Asian equity markets with a mixed tone as traders evaluated the performance in the US leading into the end of the month and quarter. Global yields and oil prices saw further upside, impacting market sentiment. The Nikkei 225 underperformed, slipping below the 32k handle and facing headwinds from a mass ex-dividend day involving over 1,400 companies in Japan. Meanwhile, the Hang Seng and Shanghai Composite indices diverged, with the property sector facing challenges following the suspension of Evergrande shares and some of its units. However, the mainland market was buoyed by the People's Bank of China's liquidity injections and China's support pledges.

In Europe, attention turns to the release of September inflation estimates for Spain (3.2% vs 3.3% Exp) and Germany, with the Eurozone flash CPI estimate scheduled for Friday. Expectations pointed to a sharp decline in Eurozone headline CPI to 4.5%, the lowest in nearly two years, from 5.2% in August, driven by lower inflation in food, energy, and services. The data reinforced expectations that the European Central Bank's interest rates had likely peaked. The Eurozone economic confidence index for September was also on the agenda, with forecasts suggesting a drop to 92.0 from August's 93.3, marking the weakest level in nearly three years. Consumer confidence had already fallen for two consecutive months, and the decline was expected to extend to industrial and services confidence.

Stateside, the focus shifted to indicators for Q3 growth, with Q2 GDP growth expected to be revised slightly higher to 2.2% (annualised) from 2.1%. Attention was also on releases such as weekly jobless claims and pending home sales.

Central bank appearances included Fed Chair Powell and some ECB speakers, with BoE MPC member Greene participating in a panel discussion in Sweden. Greene had voted for a rate hike in the recent BoE meeting. Additionally, there will be several notable speeches from Fed voters Austan Goolsbee and Charles Cook, and 2024 voter Thomas Barkin. These speeches may provide insights into the Fed's economic outlook and monetary policy stance.

FX Positioning & Sentiment

Institutional FX month-end rebalancing models are anticipating an increased demand for USD as month-end flows come into play. Credit Agricole's model suggests that the strongest USD buy signal is against CAD. However, their corporate flow model points to EUR buying at the end of the month. Barclays' model indicates strong USD buying against all major FX pairs. The USD has been on the front foot against all major currencies throughout the week, and FX options have seen raised risk premiums due to concerns of further USD gains and increased volatility. Morgan Stanley's outlook includes a projection of the DXY eventually reaching 1.0800 and EUR/USD dropping to 1.0300. These models and analyses reflect the ongoing dynamics in the foreign exchange market as traders assess various factors influencing currency movements.

CFTC Data As Of 26-09-23

During September 20-26, the USD index saw a gain of 1.01%, indicating the potential growth of USD long positions. In contrast, the EUR/USD pair declined by 1.01% during the same period, suggesting a likely further unwinding of EUR long positions, with Friday's data expected to provide more insights into this trend.

The market's view of the Federal Reserve keeping interest rates higher for longer has put the 2023 low for EUR/USD at 1.0482 in focus. The USD/JPY pair saw a gain of 0.81% in the reporting period, indicating a potential growth in yen short positions. Traders were closely watching the key level of 150, with the continued dovish stance of the Bank of Japan (BoJ) keeping the USD bid. Bullish traders have their sights set on 150, with the 2022 high at 151.94 serving as a potential target.

GBP/USD pair declined by 1.92% in the reporting period, weighed down by the Bank of England's dovish lean after the recent 5-4 rate hold. The interest rate profile (IRPR) indicated the possibility of just one more BoE rate hike in 2024, signalling a decrease from the previously expected peak rate of 6.5%.

In the commodity-centric currency space, the AUD/USD pair was down by 0.91%, while the USD/CAD pair gained 0.52%. The less dovish stance of the Federal Reserve and concerns related to China weighed on these currencies. (Source Reuters)

FX Options Expiries For 10am New York Cut

(1BLN+ represent larger expiries, more magnetic when trading within daily ATR)

-

EUR/USD: 1.0530-35 (424M), 1.0585 (468M), 1.0600 (593M), 1.0665-75 (1.1BLN)

-

USD/CHF: 0.8990 (759M) . EUR/GBP: 0.8650 (431M)

-

GBP/USD: 1.2000 (1.1BLN), 1.2100 (235M), 1.2200 (1.5BLN)

-

AUD/USD: 0.6350 (337M), 0.6475 (360M), 0.6500 (450M)

-

NZD/USD: 0.5940 (258M)

-

USD/CAD: 1.3450 (741M), 1.3465 (250M), 1.3530-35 (620M)

