The Philadelphia Fed’s Coincident Index is out, 2.1% m/m annualized (2.6% y/y):

(Click on image to enlarge)

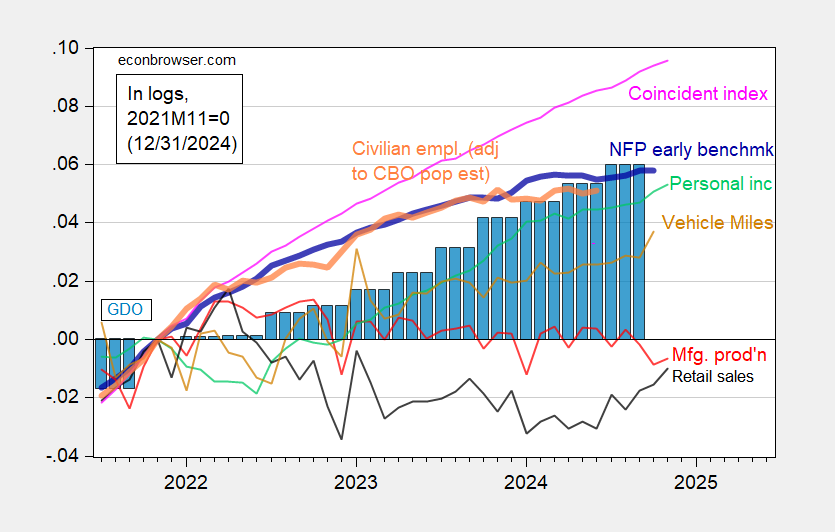

Figure 1: Implied nonfarm Payroll early benchmark (NFP) (bold blue), civilian employment adjusted using CBO immigration estimates (orange), manufacturing production (red), personal income excluding current transfers in Ch.2017$ (bold green), manufacturing and trade sales in Ch.2017$ (black), consumption in Ch.2017$ (light blue), and monthly GDP in Ch.2017$ (pink), GDO (blue bars), all log normalized to 2021M11=0. Source: Philadelphia Fed, Federal Reserve via FRED, BEA 2024Q3 third release, S&P Global Market Insights (nee Macroeconomic Advisers, IHS Markit) (12/2/2024 release), and author’s calculations.

Of the above, only personal income ex-transfers (light green) is a NBER BCDC key series (BCDC key series shown here).

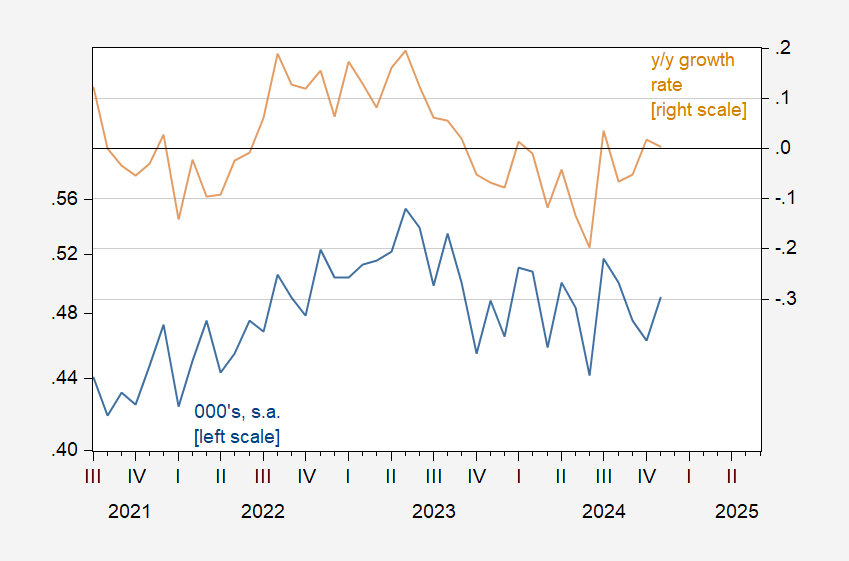

A favorite indicator of mine is heavy truck sales.

(Click on image to enlarge)

Figure 2: Heavy truck sales, 000’s (blue, left log scale), year-on-year growth rate (tan, right scale). Source: BEA via FRED,and author’s calculations.

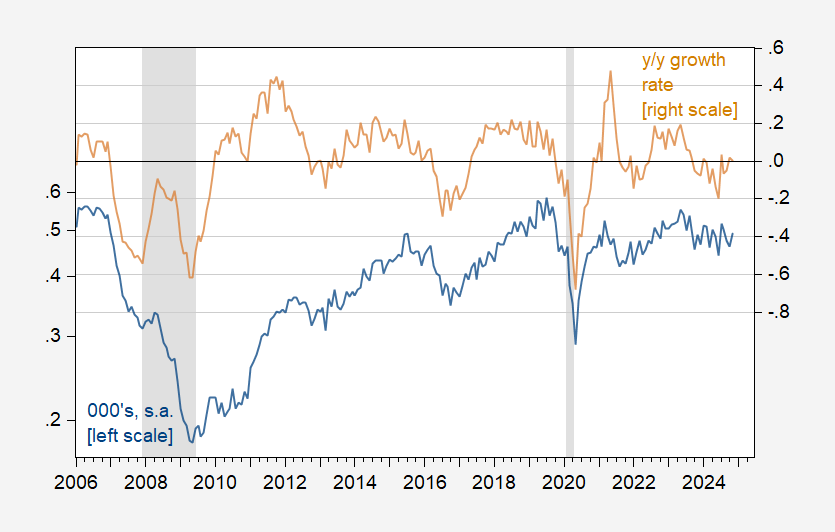

It’s hard to see whether this indicates recession, even though we’re past a local peak. For context, here’s the evolution of these series before the last two recessions.

(Click on image to enlarge)

Figure 3: Heavy truck sales, 000’s (blue, left log scale), year-on-year growth rate (tan, right scale). NBER defined peak-to-trough recession dates shaded gray. Source: BEA via FRED, NBER, and author’s calculations.

On the basis of the y/y growth rate, you didn’t think we were headed to recession in 2019, then you shouldn’t think we are in 2024.

More By This Author:

Year End Disinversion: Bull Or Bear Steepening?What If? Thoughts On The No Excess Demand Scenario

Revisiting The Relationship Between Debt And Long-Term Interest Rates

Comments

Log in or sign up to join the conversation.