Image Source: Unsplash

Asian equity markets took their cues from Wall Street, which showed positive momentum as yields and oil prices declined from recent peaks. However, gains in the region were somewhat limited as investors approached quarter-end and amid holiday closures in several countries. The Nikkei 225 initially made gains but pulled back from resistance around the 32k handle. Encouraging data releases, including Retail Sales and Industrial Production, along with softer Tokyo inflation, were not enough to sustain the gains. In contrast, the Hang Seng outperformed as property and tech sectors surged. This followed the easing of yields and additional supportive measures from Chinese authorities. The Hang Seng remained resilient despite the absence of mainland participants due to the Mid-Autumn Festival and the upcoming National Day holidays.

Earlier today, the Office for National Statistics (ONS) confirmed Q2 GDP growth in the UK at 0.2%, with the year-on-year rate revised up to 0.6% from 0.4%. The ONS's Blue Book revisions for historical GDP data will be assessed by the Bank of England's Monetary Policy Committee (MPC) at its next policy meeting in November, which will incorporate the revisions into updated economic forecasts. The Bank of England will also release money and credit data, including mortgage approvals.

Expectations are for a sharp decline in the Eurozone's flash estimate for September headline CPI inflation. Recent data from Germany and France have shown drops in EU-harmonised inflation rates, indicating downside risks for the Eurozone's CPI release. The focus is shifting to how long the European Central Bank (ECB) will keep interest rates in restrictive territory after an expected peak in inflation.

Stateside, an increase in personal spending of 0.8% is expected for August. The PCE deflator, the Fed's preferred inflation gauge, is forecasted to rise in line with the CPI, primarily driven by energy prices. Other data releases include the advance goods trade data and the final reading of the University of Michigan consumer sentiment survey. Additionally, markets will closely watch a speech on monetary policy from the Fed's Williams. Yesterday Chair Powell emphasised that while inflation has moderated somewhat and inflation expectations remain well anchored, the process of bringing inflation down to the 2.0% target has a considerable distance to go. He stated that the Federal Reserve will maintain interest rates at restrictive levels until they are confident that inflation is on a path back towards the target.Furthermore, Powell highlighted that achieving this goal may necessitate a period of growth below trend and some softening in labour markets. While he acknowledged that the last three inflation reports were positive, he emphasised the need for more sustained improvement beyond just a few reports.

FX Positioning & Sentiment

Institutional FX month-end rebalancing models are anticipating an increased demand for USD as month-end flows come into play. Credit Agricole's model suggests that the strongest USD buy signal is against CAD. However, their corporate flow model points to EUR buying at the end of the month. Barclays' model indicates strong USD buying against all major FX pairs. The USD has been on the front foot against all major currencies throughout the week, and FX options have seen raised risk premiums due to concerns of further USD gains and increased volatility. Morgan Stanley's outlook includes a projection of the DXY eventually reaching 1.0800 and EUR/USD dropping to 1.0300. These models and analyses reflect the ongoing dynamics in the foreign exchange market as traders assess various factors influencing currency movements.

CFTC Data As Of 26-09-23

During September 20-26, the USD index saw a gain of 1.01%, indicating the potential growth of USD long positions. In contrast, the EUR/USD pair declined by 1.01% during the same period, suggesting a likely further unwinding of EUR long positions, with Friday's data expected to provide more insights into this trend.

The market's view of the Federal Reserve keeping interest rates higher for longer has put the 2023 low for EUR/USD at 1.0482 in focus. The USD/JPY pair saw a gain of 0.81% in the reporting period, indicating a potential growth in yen short positions. Traders were closely watching the key level of 150, with the continued dovish stance of the Bank of Japan (BoJ) keeping the USD bid. Bullish traders have their sights set on 150, with the 2022 high at 151.94 serving as a potential target.

GBP/USD pair declined by 1.92% in the reporting period, weighed down by the Bank of England's dovish lean after the recent 5-4 rate hold. The interest rate profile (IRPR) indicated the possibility of just one more BoE rate hike in 2024, signalling a decrease from the previously expected peak rate of 6.5%.

