Fed Wants Inflation But Their Actions Are Deflationary

A recent CNBC article states the Fed will make a major commitment to ramping up inflation. How is this different than the past decade of promises for higher inflation? More importantly, while the Fed may want inflation, their very actions continue to be deflationary.

The Fed Has A Plan

“In the next few months, the Federal Reserve will be solidifying a policy outline that would commit it to low rates for years as it pursues an agenda of higher inflation and a return to the full employment picture that vanished as the coronavirus pandemic hit.

Recent statements from Fed officials and analysis from market veterans and economists point to a move to “average inflation” targeting in which inflation above the central bank’s usual 2% target would be tolerated and even desired.

To achieve that goal, officials would pledge not to raise interest rates until both the inflation and employment targets are hit.” – CNBC

Such certainly sounds familiar.

“The Federal Reserve took the historic step on Wednesday of setting an inflation target that brings the Fed in line with many of the world’s other major central banks.

In its first-ever ‘longer-run goals and policy strategy’ statement, the U.S. central bank said an inflation rate of 2 percent best aligned with its congressionally mandated goals of price stability and full employment.”– Reuters Reporting On Ben Bernanke’s Fed Policy Statement January 26, 2012

The Unseen

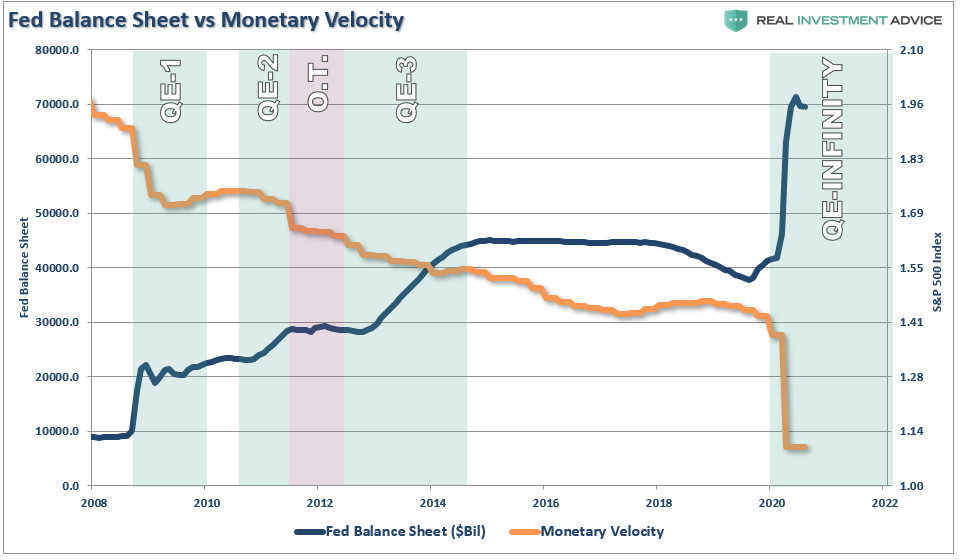

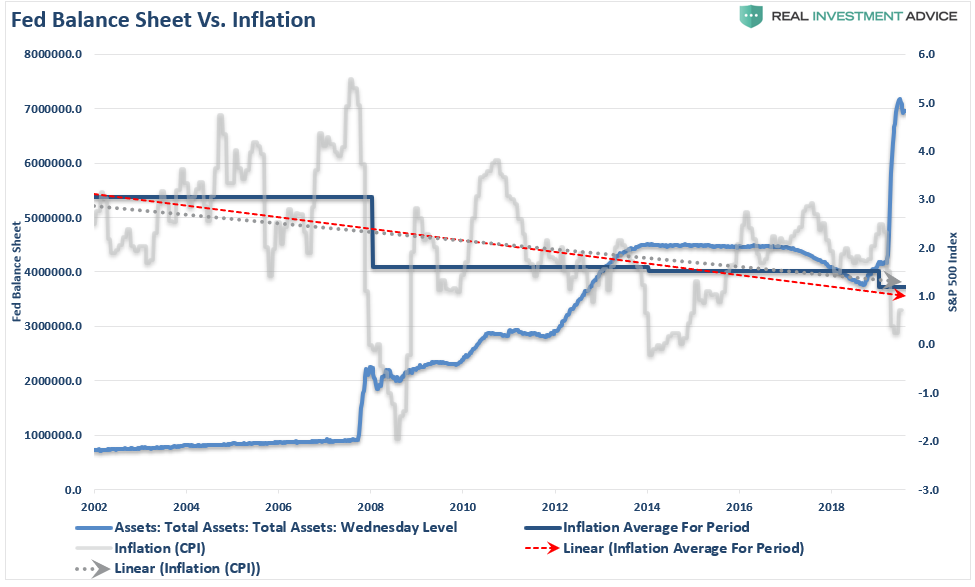

Over the last decade, the Federal Reserve has engaged in never-ending “emergency measures” to support asset markets and the economy. The stated goal was, and remains, such actions would foster full employment and price stability. There has been little evidence of success.

