3 Things: CB’s All In, Japan, Bond Bull

Who’s Buying It?

With the market breaking out to all-time highs, the media has started to once again reach for their party hats as headlines suggest clear sailing for investors ahead.

While I certainly do not disagree the breakout is indeed bullish, and signals a continuation of the long-term bullish trend, there are more than sufficient reasons to remain somewhat cautious. Earnings are still weak, there is little evidence of economic resurgence and inflationary pressures globally remain nascent. But, for now, a rash of global Central Banks continue to support asset prices by increasing accommodative policies either through additional reductions in interest rates or direct injections of liquidity. As Matt King from Citi recently noted:

“It has been a surge in net global central bank asset purchases to their highest level since 2013.”

With the ECB in full QE mode, the BOC now using $300 billion in Pension Funds to prop up prices, and the BOJ now moving towards an additional $130 billion in QE as well, the liquidity push continues.

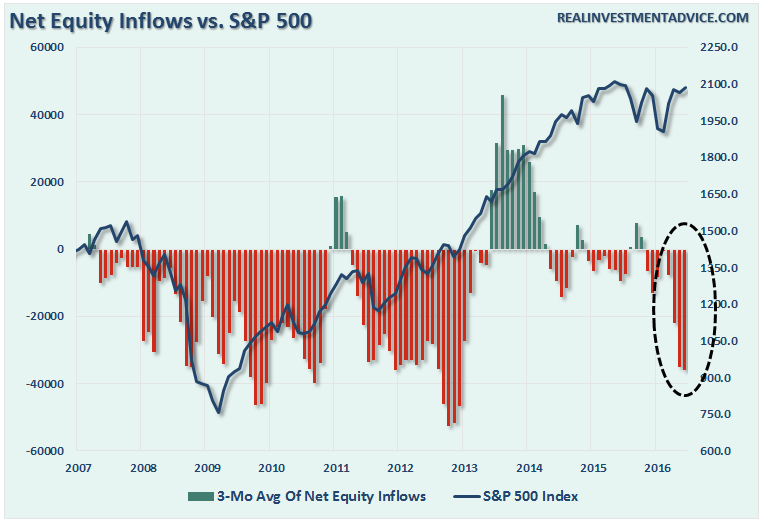

Interestingly, despite the push by Central Banks to loft asset prices higher, individual market participants as measured by the Investment Company Institute (ICI) have a different idea.

As shown in the chart above, despite asset prices ringing all-time highs, net equity inflows have turned decisively negative. This was much the same case following the 2012 market rout and it wasn’t until the launch of QE3 in 2013 that investors began to once again chase the markets.