In the commodity-centric currency space, the AUD/USD pair was down by 0.91%, while the USD/CAD pair gained 0.52%. The less dovish stance of the Federal Reserve and concerns related to China weighed on these currencies. (Source Reuters)

FX Options Expiries For 10am New York Cut

(1BLN+ represent larger expiries, more magnetic when trading within daily ATR)

-

EUR/USD: 1.0500 (1.7BLN), 1.0555 (593M), 1.0570-75 (1BLN)

-

1.0600 (3.7BLN), 1.0650 (1.4BLN)

-

USD/CHF: 0.9100 (600M), 0.9120-25 (710M), 0.9150 (480M)

-

EUR/CHF: 0.9610 (572M), 0.9625 (321M), 0.9675 (347M)

-

GBP/USD: 1.2130 (269M), 1.2150 (258M), 1.2250 (325M)

-

1.2280 (248M), 1.2300 (411M). EUR/GBP: 0.8640 (769M)

-

AUD/USD: 0.6380 (774M), 0.6425 (253M), 0.6500 (734M)

-

NZD/USD: 0.6000 (365M)

-

USD/CAD: 1.3400-05 (631M), 1.3470-75 (533M), 1.3500 (836M), 1.3510-15 (707M)

-

USD/JPY: 148.50 (305M), 149.00 (1.3BLN)

Overnight Newswire Updates of Note

-

Fed's Barkin: Job Market Has Been Resilient In Current Tightening Cycle

-

Bank Of Japan Announces Unscheduled Bond Buying Operation

-

Tokyo Inflation Slows, Giving Support To BoJ Price Outlook

-

Japan Retail Sales Climb 7.0% On Yr In Aug, Industrial Production Unch

-

China Central Banker Pushes Banks To Expand Along Belt And Road

-

Dollar Off 10-Month High, Yen Still Under Intervention Watch

-

Japan’s 30-Year Bond Yield Reaches Highest Level Since 2013

-

Oil Edges Higher After Technical Resistance Stalled Fierce Rally

-

Unexpected China Demand, Output Cuts Behind Surge In Oil Prices

-

Asian Stocks Gain, Paring Quarterly Loss, As Hong Kong Rallies

-

HSBC’s Cowper-Coles To Exit After Deploring UK’s Stance On China

-

Nike Beats Profit Estimates, Pledges To Boost Focus On Running Shoes

(Sourced from Bloomberg, Reuters and other reliable financial news outlets)