-

USD/JPY: 146.60 (2BLN), 147.00 (516M), 147.70 (974M), 148.00 (424M)

-

148.80 (517M), 149.70 (427M), 150.00-05 (594M)

Overnight Newswire Updates of Note

-

JPMorgan ‘Options Whale’ Worries Resurface As Stocks Extend Drop

-

WH: US Economy Facing Headwinds From Possible Government Shutdown

-

Australian Retail Sales Cool, Boosting Case To Extend Rate Pause

-

China Risk Growing, Say 60% Of Japan's Corporate Heads - Nikkei Poll

-

Property Fallout To Continue In China Despite Modest Policy Easing - Fitch

-

Italy’s Fiscal Deficit Predicted To Hit 5.3% Of GDP This Year

-

Dollar Sticks Near 10-Month High, Keeping Heat On Yen

-

Japan 20-Year Bond Yield Rises To Highest Since 2014

-

Bitcoin Refuge Appeal Touted Again As US Shutdown Prospects Rise

-

WTI Oil Hits $95/Bbl For The First Time Since Aug. 2022

-

Japan's Nikkei Hits One-Month Low On Fed's Higher-For-Longer Rate Woes

-

Global Market Cap Drops Under $100tn On China Jitters, Rising Rates

-

China’s Top Developers Lost Close To $3bn Due To Weakened Renminbi

-

Evergrande Suspends Trading In Hong Kong, Along With Units

-

Micron Widens Loss Forecast, Shares Drop; Chipmaker Hopes To Supply Nvidia

(Sourced from Bloomberg, Reuters and other reliable financial news outlets)

Technical & Trade Views

SP500 Bias: Bullish Above Bearish Below 4300

-

Above 4310 opens 4330

-

Primary resistance is 4400

-

Primary objective is 4225

-

20 Day VWAP bearish, 5 Day VWAP bearish

(Click on image to enlarge)

EURUSD Bias: Bullish Above Bearish Below 1.0610

-

Above 1.06opens 1.0650

-

Primary resistance is 1.0760

-

Primary objective is 1.0477

-

20 Day VWAP bearish, 5 Day VWAP bearish

(Click on image to enlarge)

GBPUSD Bias: Bullish Above Bearish Below 1.22

-

Above 1.22opens 1.2250

-

Primary resistance is 1.2450

-

Primary objective 1.2060

-

20 Day VWAP bearish, 5 Day VWAP bearish

(Click on image to enlarge)