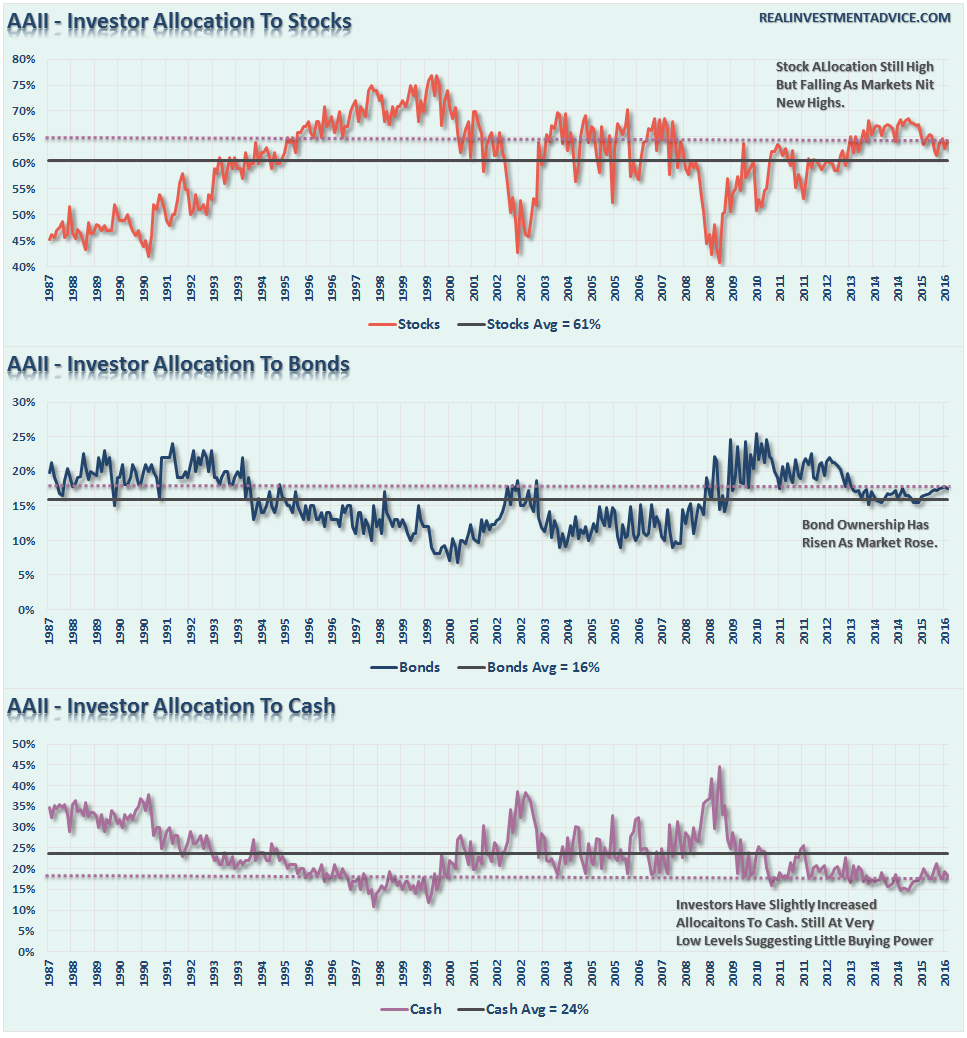

The same can be seen for the American Association of Individual Investors as shown below.

(Click on image to enlarge)

While the ICI chart above shows “net flows,” the AAII chart shows percentage allocated to stocks, bonds and cash.The recent decline in percentage of stock holdings confirms the recent net equity outflows from ICI.

However, despite the outflows from stocks, and increased allocation to bonds in recent months, the net exposure to equity risk by individuals remains at historically high levels with cash near historically low levels. Such suggests two things:

- There is little buying left from individuals to push markets marginally higher, and;

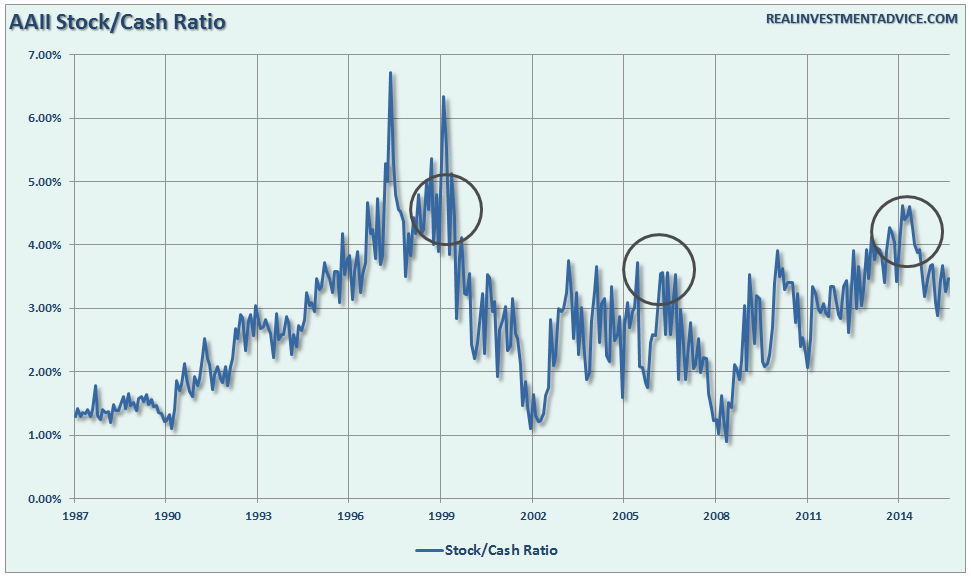

- The stock/cash ratio, shown below, is at levels normally coincident with more important market peaks.

Here is the point, despite ongoing commentary about mountains of “cash on the sidelines,” this is far from the case. This leaves the current advance in the markets almost solely in the realm of Central Bank activity.

Of course, there is nothing wrong with that…until there is.