Technical & Trade Views

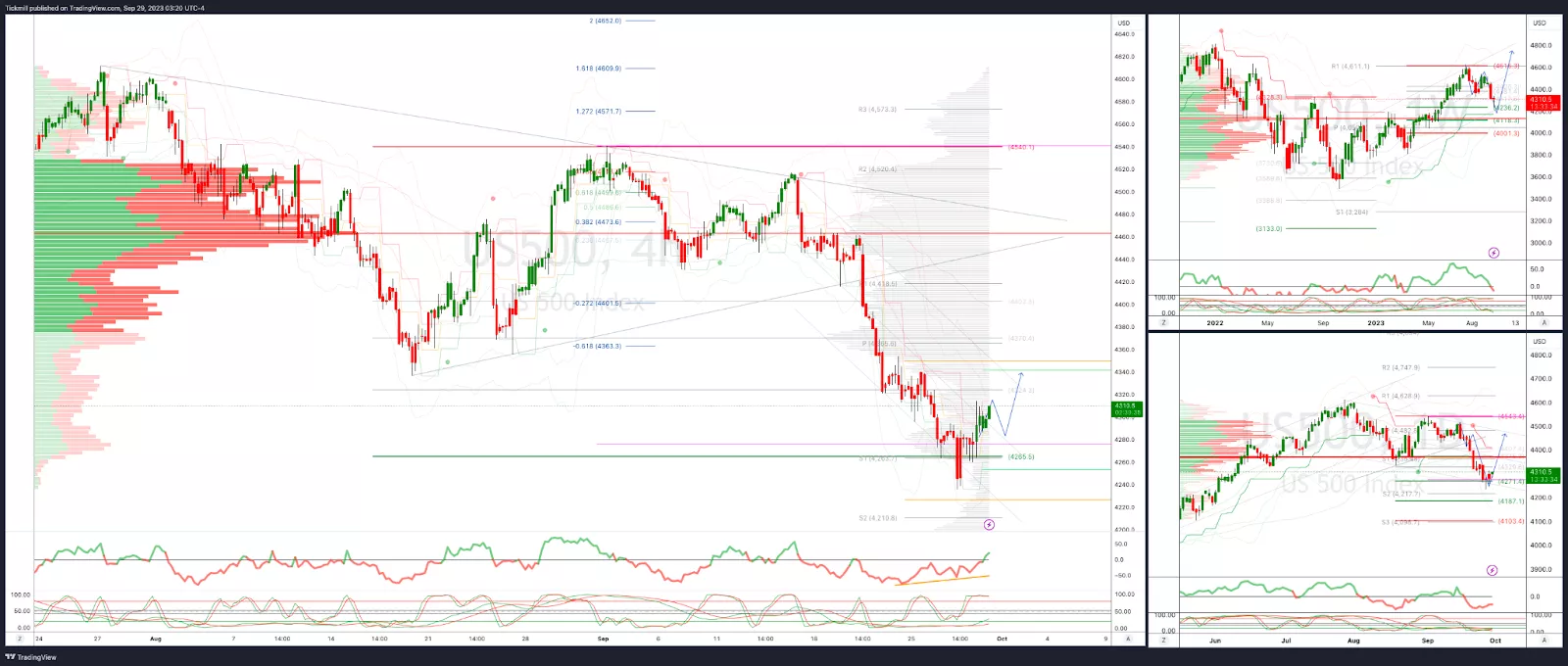

SP500 Bias: Bullish Above Bearish Below 4300

-

Above 4310 opens 4330

-

Primary resistance is 4400

-

Primary objective is 4225

-

20 Day VWAP bearish, 5 Day VWAP bearish

(Click on image to enlarge)

EURUSD Bias: Bullish Above Bearish Below 1.0610

-

Above 1.06 opens 1.0650

-

Primary resistance is 1.0760

-

Primary objective is 1.0477

-

20 Day VWAP bearish, 5 Day VWAP bearish

(Click on image to enlarge)

