Market Briefing For Thursday, May 13

A typical trendy haircut - is a 'fade', but it is not the same as a 'close shave'. In a sense that's a debate in this market, especially for the S&P and Nasdaq because of the leverage; because of the compelled selling in a number of the so-called hot stocks in the pandemic (that are now down as much as 50% and that is a wipe-out or worse for some hedge funds; especially leveraged play).

So as rates move up; inflation increasingly is viewed as 'other than transitory', (except for comments from some of the Fed speakers you may have heard in today's excerpts of their comments) even 'if' wages and costs do eventually it seems encounter a sharp pullback from current levitation; it's another scene.

It's all coming in April and May; though as forewarned in January, even before a totally unexpected hospital 'adventure', seasonal money would be limited in the weeks after 'contributions' (IRA and so on); and only the 'game' aspect so instilled in this era's traders would extend the move. Some stock vulnerability was suspected likely after early February; and indeed a look at Covid-plays in fact suggests many of them topped on a rotating basis starting back then.

We counted on 'rotation' to provide 'distribution under cover of a firm S&P' to sustain illusions of strength in the Index, really for a couple months at least, and that's what we were fortunate enough to see. Not very exciting as I noted a few times; but it was correct as to what we got. Momentum-type investing is (or at least was) a 'chasing of performance' late in the game; rather than when it was a 'real' bargain back at our low in March of 2020.

Executive summary:

- Risks that the Fed view of inflation being 'transitory' is increasingly playing a role in more rapid unwinding of extremely excessive early-year gains;

- Leveraged players won't escape a true 'liquidation' if that's what occurs; at this point we do not have such an event; but the threat is there especially if it increasingly appears inflation has traction;

- Even when it diminishes to a 2% or so pace (as Clarida opined today), we will still have the preceding 8-10% annualized rate from today's report so adjusting at the end, may still show higher inflation than the Fed sees;

- I have already opined that the Fed's likely slightly 'behind the curve'; and now they know every word matters; so they will parse them carefully;

- Hints of a more dramatic swoon (which could conclude this phase of the decline; but not necessarily the overall downtrend) exist by virtue of broad selling of assets, not just the big tech or pandemic-play stocks;

- In a 'liquidation' the over-leveraged crowd will sell what they 'can' sell, not simply what they want to or prefer not; and there were hints of that today;

- Some analysts thought the slightly higher Treasuries today meant traders were not seeking cover (which normally takes rates lower); I question that and think rates would be even firmer if traders weren't seeking safety;

- Big core stocks like Amazon (down despite winning an EU litigation) and Google or Facebook, are all continuing to fade (Google was the only one I thought would move higher until the recent 'peak earnings thrust'); as for the most part I've considered the entire category a reflection of overreach;

- We may see more or less a persistent inflation; obviously tapering as lots more trees are cut down; as real estate frenzies taper-off; and so on;

- As inflation pulls-down all kinds of values (often hard to recognize as 'raw price' is up from that inflation; but buying power doesn't always keep up);

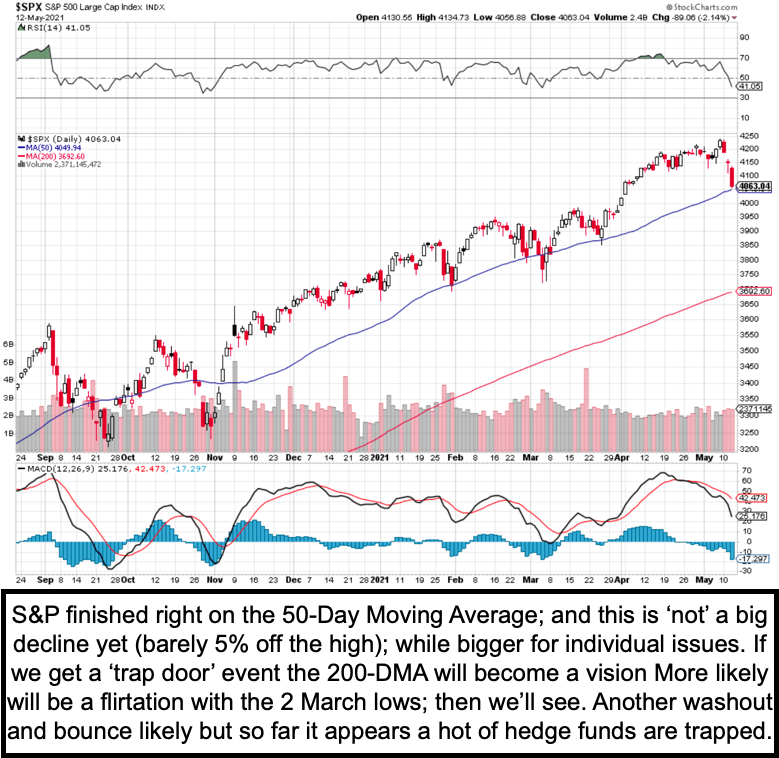

- Again, we are only off 5% in the S&P; but secular Bull Market that in my view is only just over a year old (I called 'The Inger Bottom' as a cycle low of longer-term significance); and very entitled to intermediate correction;

- I have argued that 'rotation' gave us 'distriution under an S&P cover' for a long time now; and identified late April and May as most likely for a break of the obviously-artificially S&P levels we've discussed throughout;

- This matters because it means a good percentage of the super-cap drops might be behind; except if we get the 'trap door' effect triggered by 'algos';

Markets are sometimes more 'art than science'; and the 'art' this year clearly it seems was seeing how the 'former' FANG-type (+) fund favorites were fading, while Industrial and Energy rotational strength somewhat offset those declines for awhile. Today pundits will say that 'money managers are warning clients'. I smile at that; as in many cases it's analysts and managers that perpetuated a 'false narrative' that the Fastlies, Zooms, Zillows (etc.) could only move up.

So now what? Well we've had a 'fade'; and it risks becoming a 'close shave' if algorithmic trading kicks-in, giving those analysts and trades someone to sort of blame, or should I say some 'thing' to blame. Those technical levels in this case could set-up a more important washout low than the recent minimal one, but the rub can be interest rates and real concern about inflationary aspects.

- Remember today's decline was 'only' 2% but the 50-DMA is right now, so as it breaks in the morning you might get a little technical selling before a rebound try; but there's little enthusiasm for catch fallling knives, as of yet.

An interesting analysis.

Please visit www.ingerletter.com and subscribe to our Daily Briefing. If you do so this week and mention TalkMarket in feedback to me, and I'll 'comp' the intraday MarketCasts to you at no extra charge. I have provided much of my work here for far too long; even though without videos (voice over charts.. technical analysis primarily). To continue doing so we need to see a response from readers here; which is why I will reward personal feedback so I know you read this post. I'm pretty much back to full speed; after (miraculously) surviving Covid and a more than two months hospital stay. (How I did so and how I have my strength somewhat back remains a mystery to me.)