The question that everyone should be asking themselves is this:

“If the markets are rising because of expectations of improving economic conditions and earnings, then why are Central Banks pumping liquidity like crazy?”

Someone is going to be very wrong.

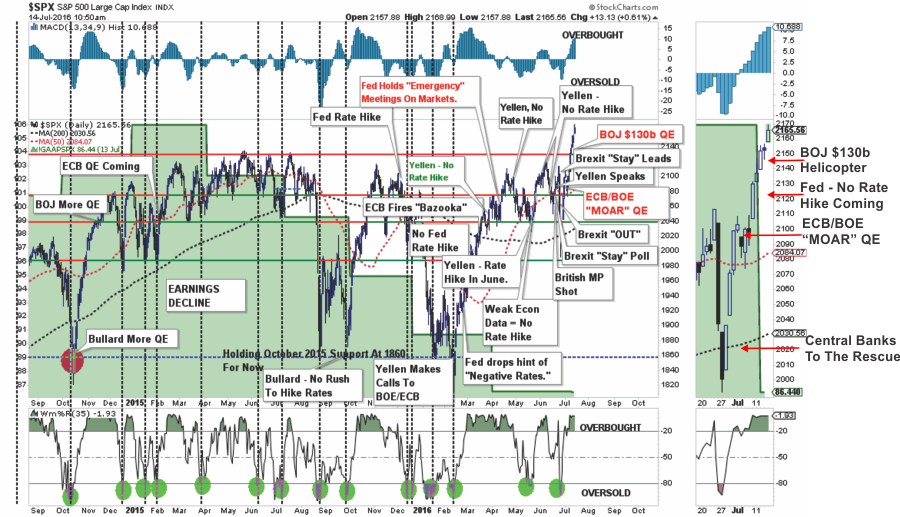

Market Surge Might Have A Problem

The recent surge in the market, as I discussed earlier this week, was directly due to the expectation of “helicopter money” from Japan. Of course, as I have shown before, the recent market surges have been almost entirely due to the ongoing rhetoric from Central Banks globally, most recently to “save the markets” from the “Brexit.”

(Click on image to enlarge)

First of all, let’s remember that while “helicopter money” may seem like a good idea in the short-term, it is not a long-term solution as it shrinks the middle-class which is the ultimate driver of economic growth.

- Using monetary policy to drag forward future consumption leaves a larger void in the future that must be continually refilled.

- Monetary policy does not create self-sustaining economic growth and therefore requires ever larger amounts of monetary policy to maintain the same level of activity.

- Japan’s program will continue to push the Yen lower and the dollar higher. This will suppress oil prices, exports and ultimately earnings growth expectations leaving a larger gap between market prices and fundamentals.

- The filling of the “gap” between fundamentals and reality leads to consumer contraction and ultimately a recession as economic activity recedes.

- Job losses rise, wealth effect diminishes and real wealth is destroyed.

- Middle class shrinks further.

- Central banks act to provide more liquidity to offset recessionary drag and restart economic growth by dragging forward future consumption.

- Wash, Rinse, Repeat.

If you don’t believe me, here is the evidence from Jim Quinn:

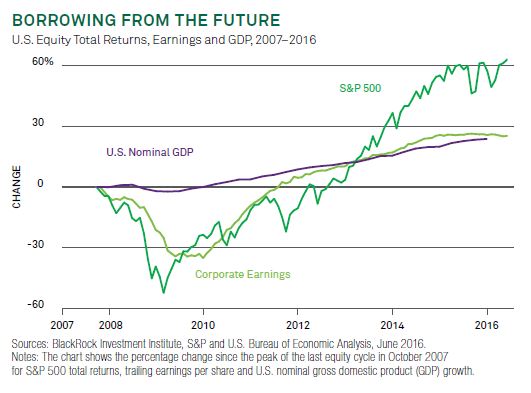

“The stock market has returned 60% since the 2007 peak, three times the growth in corporate profits and GDP.The all-time highs in the stock market have been driven by the $3.4 trillion increase in the Fed’s balance sheet, hundreds of billions in stock buybacks, PE expansion, and ZIRP. The valuation of the median stock is now the highest in history.”

Secondly, while the markets are rallying on hopes of “helicopter money” from Japan, the reality is those expectations may be misplaced. According to Reuters:

“There is no chance Japan will resort to ‘helicopter money.’

