The September 2025 edition of the S&P 500 equity sector rotation chartbook can be found here. You can read more about the methodology and underlying assets here.

Image Source: Unsplash

This chartbook has been prepared with one-year total returns, which is a departure from the first version with six-month returns. I honestly didn’t think about this when I pulled the data from Investing.com, as I normally work with one-year total return data for portfolio construction and the like. This shouldn’t make a huge difference to the main conclusions, though in some cases it might obviously shift the sectors around in the key diagram, compared to a six-month return framework. If you have a preference for future versions of this chartbook, let me know.

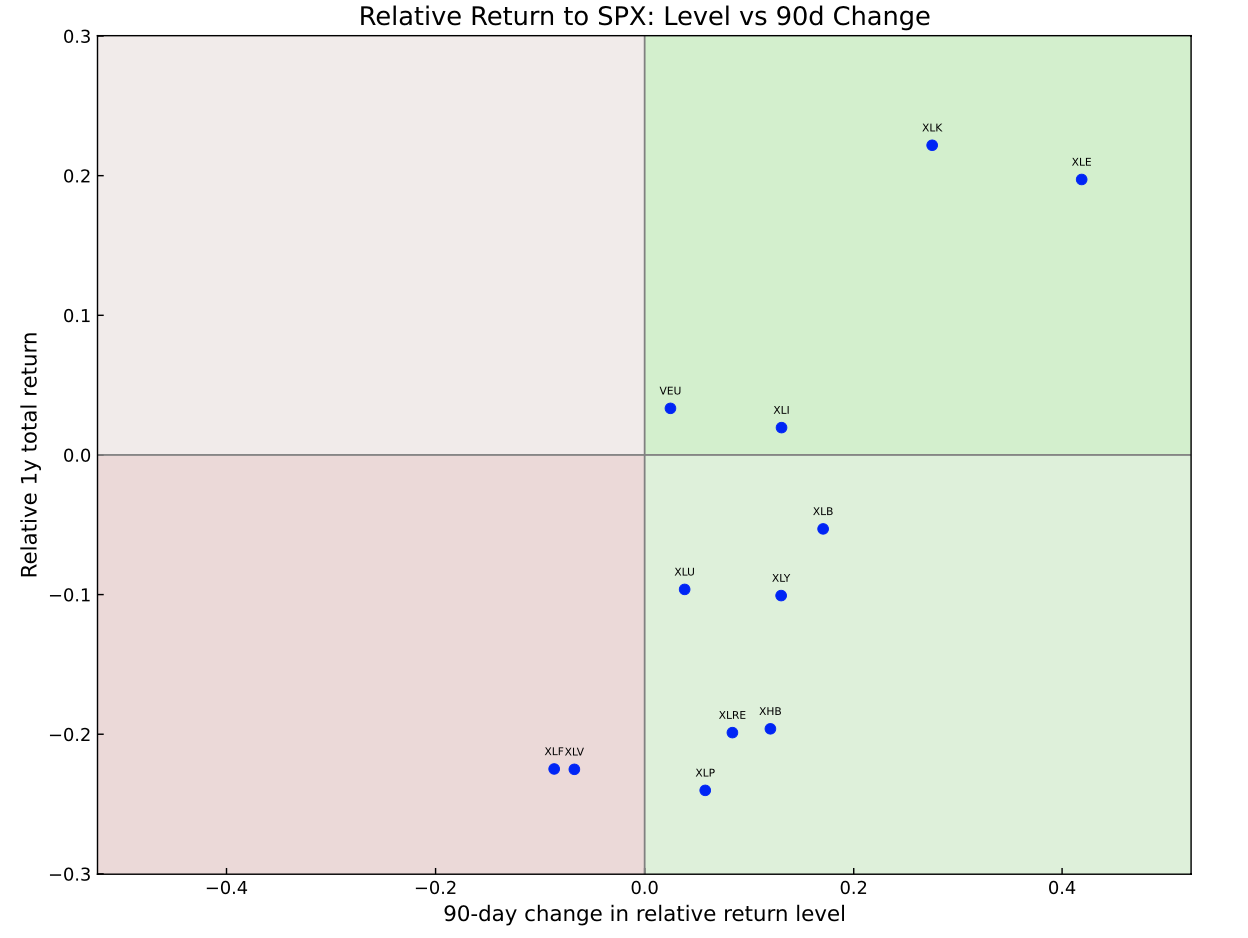

US equities have found their groove again -- and, as seen so often before, this is coinciding with a clear and strengthening leadership of technology firms and their brethren. The rotational chart below shows that telecommunication services (XLC) and technology (XLK) are now the two only sectors with positive relative return and momentum compared to the market.

This means that stalwarts and momentum investor favorites such as NVIDIA, Google, Meta, Microsoft, Apple, Palantir, Broadcom, Oracle, and Netflix are doing the heavy lifting, once again.

A rally to new highs has inevitably reignited discussions about a bubble—particularly regarding stocks driven by the ever-growing appetite for the promises of the AI revolution. JPMorgan’s Michael Cembalest addresses this in his latest Eye on the Market (EOTM) missive. His opening line is striking:

“I think this is well understood, but just to reinforce the point: AI related stocks have accounted for 75% of S&P 500 returns, 80% of earnings growth and 90% of capital spending growth since ChatGPT launched in November 2022.”

