Market Analysis

The USDA’s October corn (CORN) and soybean (SOYB) crop updates were higher than last month, but their increases were moderate compared to the trade’s expectations. These larger outputs also upped both corn and soybeans 2021/22 ending stocks, but these carryover levels were just modestly higher than trade’s average estimates. US wheat and world stocks were lower as expected providing support to this food grain.

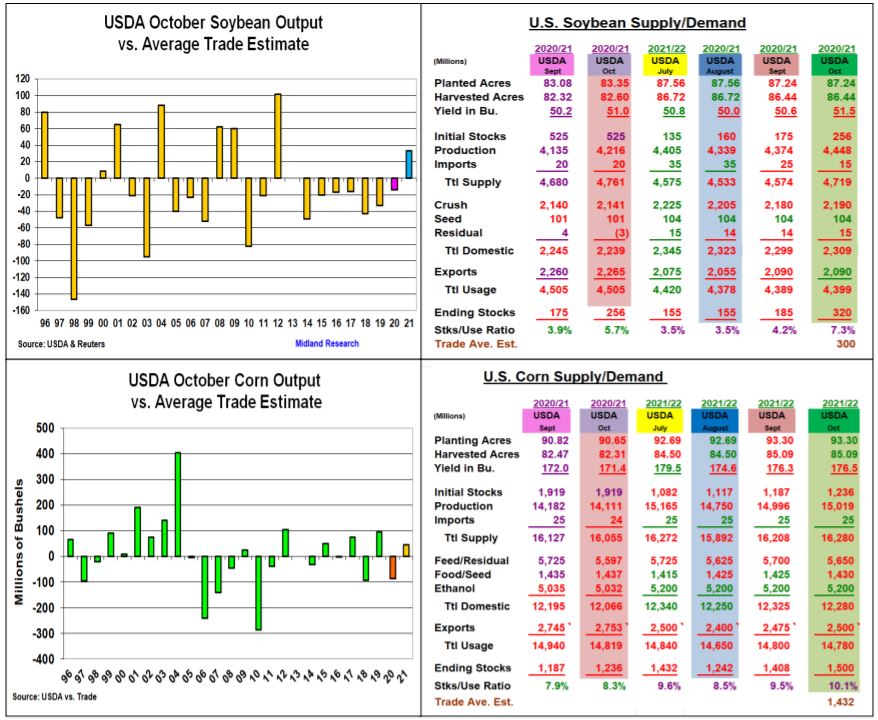

This month’s 0.9 bu increase in the US soybeans yield to 51.5 bu was 0.4 bu higher than expected. Higher yields in the W Midwest were the reason as expected. The region’s 1.5 bu yield increase along with 5 bu jump in WI’s yield pushed October output by 74 million bu, 33 million larger level than the trade forecast. This larger output and 2019/20’s higher carryover advanced this fall’s supplies to 4.719 billion (-10 million from less imports). A 10 million increase in beans’ new crop crush left the upcoming year’s stocks at 320 million, just 20 million bu larger than trade’s forecast. A note – despite a 81 million increase in 2019/20 soybean crop last month, last year’s US balance sheet has a negative 3 million bu residual in its demand data currently.

With the markets looking for a decline in corn’s Oct yield, the USDA raised its US yield by 0.2 bu to 176.5 bu this week. As expected, the ECB’s average yield was reduced by 2.8 bu because of late season disease problems this month. However, the USDA upped IA, MN & NE yields in the WCB advancing the US corn production by 46 million bu over the trade’s forecast to 15.019 billion bu. These bushels along with last year’s larger ending stocks increased this year’s supplies by 72 million. After last year’s late cut in feed demand, the USDA also sliced 50 million off 2021/22 feed outlook. However, they upped food and exports by 35 million forecasting a 1,5 billion ending stocks, up 92 million bu vs September.

A smaller US crop last month and a 2 mmt cut in Canada’s wheat output likely decreasing US wheat (WEAT) imports by 10 million bu decreased the USDA’s US wheat ending stocks to 580 million. Even with 25 million bu reduction US wheat feeding this month. 2021/22’s stocks are the lowest since 2009.

What’s Ahead

This month’s larger US corn & bean crops were the negative price catalysts. However, foreign demand led by China’s purchases as Phrase 1 concludes & La Nina’s impact on S America’s growing season remain important price factors. US harvest reports will also remain important to the markets.

Still looking to add 10-15% sales to 20-25% levels at $12.70-12.85, $5.70-85 & KC $7.75-95 prices.

Comments

Log in or sign up to join the conversation.