The Bank of Japan already gobbles up more government bonds than is sold to the market each month under its massive monetary stimulus program – dubbed ‘quantitative and qualitative easing’ (QQE) – deployed in 2013.

With the BOJ already keeping borrowing costs near zero with aggressive money printing, there is no strong push from premier Shinzo Abe’s administration to revise the law and force the central bank to resort to helicopter money, said the officials, who declined to be named due to the sensitivity of the matter.

It is also prohibited by law to directly underwrite government debt, which means parliament needs to revise the law for the central bank to start directly bank-rolling debt.”

Oops.

Bond Bull Ain’t Dead, Just Resting

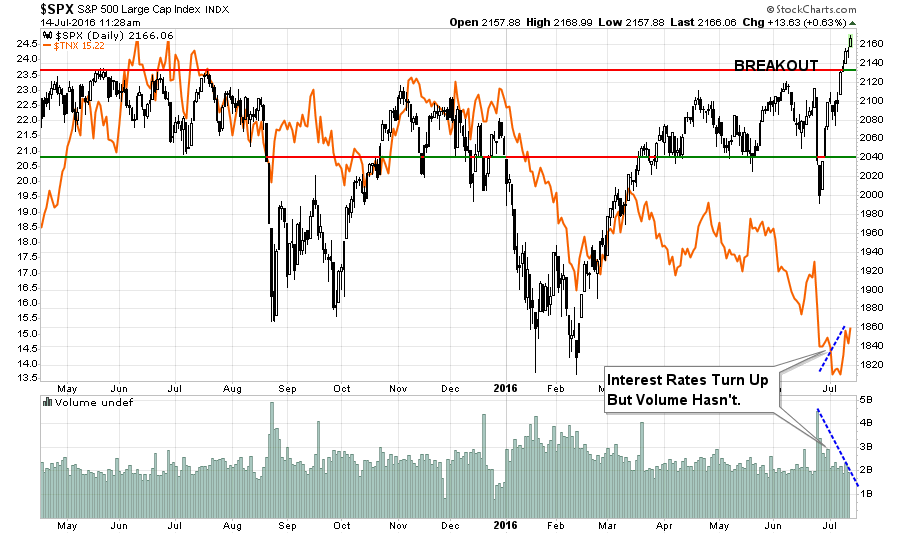

This past Monday, as the markets broke out to new all-time highs, I increased net equity exposure in portfolios.However, I also took one other action which was to short interest rates to hedge the bond exposure in accounts.

“While the breakout has yet to be confirmed through the end of this week, interest rates have turned up suggesting a rotation, at least temporarily, from ‘safety’ back into ‘risk.’ Unfortunately, a pickup in volume to confirm conviction to the move is still lacking at the moment.”

The chart below is updated through this morning. Nothing has changed.

(Click on image to enlarge)

So, while I shorted interest rates to hedge bond portfolios, this is a risk-management decision to maintain allocation structures and protect capital.

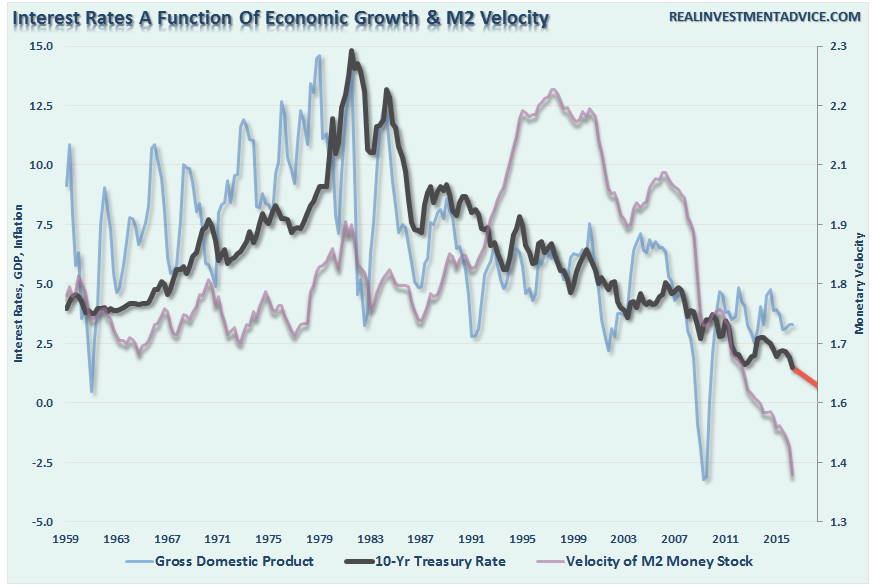

However, longer-term, as shown in the chart below, I expect rates to fall further.