EOTM adds, using the example of the recently announced Oracle–OpenAI partnership, that the capital cycle in AI might be shifting, and becoming riskier. Companies are running out of free cash flow to fund the enormous capex needed to keep pace with competitors and meet the seemingly insatiable demand tied to this technology.

As a result, they’re turning to debt, or perhaps in time, equity issuance. More precisely, some firms eager to join the AI boom lack the cash flow to participate and must therefore seek alternative funding sources. EOTM draws on a point made by Doug O’Laughlin:

“There is no way for Oracle to pay for this with cash flow. They must raise equity or debt to fund their ambitions. Until now, the AI infrastructure boom has been almost entirely self-funded by the cash flows of a select few hyperscalers. Oracle has broken the pattern. It is willing to leverage up to hundreds of billions to seize a share. The stable oligopoly is cracking. I wrote about this earlier, and I think that we are starting to see the markers of a classical bubble.”

It’s possible we’re over-extrapolating Oracle’s strategy to suggest a broader industry shift. After all, EOTM shows that Oracle’s balance sheet looks quite different from most other large-cap firms trying to carve out a piece of the AI space.

The trend to watch now is whether we start to see a wider move toward increased leverage across the sector, with firms borrowing heavily just to keep up. Perhaps the most interesting aspect of this potential shift is that it’s not being driven by a race to build the best AI, but rather by a scramble to build the infrastructure to support the AI that already exists.

AI is now visibly driving up energy costs. EOTM notes that, “Specialized power rates for most data centers aren’t enough to cover costs of a new natural gas plant”.

In other words, even if data centers are paying a premium for existing grid energy, it’s still not enough to incentivize new capacity in a free market. And even if it were, demand would likely outpace supply, driving prices higher regardless.

Even if hyperscalers are moving quickly to vertically integrate energy into their value chains—and some undoubtedly are—energy demand is still rising faster than supply, at least for the time being. It’s a classic case of inflexible supply meeting surging demand, an economic lesson consumers, businesses, and policymakers have had to relearn repeatedly since the COVID-19 pandemic.

So, are you still buying the AI story?

I can think of at least two macro drivers supporting it, which suggest why you might, or at least why betting against it could be risky. EOTM highlights one of them: the U.S. government's decision to take a 10% stake in Intel.

EOTM defends this move with two arguments. First, that Europe and China are already supporting and subsidizing their own tech sectors, meaning U.S. firms risk falling behind without similar backing. Second, that the AI race—and perhaps the tech race more broadly—is no longer just a competition between corporations, but also between nations.

If it’s strategically vital for the U.S. to develop AGI—whatever that may be—before China does, then a strong case emerges for overweighting U.S. tech stocks, particularly for dollar-based investors with Western institutions as custodians. This geopolitical dimension is a distinguishing feature of the current AI euphoria that was largely absent during the Dotcom bubble

There’s a similar connection between the AI-fueled market rally and monetary policy. While the Fed’s recent dovish pivot is at least partly a response to labor market concerns, mounting pressure from the White House is undeniable.

Trump, Scott Bessent, and Stephen Miran—recently appointed to the FOMC—are all calling for lower rates. And it’s hard to shake the sense that their motivation isn’t solely economic. They appear to believe that an independent central bank with a 2% inflation target isn’t essential, because they want the stock market to rise, regardless of what valuations might imply in terms of long-term risk to the health of investor returns.

Tied to the AI/tech story, we might call this 'Too Big to Fail 2.0.' In the post-GFC world, governments had to accept, at the point of staring into the abyss after the crash, that letting major banks collapse—even if justified in a free market—was too dangerous. Today, TBTF means the stock market itself must always slope upwards at a 45-degree angle, or risk conceding the economic contest to geopolitical rivals.

What is a Contrarian To Do?

Returning to the rotational model above, you don’t need to buy into the idea of a government-sanctioned rally in tech/AI to stay long the sector. All you need is an understanding of momentum—and that right now, momentum clearly favors technology stocks. Trailing relative returns of XLC and XLK are still well below prior cyclical peaks—here on a one-year basis—suggesting leadership could continue.

More broadly, recent history shows that a narrow market isn’t necessarily an unhealthy one—though it is, by definition, a riskier one—despite what various market-breadth analysis may argue.

Elsewhere, several sectors now look attractive to the contrarian investor. Trailing returns for healthcare, materials, and consumer staples are approaching ten-year lows. In healthcare’s case, this partly reflects fears that the White House may target private healthcare and pharmaceutical business models to lower consumer prices.

Interestingly, the poor relative return of utilities—which should benefit from AI-driven energy demand—may tell a similar story. A market contact recently speculated that the administration is contemplating price controls in the utility sector. Meanwhile, real estate (XLRE) is also lagging, just as the Fed appears ready to ease. This may reflect skepticism about how much and how quickly the FOMC can actually cut rates.

Finally, the relative performance of non-U.S. equities (VEU in the model above) continues to fade—a predictable consequence of a U.S.-centric, tech-led rally.

Among upward movers, energy has surged over the past six months into a “rising star” category. Markets appear less concerned about a non-OPEC supply glut or a Saudi price war, and more optimistic about resilient demand.

More By This Author:

Who's Afraid Of Payrolls Anyway?

Equity Sector Rotation Chartbook For August 2025 - Order Is Restored, For Now

A Question Of Time

Comments

Log in or sign up to join the conversation.