Inflation: The Fed’s False Flag

“Don’t piss down my back and tell me it’s raining” –Clint Eastwood/The Outlaw Josey Wales

On April 30, 2019, one day before the Federal Reserve’s FOMC policy-setting meeting, the Wall Street Journal published an article by Nick Timiraos and Paul Kiernan entitled Inflation Is Likely to Fuel Discussions as Fed Officials Meet. We quickly recognized this article was not the thoughts of the curious authors but more than likely indirect Fed messaging.

Similar to a trial balloon, conveyances like the one linked above allow the Fed to gauge market response to new ideas and prepare the markets and public for potential changes in policy.

Based on numerous articles published over the last two weeks, we are under growing suspicion that the Fed wants us to believe we need more inflation. For their part, the Fed in the May 1, 2019, FOMC policy statement changed language from the prior statement to highlight that inflation is not running at their 2% target but it is “running below” their goal.

Is declining inflation a legitimate concern or a false flag meant to provide cover to lower rates?

Selling Deflation

The WSJ article published the day before the FOMC policy meeting has the Fed’s fingerprints all over it. The gist of the article is that inflation is running below the two percent goal and therefore needs to be addressed.

The following quotes come from that article:

- Lower inflation remains the fly in the ointment.

- Officials worry that the failure to hit the inflation target could undermine its credibility over time, which could cause consumers and businesses to expect lower inflation in the future, which in turn could cause price pressures to weaken further.

- If officials grew concerned that the (inflation) shortfall was persistent, some could push for lowering rates.

Not to be outdone, Neil Irwin of the New York Times, in discussing how the Fed might fight the next recession, stated:

“In the near term, any changes are likely to tilt policy in the direction of having lower interest rates for longer periods, with the aim of getting inflation to more consistently average 2 percent (it has been consistently below that level for years).”

These and a slew of comments from Fed officials, the media and market prognosticators lead us to believe the Fed is now using a lack of inflation to justify lowering interest rates.

First quarter 2019 GDP was just reported at 3.2% and has grown in each of the last 12 quarters, an unprecedented string of consecutive increases in GDP growth. The unemployment rate and jobless claims are at or near 50-year lows. Despite the solid economic growth and strong labor market, the amount of monetary and fiscal stimulus being employed is immense as we have documented on numerous occasions. Fed Funds at 2.5%, while off of the zero bound, is still well below rates of the prior 50 years. The Fed’s balance sheet, despite some run-off, is still four times larger than where it stood pre-financial crisis.

Since the economy and labor markets are strong and monetary policy very easy, inflation appears to be the only factor that the Fed could use to justify adopting an easier policy stance.

The Smoking Gun

Before considering inflation data, its worth reviewing the Fed’s thoughts about inflation as it relates to monetary policy. On October 2, 2018, Chairman Powell stated the following:

From the standpoint of contingency planning, our course is clear: Resolutely conduct policy consistent with the FOMC’s symmetric 2 percent inflation objective, and stand ready to act with authority if expectations drift materially up or down.

Given the statement above, is Inflation or inflation expectations materially changing?

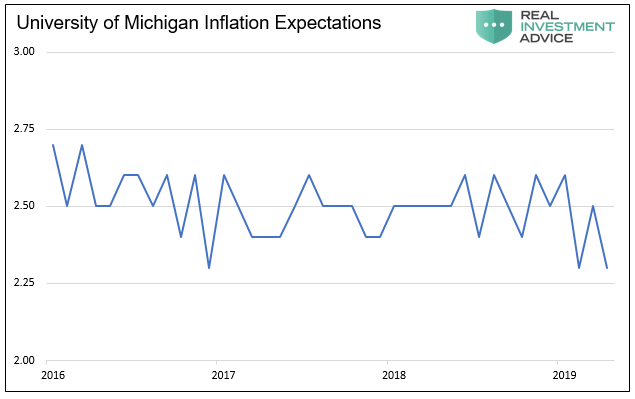

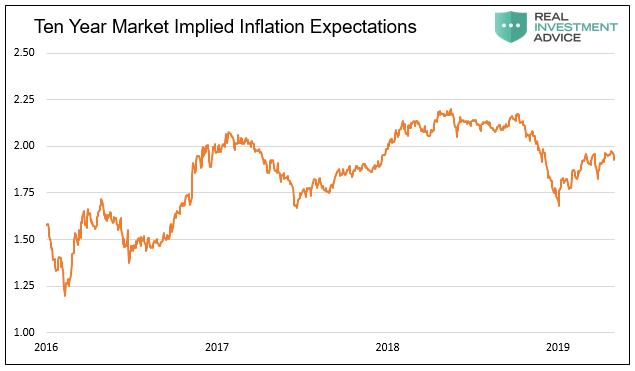

Below are six charts to help you decide if inflation or inflation expectations are moving materially lower. If not, is inflation the Trojan horse that allows the Fed to lower rates despite any reasonable rationale? All of the data for the graphs below are sourced from Bloomberg.