How much further?

Like below 1% further.

(Click on image to enlarge)

With monetary velocity in a sharp decline, as monetary policy is a direct retardant to the demand for money through the system, and economic growth weakening, interest will fall further to reflect the weak economic environment. This will occur during the onset of the next recession.

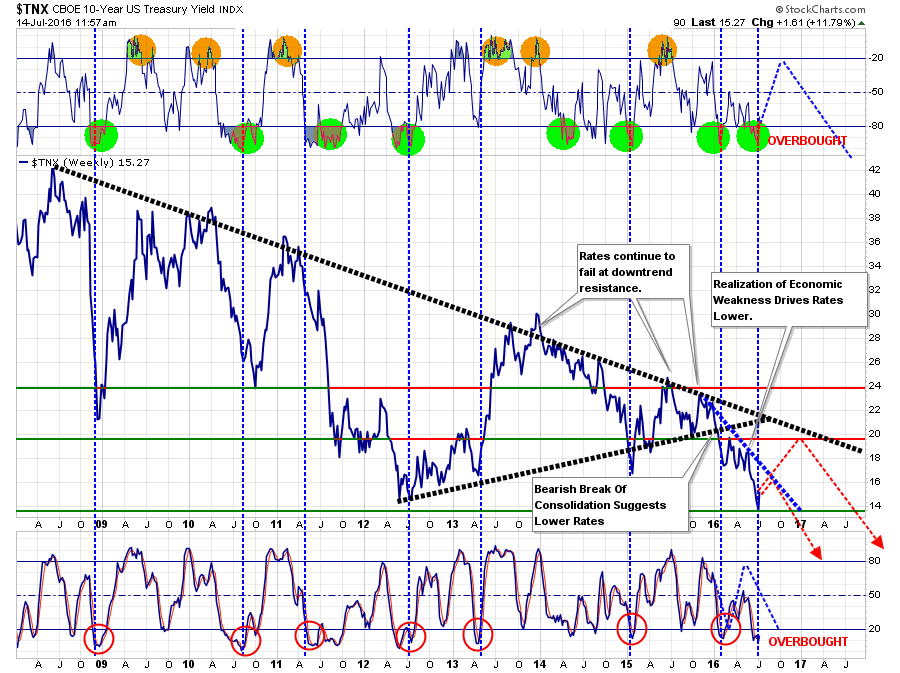

In the meantime, however, I think there is a reasonable probability, if the market has indeed entered a market “melt up”stage discussed previously, rates could rise back to the top of the current downtrend around 1.8-1.9%.

(Click on image to enlarge)

If the current rally fails, and we continue to the current long-term market topping process, then rates would like stall out at roughly 1.6%.

As you can see we are currently playing with very small ranges. However, when it comes to rates even small movements can have a large impact on long-duration holdings. From a portfolio management perspective, hedging interest rate risk currently is well worth the cost of insurance.

Betting on the “end of the bond bull market” is a trade I wouldn’t take.

Why? Interest rates are relative.

With global rates at zero to negative, money will continue to chase U.S. Treasuries for the higher yield. This will continue to push yields lower as the global economy continues to slow. What would cause this to reverse? It would require either an economic rebound as last seen in 50’s and 60’s or a complete loss of faith in the U.S. to pay its debts such as a collapse of the Government and the onset of the “zombie apocalypse.”

We no longer have the drivers of manufacturing, demographics or credit expansion for the former, so I am ready for the latter.

Just some things I am thinking about.

Disclosure: The information contained in this article should not be construed as financial or investment advice on any subject matter. Streettalk Advisors, LLC expressly disclaims all liability in ...

more

Nice article. #HelicopterMoney appears to be quite illegal in Japan. So, even perpetual bonds, with zero interest rates, would be a form of helicopter money that may be illegal as well. We would have to see the bonds to believe they would ever exist. Real helicopter money, as defined by Eric Lonergan, would help the real economy worldwide. But it requires an unsterilized expansion, one time only, of base money. I can't see Japan seeing that as being "clean". I wrote about it in my last article.