Image Source: Pixabay

Robert Rubin, as Treasury Secretary in the Clinton years, argued that the US economy benefitted from a “strong dollar”. Not surprisingly, those arguments continue to apply, thirty years later. Yet when we look at the Trump’s dollar policy, we come away confused and somewhat bewildered.

Rubin’s arguments for a strong dollar are straightforward and easy to understand. A strong US dollar is necessary to:

- Fight inflation. Imports are cheaper for American consumers, putting downward pressure on a host of everyday products that underlie the CPI, and hence the level of interest rates needed to contain inflation.

- Attracting Investors to Build in the US. A strong dollar signifies the US economy is expanding, that its financial institutions are robust and that its Treasury bonds are the most preferred US asset to own. All these conditions made for low interest rates which in turn stimulated more capital investment.

- Avoid competitive devaluation. Broadly, Rubin suggested that a strong dollar indicates the US will never purse a policy of devaluation in the expectation of gaining a trade advantage.

Rubin’s position remained largely intact during subsequent presidential administrations, right up to the arrival of Trump and his trade wars.

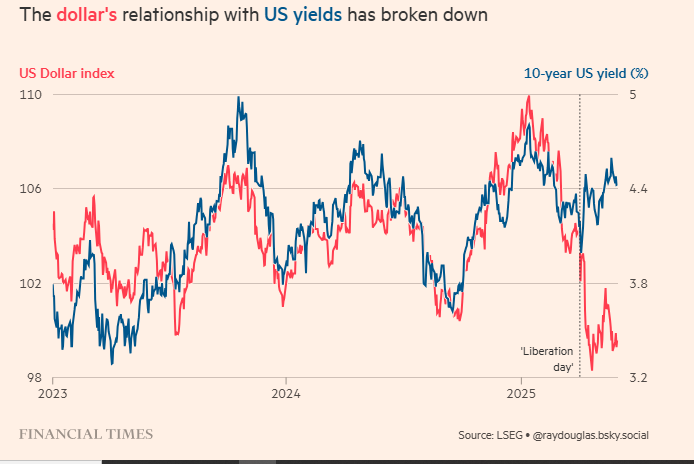

The most important relationship in any economy exists between a nation’s currency and interest rates. Conceptually, as Rubin implies, a rising currency is accompanied by lower interest rates as foreign investors seek US dollars, hence driving down the level of interest rates by purchasing US assets in the debt markets. This relationship was one of the cornerstones of the US economy, up and until Trump introduced his trade wars and upset the whole apple cart. The confusion arises from US policies regarding, trade, fiscal and monetary policies, each having a separate impact on the dollar’s worldwide position.

Impact of the tariff wars. Investors have decidedly cooled on the purchase of US Treasuries, driving up long term interest rates. Even the purchase of insurance ( credit default swaps,) against the highly unlikely prospect of the U.S. defaulting has spiked. Since ‘liberation day” US 10-year yields spiked as high as 4.7% and the dollar fell by nearly 5% against a basket of currencies.

Impact of US fiscal policy. Further spooking domestic and foreign investors is US fiscal policy which features a very dramatic increase in the federal deficit. Moody’s downgraded the US credit rating, prompting a further spike in Treasury yields at the long end.

Impact of the attack on the Federal Reserve. Worldwide, investors took a step back when Trump started to attack Chairman Powell, threatening his independence. Having backed away from that threat, investors are still left with a new set of worries about the integrity of US financial institutions and hence the US dollar.

Impact of worldwide dollar sell-off. China and Japan, the two largest holder of US dollar assets, have been shedding those assets in response to the concern for losses, but more in response to the same fears held by US domestic investors regarding the direction of US fiscal and monetary policy.

The administration’s conflicting dollar policy is been played out in the equity markets, as well. Dollar weakness accompanied by higher bond yields have a direct impact on equity prices.

In sum, as the premier reserve currency, the US dollar, is now subject to a series of inconsistent policy measures that make it very worrisome for investors. Congress is considering the Trump’s ‘big, beautiful bill” that anticipates a huge spike in the federal deficit, setting off alarm bells on Wall St. JP Morgan's Jamie Dimon has warned that the US bond market will “crack” under the weight of the country’s rising debt. The divergence between rising interest rates and the dollar will likely widen, as the faith in the US dollar declines further.

.

More By This Author:

Trump’s Great Walk Back On TariffsThe Bank Of Canada Calls The Trade War The Greatest Threat To Financial Stability

Early Waring Signs Of The Impending Recession

Comments

Log in or sign up to join the conversation.