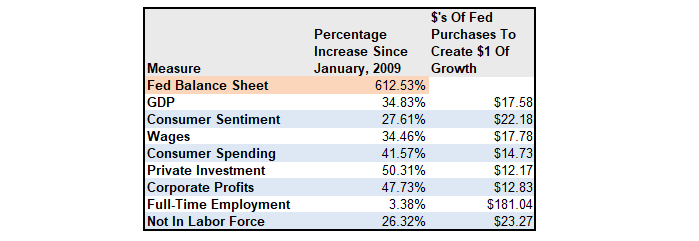

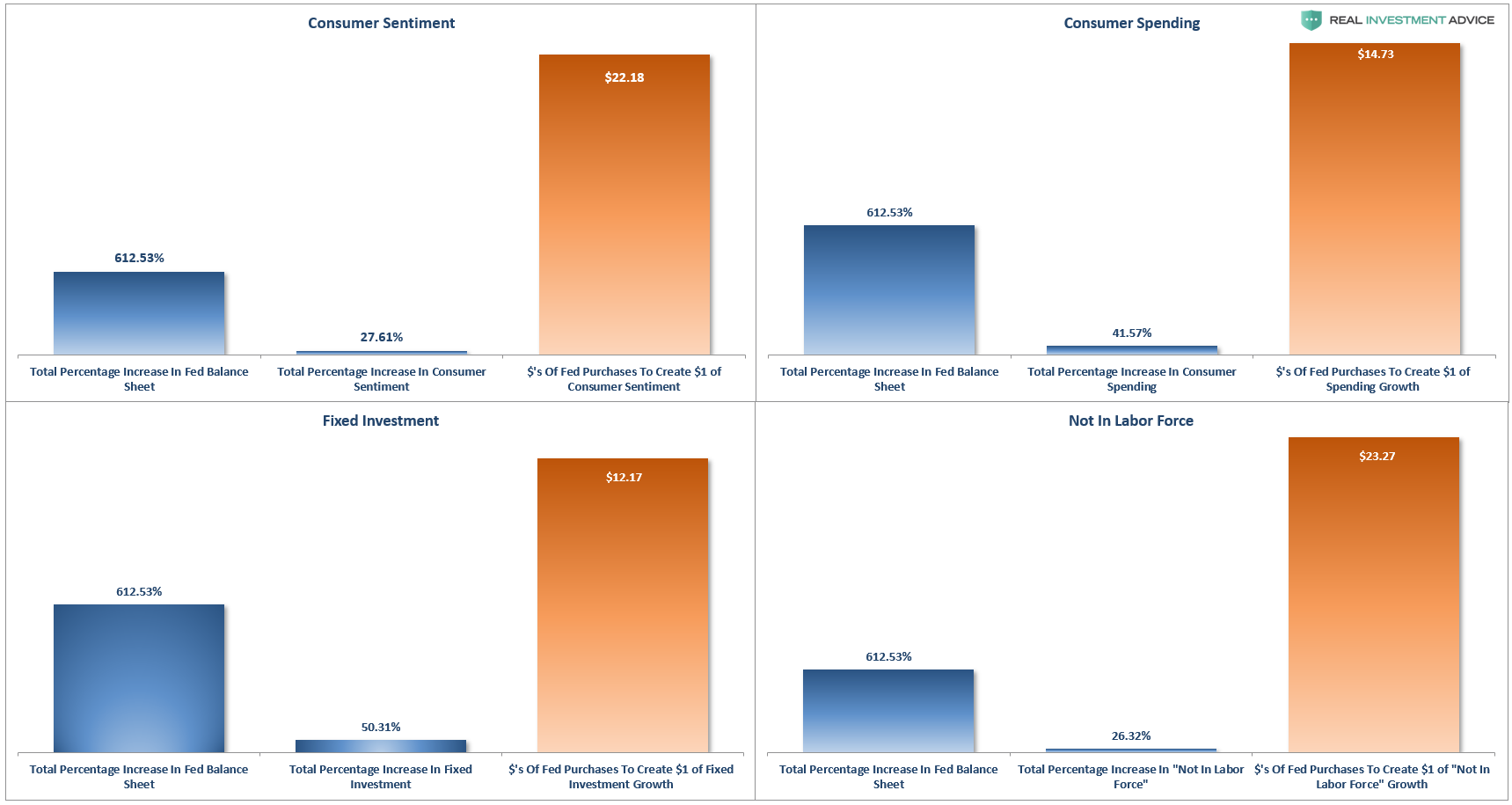

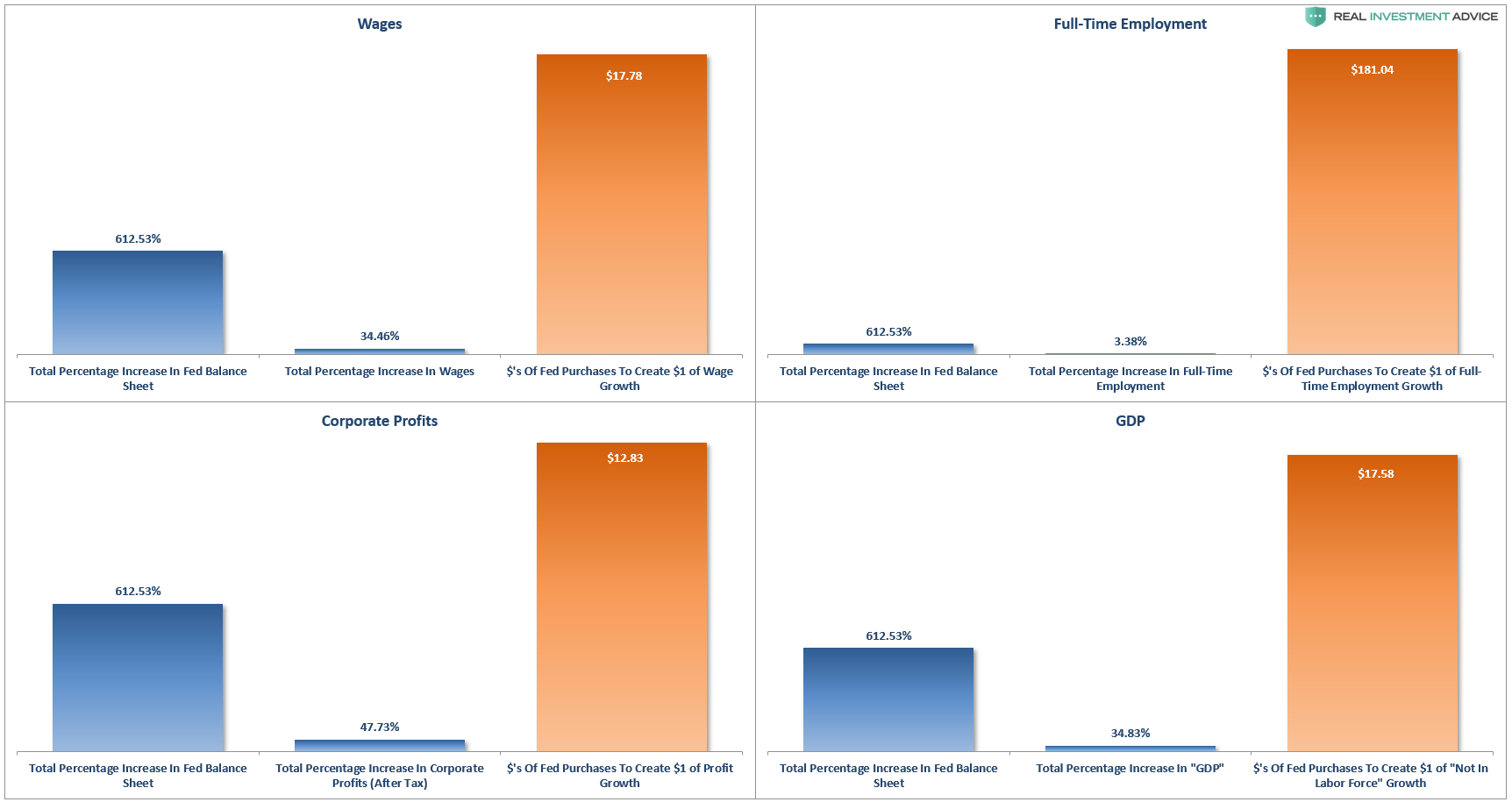

The table and charts below show the Fed’s balance sheet’s expansion and its effective “return on investment” on various aspects of the economy. For example, since 2009, the Fed has expanded its balance sheet by 612%. During that time, the cumulative total growth in GDP (through Q2-2020) was just 34.83%. In effect, it required $17.58 for every $1 of economic growth. We have applied that same measure across various economic metrics.

No matter how you analyze it, the “effective ROI” has been lousy.

These are the unseen consequences of the Fed’s monetary policies.

The Seen

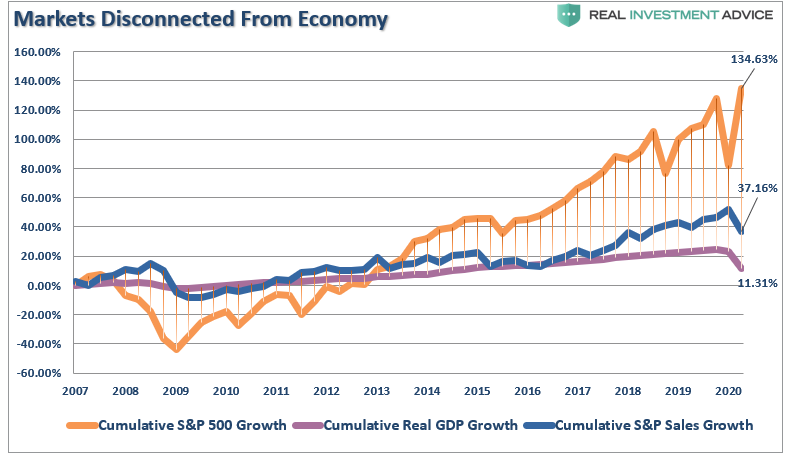