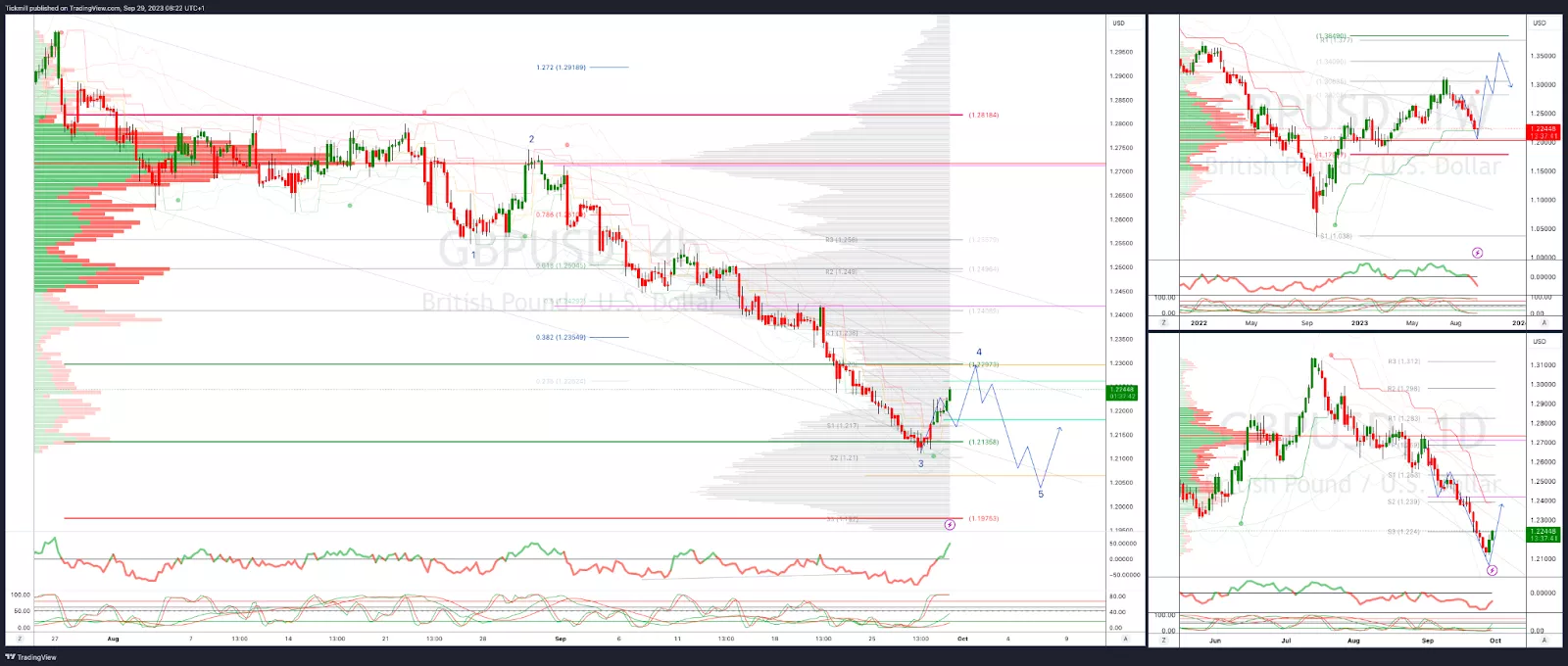

GBPUSD Bias: Bullish Above Bearish Below 1.22

-

Above 1.22 opens 1.23

-

Primary resistance is 1.2450

-

Primary objective 1.2060

-

20 Day VWAP bearish, 5 Day VWAP bullish

(Click on image to enlarge)