Inflation Expectations

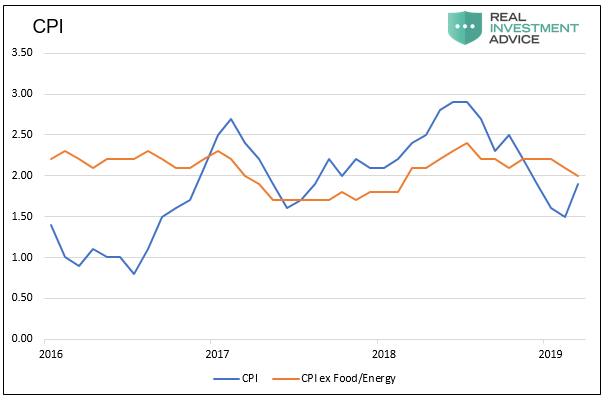

Standard Inflation Measurements

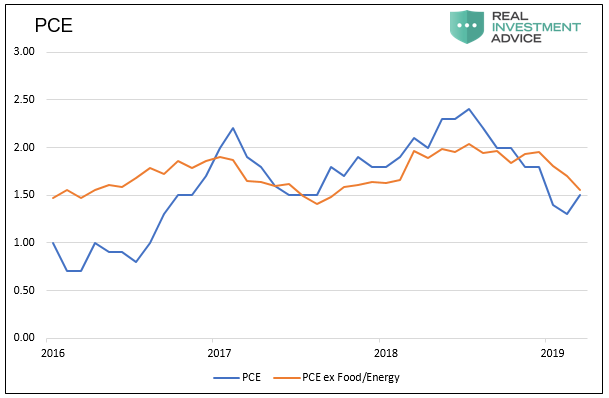

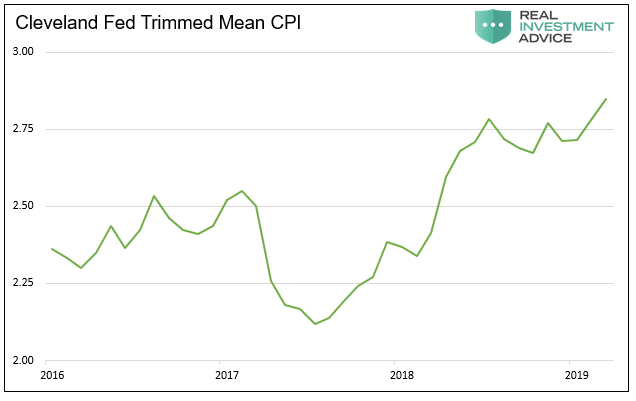

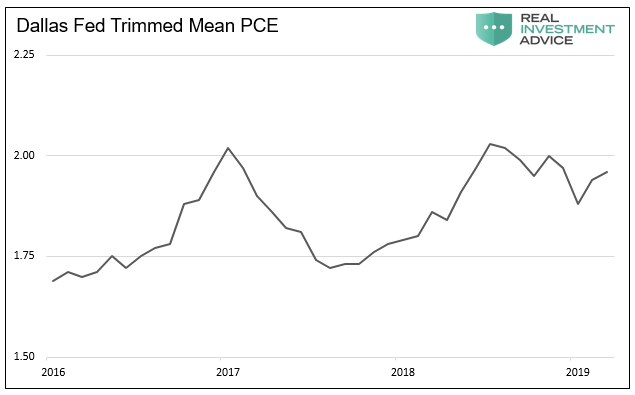

Fed’s Own Inflation Measures

The following two graphs are inflation indicators that the Fed created. They are designed to reduce temporary blips in the prices of all goods and services within the CPI and GDP reports. The Federal Reserve believes these measures present a more durable reading that is not as subject to transitory forces as other inflation measures.

Summary

Have inflation “expectations drift(ed) materially up or down?”

Looking at the ebbs and flows of inflation and inflation expectations of the last three years, we see no consistent change in the trend. As for the dreaded fear of deflation, the United States has not experienced it since the Great Depression in the 1930s. In our opinion, this recent talk about lower inflation is a sad case of the Fed manufacturing a story to justify easier monetary policy.

We conclude with a message for the Federal Reserve- If you want to lower rates then lower rates, but please do not feign concern about inflation trends that are non-existent as cover for such moves. You preach transparency, so be transparent.

Disclaimer: Click here to read the full disclaimer.

You could be right. But the Fed is obsessed with wages. This has been proven time and again. That is the opposite of lowering rates. The Fed may get around to lowering rates, but to do so quickly would be totally out of character.