The only reason Central Bank liquidity “seems” to be a success is when viewed through the lens of the stock market. Through the end of the Q2-2020, using quarterly data, the stock market has returned almost 135% from the 2007 peak. Such is more than 12x the growth in GDP and 3.6x the increase in corporate revenue. (I have used SALES growth in the chart below as it is what happens at the top line of income statements and is not AS subject to manipulation.)

Unfortunately, the “wealth effect” impact has only benefited a relatively small percentage of the overall economy. Currently, the Top 10% of income earners own nearly 87% of the stock market. The rest are just struggling to make ends meet.

While in the short-term ongoing monetary interventions may appear to be “risk-free,” in the longer-term, the Fed has now reached the “end game” of monetary policy.

Fed’s Actions Are Deflationary

What the Federal Reserve has failed to grasp is that monetary policy is “deflationary” when “debt” is required to fund it.

How do we know this? Monetary velocity tells the story.

What is “monetary velocity?”

“The velocity of money is important for measuring the rate at which money in circulation is used for purchasing goods and services. Velocity is useful in gauging the health and vitality of the economy. High money velocity is usually associated with a healthy, expanding economy. Low money velocity is usually associated with recessions and contractions.” – Investopedia

With each monetary policy intervention, the velocity of money has slowed along with the breadth and strength of economic activity.