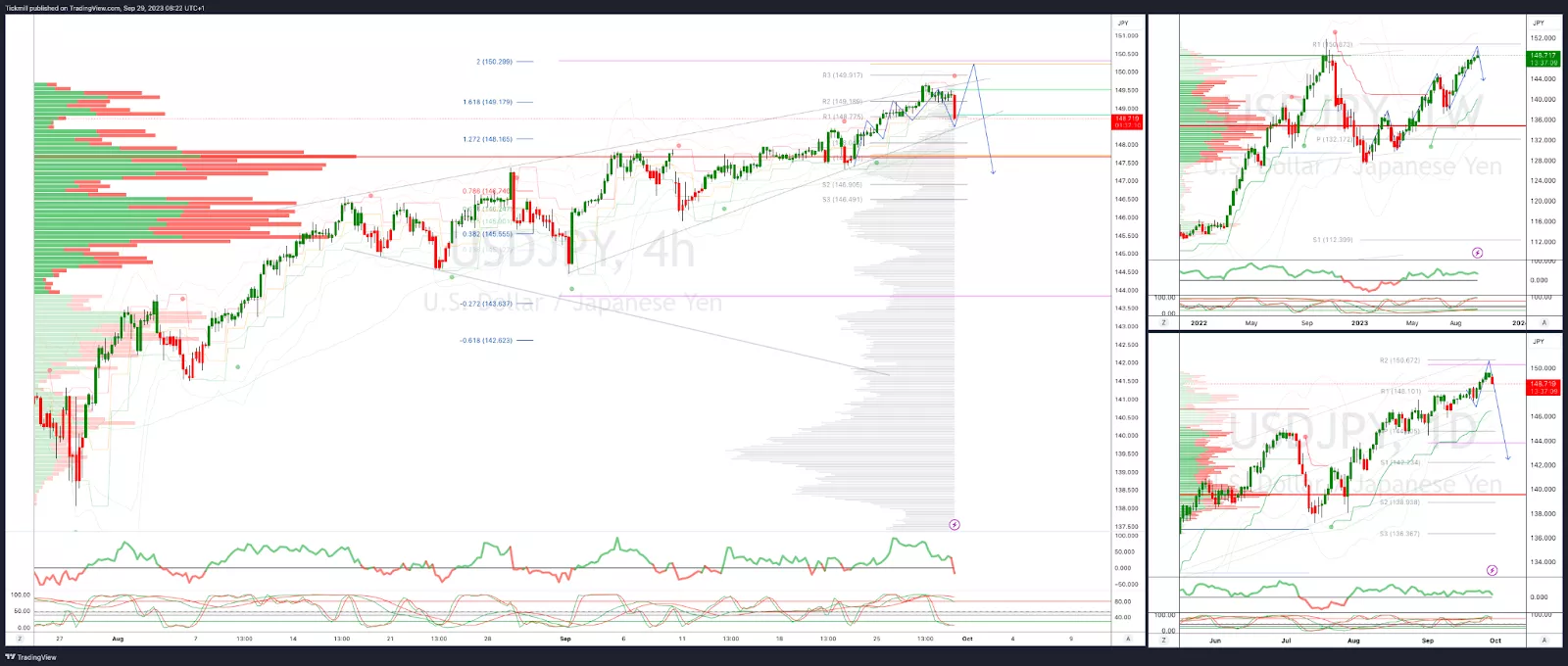

USDJPY Bias: Bullish Above Bearish Below 148.50

-

Below 148 opens 147.50

-

Primary support 144.50

-

Primary objective is 150

-

20 Day VWAP bullish, 5 Day VWAP bullish

(Click on image to enlarge)

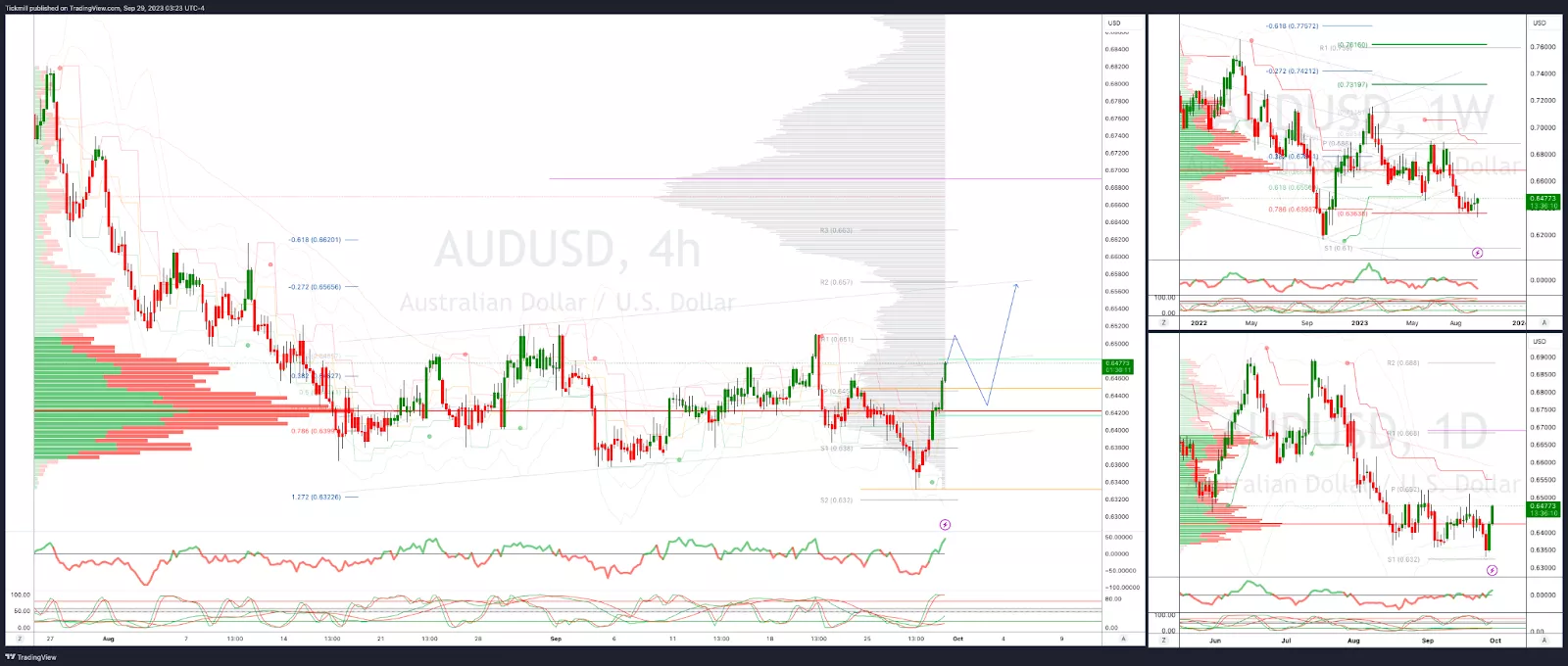

AUDUSD Bias: Bullish Above Bearish Below .6450

-

Above .6475 opens .6525

-

Primary resistance is .6620

-

Primary objective is .6320

-

20 Day VWAP bearish, 5 Day VWAP bearish

(Click on image to enlarge)

