (SPY) vs. bonds (BND) continues to signal a strong risk-on bias, too.

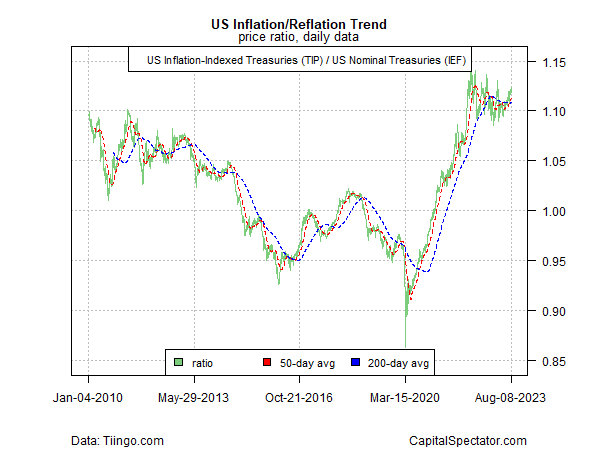

Meanwhile, the reflation/inflation trade remains in a holding pattern, based on inflation-indexed Treasuries (TIP) vs. conventional Treasuries (IEF). That’s an encouraging sign for the bulls because it suggests that the market continues to anticipate that inflation pressure will continue to ease, which in turn supports the risk-on trade.

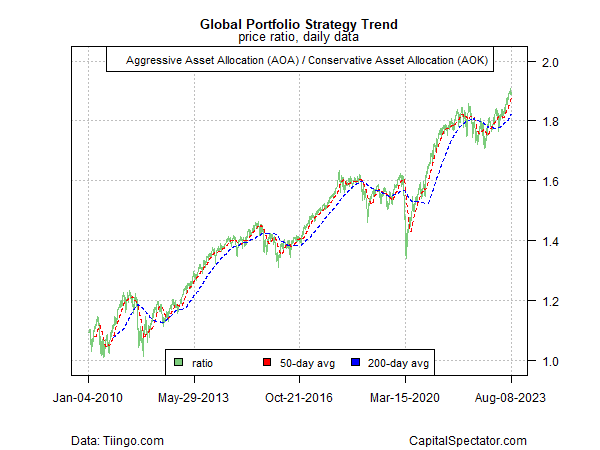

Reviewing the trend for aggressive allocation (AOA) vis-à-vis a conservative strategy for global assets (AOK) also indicates an ongoing risk-on bias.

The key question, as always, is whether the recent past is still prologue for markets? There’s always room for debate, but the lessons of trend behavior in history suggest that it’s reasonable to assume that a directional bias holds until there’s convincing evidence to the contrary.

More By This Author:

Markets See End Of Rate Hikes As Fed Officials Suggest Otherwise

US Stocks Still Lead Global Markets In 2023 By Wide Margin

First Line Of Defense For Assessing Investment Strategy Backtests

Disclosure: None.