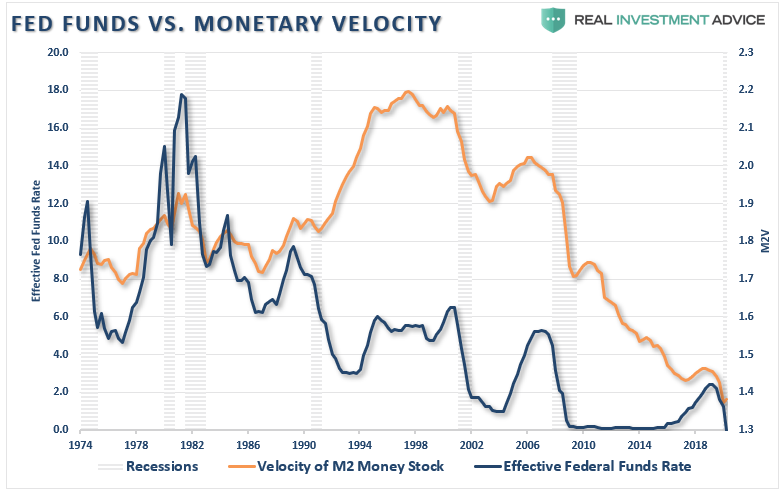

However, it isn’t just the expansion of the Fed’s balance sheet which is undermining the strength of the economy. It is also the ongoing suppression of interest rates to try and stimulate economic activity.

In 2000, the Fed “crossed the Rubicon,” where lowering interest rates did not stimulate economic activity. Instead, the “debt burden” detracted from it.

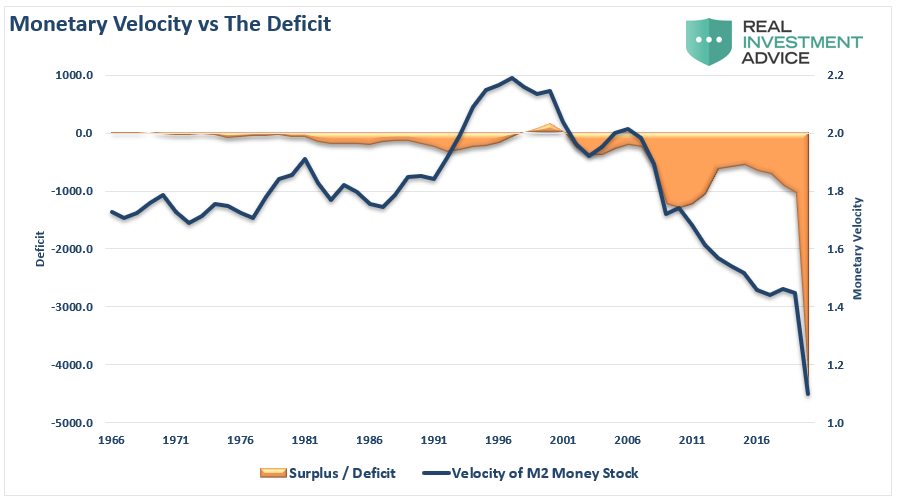

To illustrate the last point, we can compare monetary velocity to the deficit.

To no surprise, monetary velocity increases when the deficit reverses to a surplus. Such allows revenues to move into productive investments rather than debt service.

The problem for the Fed is the misunderstanding of the derivation of organic economic inflation