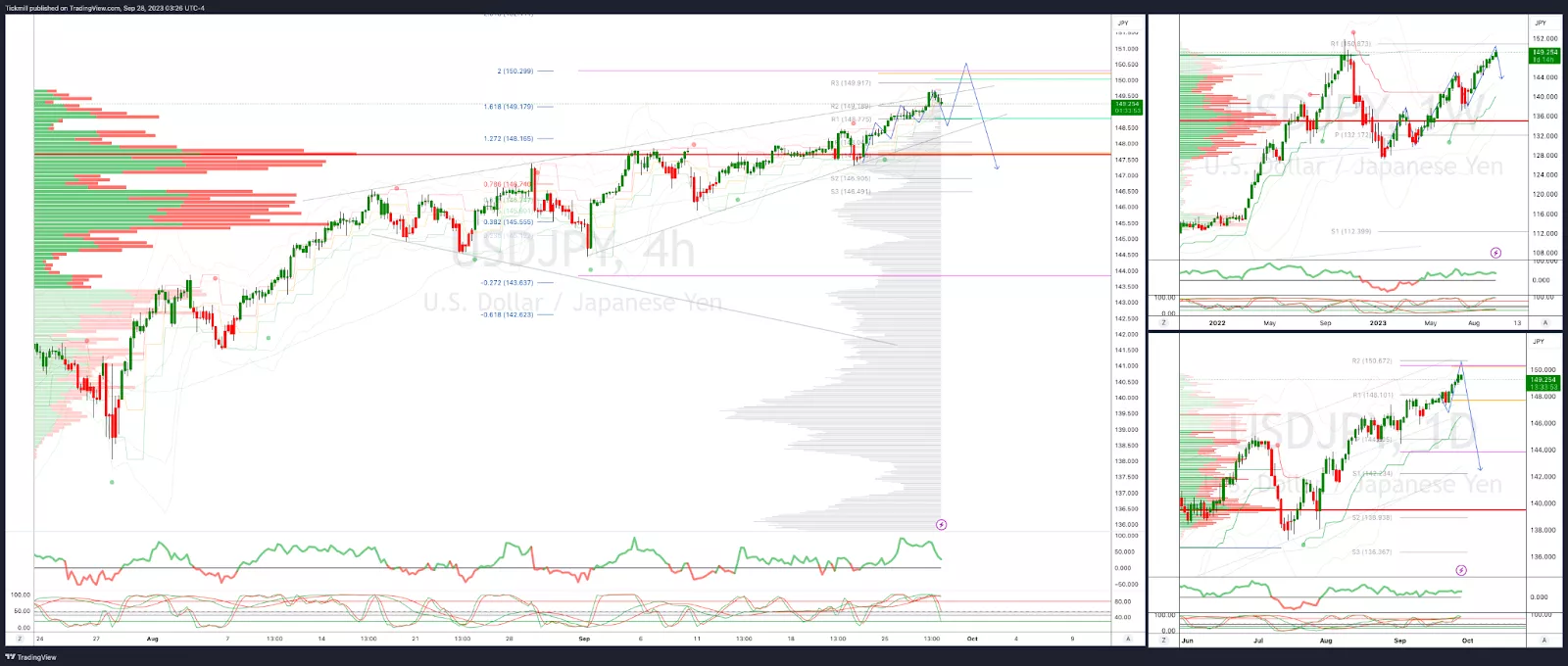

USDJPY Bias: Bullish Above Bearish Below 148.50

-

Below 148 opens 147.50

-

Primary support 144.50

-

Primary objective is 150

-

20 Day VWAP bullish, 5 Day VWAP bullish

(Click on image to enlarge)

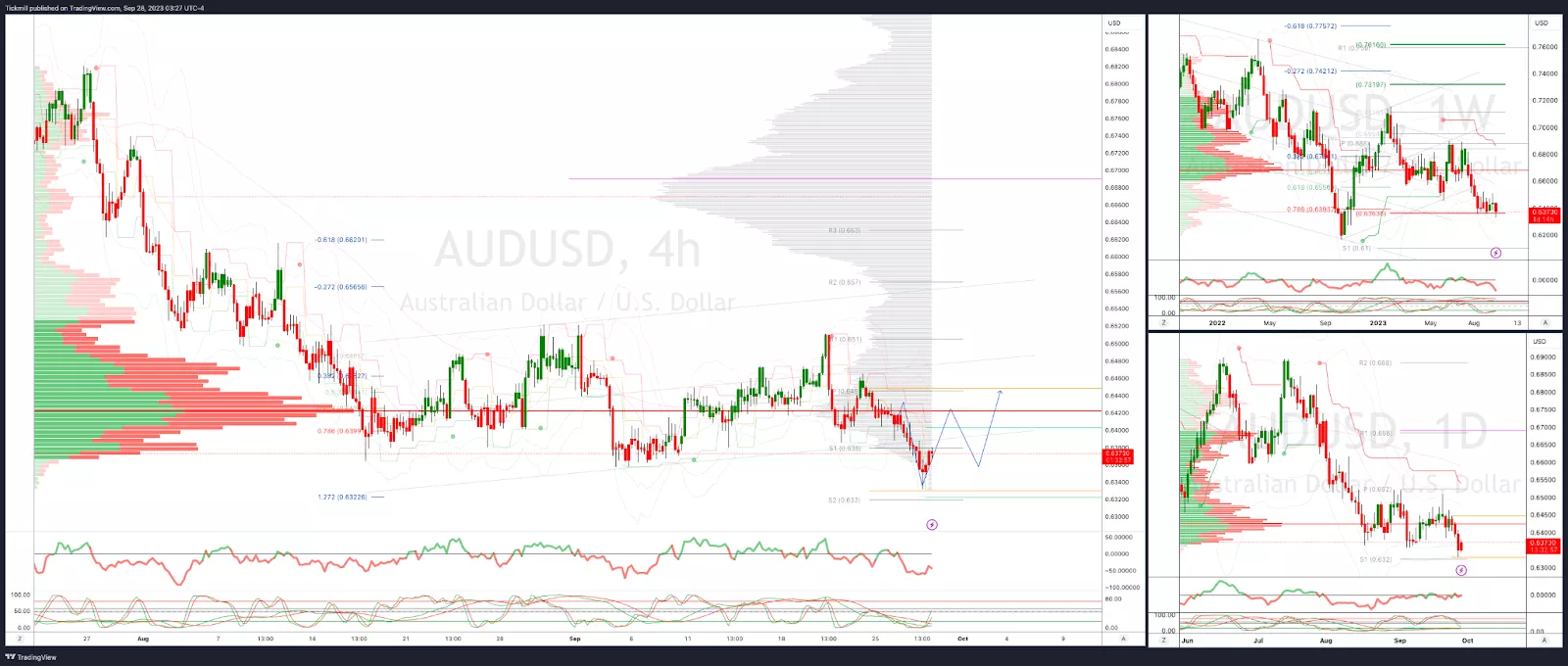

AUDUSD Bias: Bullish Above Bearish Below .6450

-

Above .6475 opens .6525

-

Primary resistance is .6620

-

Primary objective is .6320

-

20 Day VWAP bearish, 5 Day VWAP bearish

(Click on image to enlarge)