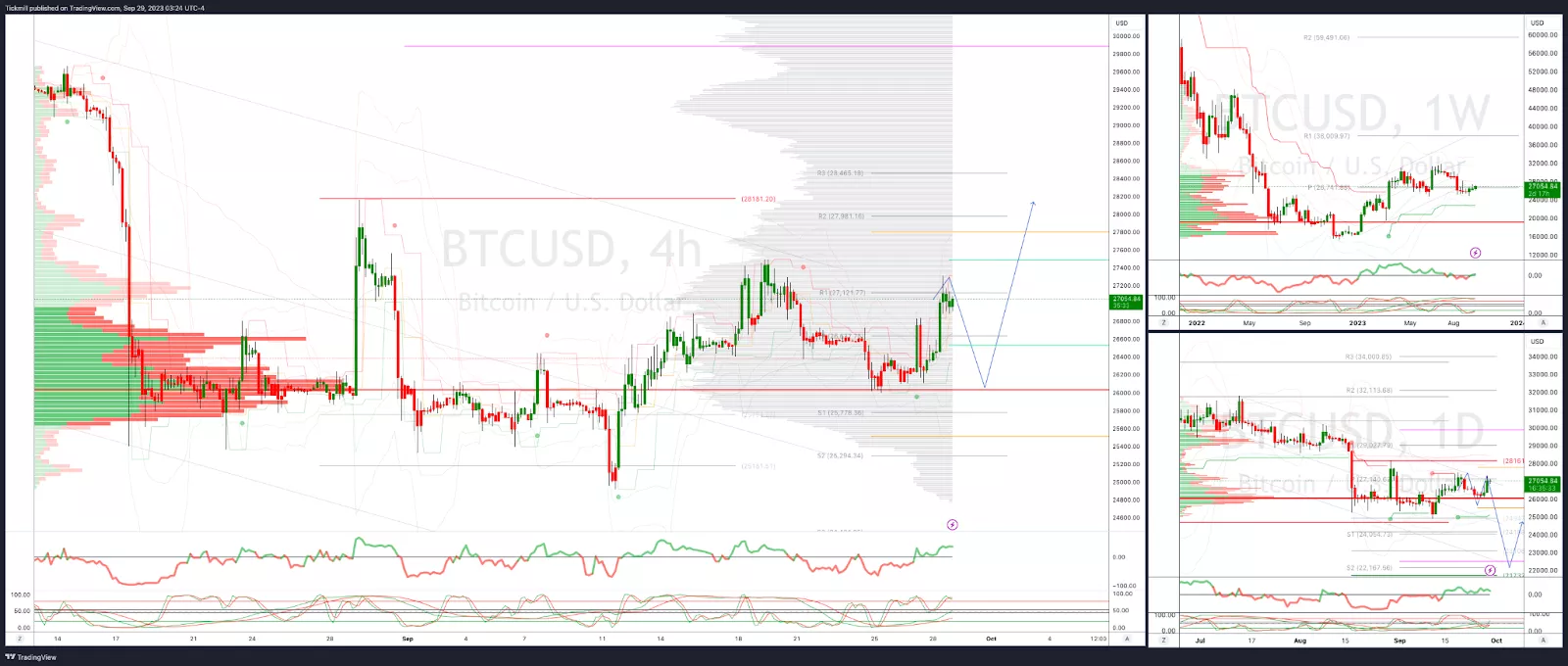

BTCUSD Bias: Bullish Above Bearish below 27500

-

Above 28200 opens 30000

-

Primary resistance is 28175

-

Primary objective is 23300

- 20 Day VWAP bearish, 5 Day VWAP bearish

(Click on image to enlarge)

More By This Author:

Homebuilders Under Pressure As Borrowing Costs Remain Elevated

Daily Market Outlook - Thursday, September 28

Increasing Interest Rate Woes Weigh On Sentiment

Comments

Log in or sign up to join the conversation.