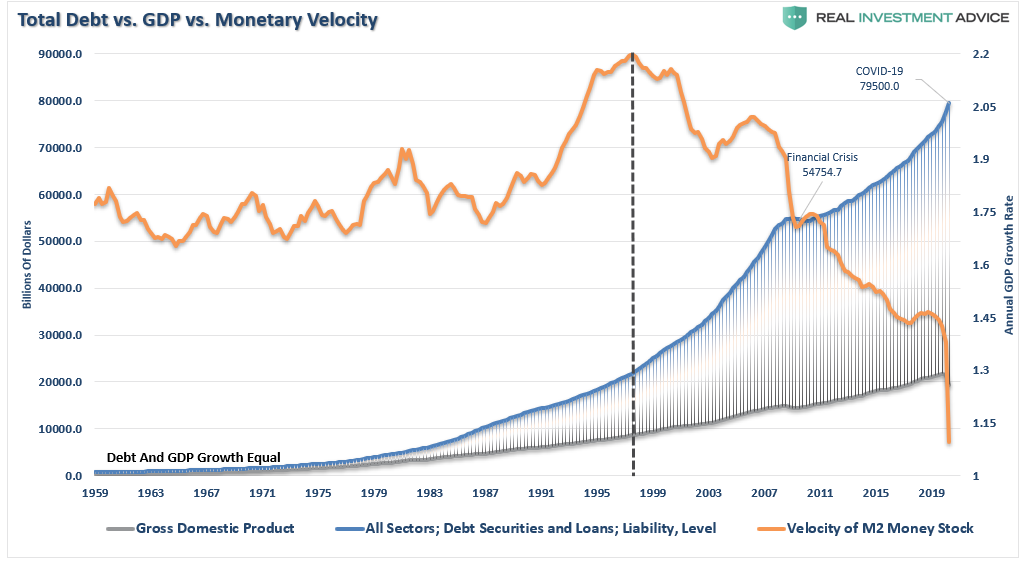

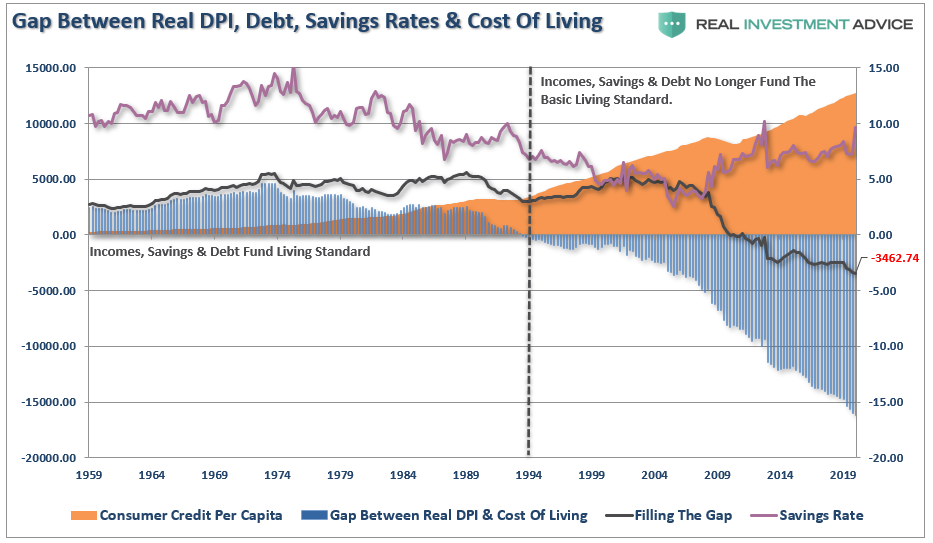

It’s The Debt

It isn’t just the Federal debt burden that is detracting from economic growth. It is all debt. As stated, the belief that lower interest rates would spur more economic activity was correct, to a point. However, as shown, once the debt burden because to consume more than it produced, the lure of debt turned sour.

You will notice that in 1998, monetary velocity peaked and began to turn lower. Such coincides with the point that consumers were forced into debt to sustain their standard of living. For decades, WallStreet, advertisers, and corporate powerhouses flooded consumers with advertising to induce them into buying bigger houses, televisions, and cars. The age of “consumerism” took hold.

However, while corporations grew richer, households got poorer, as growth in the economy and wages remained nascent.

The problem for the Federal Reserve is that due to the massive levels of debt underlying the meager economic activity it generates, interest rates MUST remain low. Any uptick in rates quickly slows economic activity, forcing the Fed to lower rates and support it.

Economic Inflation

For the last several years, the Fed’s belief has been inflating asset prices would lead to a rise in economic prosperity and inflation. As noted, the Fed did achieve “asset inflation,” which led to a burgeoning “wealth gap.”

What monetary policy did not do was lead to “general fluctuations in price levels.”

Despite the Fed’s annual call of higher rates of inflation and economic growth, the realization of those goals remains elusive.

The problem for the Fed is that monetary policy creates “bad” inflation, without supporting the things that lead to “good” inflation.

Good Inflation

The Fed believes the rise in inflationary pressures is directly related to an increase in economic strength. However, as I will explain: Inflation can be both good and bad.

