Listen To Dallas

Image Source: Pexels

The Federal Reserve has begun a review of its monetary policy framework. The previous review was conducted in 2020, and led to the “Flexible Average Inflation Targeting” framework. The FAIT approach would have been effective, if it had been tried. Unfortunately, the Fed forget the meaning of “average”.

In a recent podcast with David Beckworth, Evan Koenig explained what went wrong with monetary policy in 2021:

Right now, I think another example which addresses the question you raised is an article I wrote along with Tyler Atkinson and Ezra Max. This was a Dallas Fed Economics blog piece that came out in January of 2022, but we wrote it in the fall or, yes, the late fall of 2021, where the latest GDP data were for the third quarter of 2021. The reason we wrote it was because if you looked at an extrapolation of nominal GDP growth from before the COVID crisis, given the Fed’s 2% inflation target, given that most estimates of long-run potential growth in the economy at the time were 2%, and given that the economy before COVID was roughly at full employment, the natural target path for nominal GDP would have been a 4% growth path extended out from late 2019.

We did that; we extrapolated a 4% growth path out, and we plotted nominal GDP since the beginning of the COVID recession. As it happened, in the third quarter of 2021, we just got back to that hypothetical target path, which is great. That’s what you want to do. The problem was that if you looked at the projections of private forecasters, and though we couldn’t talk about it at the time, if you looked at internal Fed projections, the projection was that nominal GDP was going to overshoot, substantially overshoot, that path and not come back to it.

Our argument was, “hey, great so far, but trouble ahead unless the Fed starts removing accommodation. We should be in a neutral policy stance now, neutral in the sense of stabilized nominal GDP growth at 4%. The recovery in nominal GDP has been completed. We should be at neutral, and we’re not at neutral. We’ve got our foot all the way down to the floor on the accelerator pedal, interest rates at zero, and we’re doing asset purchases.”

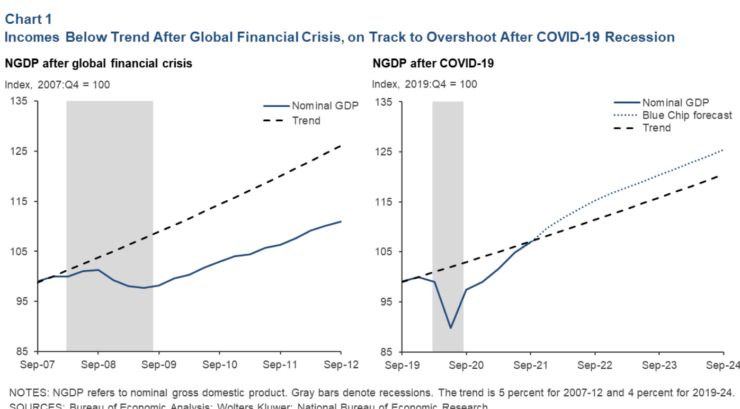

In their Dallas Fed paper, they clearly indicated that current Fed policy (in late 2021) was too expansionary:

But will NGDP stay on that path? Professional forecasters think not. Blue Chip forecasters see NGDP growth exceeding 4.0 percent from now through 2025. Thereafter, growth stabilizes, leaving the level of NGDP 4.2 percent above trend, as depicted in the right panel of Chart 1.

If the pandemic has no lasting effect on real output, that upward shift in NGDP would imply a price path 4.2 percent higher than before the pandemic. If the pandemic leaves a lasting negative mark on output, the upward shift in the price path will be even larger. The expectations of Fed policymakers, as documented in the latest Summary of Economic Projections, are broadly consistent with this outlook.

An NGDP-targeting strategy would prescribe removing policy accommodation more rapidly than currently expected in order to keep incomes nearer their prepandemic trends and reduce the long-run price-level impact of the pandemic.

They provide a chart showing the outcome they feared.

The actual NGDP overshoot was even worse than anticipated, but at least the Dallas Fed economists understood that policy was too expansionary. I hope that the people revising the Fed’s policy framework will take into consideration which parts of the Fed correctly warned that policy was off course in 2021.When policy mistakes are made, it makes sense to ask for advice from those who opposed those mistakes.

More By This Author:

Corrections Are UnhealthyChina's Deflation: Made In The USA

The Nato Debate, One Year Later