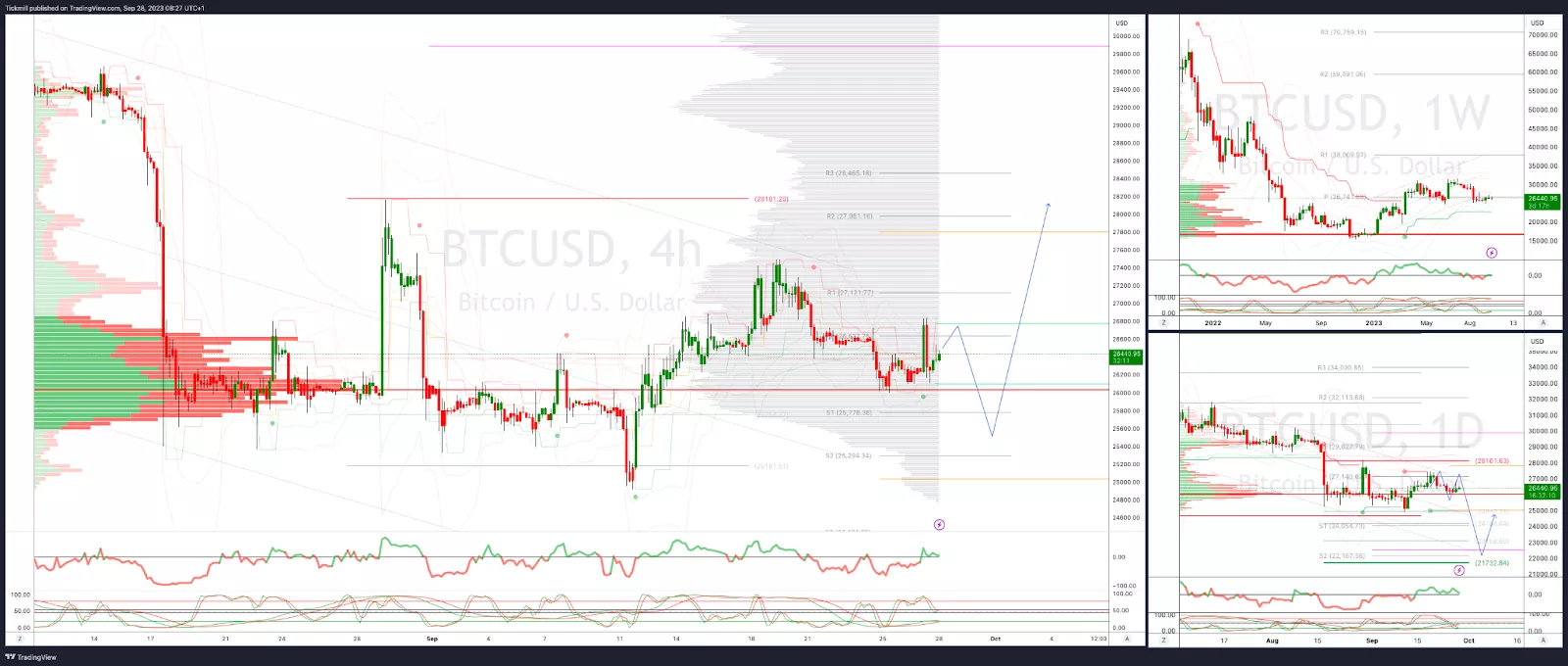

BTCUSD Bias: Bullish Above Bearish below 27500

-

Above 28200 opens 30000

-

Primary resistance is 28175

-

Primary objective is 23300

-

20 Day VWAP bearish, 5 Day VWAP bearish

(Click on image to enlarge)

More By This Author:

Increasing Interest Rate Woes Weigh On SentimentDaily Market Outlook - Wednesday, September 27

FTSE: RS Group Takeout Rumors Rally Investor Sentiment

Comments

Log in or sign up to join the conversation.