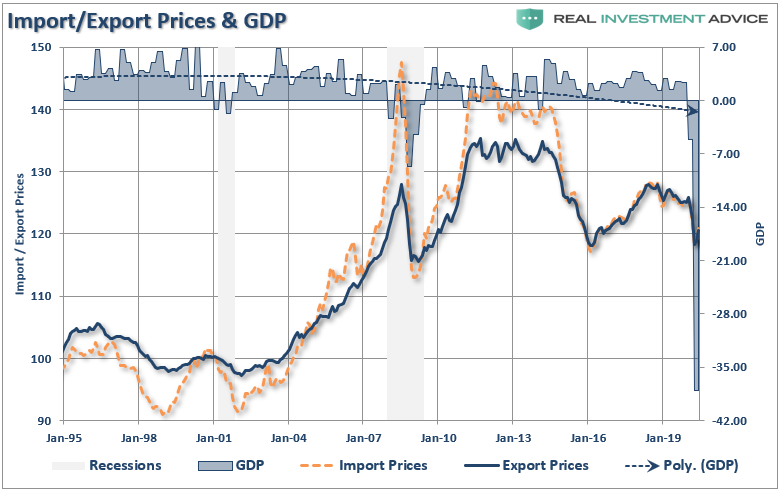

Inflationary pressures can be representative of expanding economic strength if reflected in the more robust pricing of imports and exports. Such increases in prices would suggest stronger consumptive demand, which is 2/3rds of economic growth and increases in wages allowing for the absorption of higher prices.

That would be “the good.”

Bad Inflation

The bad would be inflationary pressures in areas which are direct expenses to the household. Such increases curtail consumptive demand, negatively impacting pricing pressure, by diverting consumer cash flows into non-productive goods or services.

If we look at import and export prices, there is little indication that inflationary pressures are present.

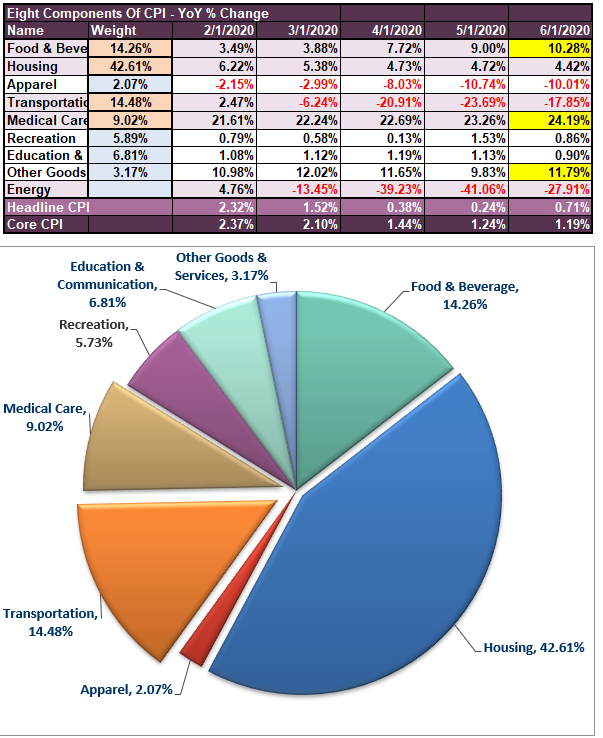

This lack of economic acceleration is seen in the breakdown of the Consumer Price Index below, which shows where inflationary pressures have risen over the last 5-months.

(Thank you to Doug Short for help with the design)

As is clearly evident, the surge in “healthcare” related costs, due to the surging premiums of insurance, pushed both consumer-related spending measures and inflationary pressures higher. Unfortunately, higher health care premiums do not provide a boost to production but drain consumptive spending capabilities.

[Housing costs, a very large portion of overall CPI, is also boosting inflationary pressures. But like “health care” costs, rising housing costs and rental rates also suppress consumptive spending ability. It is the same for Other Goods and the cost of “food,” which is stripped out of the core calculation, but eat away at disposable incomes.]

“For the middle-class and working poor, which is roughly 80% of households, rent, energy, medical and food comprise 80-90% of the aggregate consumption basket.” – Research Affiliates

The Fed’s problem is that by trying to push inflation higher, which will also drive interest rates higher to compensate, will immediately curtail increases in economic activity.

Such is why the Fed remains caught in a liquidity trap.

The Liquidity Trap

Here is the definition:

“When injections of cash into the private banking system by a central bank fail to lower interest rates or stimulate economic growth. A liquidity trap occurs when people hoard cash because they expect an adverse event such as deflation, insufficient aggregate demand, or war.

Signature characteristics of a liquidity trap are short-term interest rates remain near zero. Furthermore, fluctuations in the monetary base fail to translate into fluctuations in general price levels.”

Pay particular attention to the last sentence.

As discussed through the entirety of this article, every aspect of a liquidity-trap has been checked:

- Lower interest rates fail to stimulate economic growth

- People hoard cash because they expect an adverse event (economic crisis).

- Short-term interest rates near zero.

- Fluctuations in monetary base fail to translate into general price levels.

Importantly, the issue of monetary velocity and saving rates is critical to defining a “liquidity trap.”

Confirmation

As noted by Treasury&Risk:

“It is hard to overstate the degree to which psychology drives an economy’s shift to deflation. When the prevailing economic mood in a nation changes from optimism to pessimism, participants change. Creditors, debtors, investors, producers, and consumers all change their primary orientation from expansion to conservation. Creditors become more conservative, and slow their lending. Potential debtors become more conservative, and borrow less or not at all.

As investors become more conservative, they commit less money to debt investments. Producers become more conservative and reduce expansion plans. Likewise, consumers become more conservative, and save more and spend less.

These behaviors reduce the velocity of money, which puts downward pressure on prices. Money velocity has already been slowing for years, a classic warning sign that deflation is impending. Now, thanks to the virus-related lockdowns, money velocity has begun to collapse. As widespread pessimism takes hold, expect it to fall even further.”

Deflationary Spiral

Such is the biggest problem for the Fed and one that monetary policy cannot fix.

Deflationary “psychology” is a very hard cycle to break.

“In addition to the psychological drivers, there are structural underpinnings of deflation as well. A financial system’s ability to sustain increasing levels of credit rests upon a vibrant economy. A high-debt situation becomes unsustainable when the rate of economic growth falls beneath the prevailing rate of interest owed.

As the slowing economy reduces borrowers’ ability to pay what they owe. In turn, creditors may refuse to underwrite interest payments on the existing debt by extending even more credit. When the burden becomes too great for the economy to support, defaults rise. Moreover, fear of defaults prompts creditors to reduce lending even further.”

For the last four decades, every time the Fed has taken action trying to achieve their goals of “full employment and stable prices,” it has led to an economic slowdown, or worse.

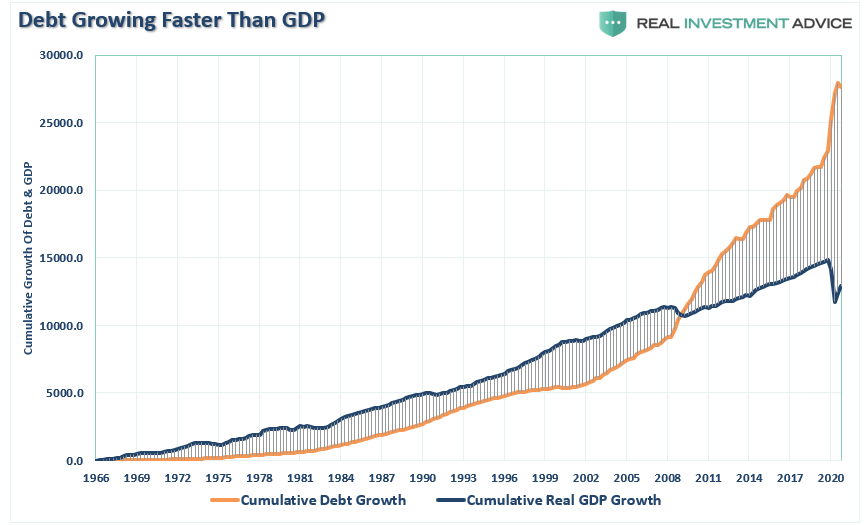

The relevance of debt growth versus economic growth is all too evident. Over the last decade, it has taken an ever-increasing amount of debt to generate $1 of economic growth.

In other words, without debt, there has been no organic economic growth.

While the Fed has been diligently working on its next program to achieve the long-elusive 2% inflation target, it will result in the same outcome as the last decade.

The problem is the debt, and you can’t solve a debt problem with more debt.

At some point, you have to stop digging.

Disclaimer: Real Investment Advice is powered by RIA Advisors, an investment advisory firm located in Houston, Texas with more than $800 million under management. As a team of certified and ...

more

Sometimes I wonder how sane the Fed actually is!