The media is full of articles about the financial situation of Millennials in today’s economy. According to numerous surveys, they are saddled with too much debt, can’t secure higher wage-paying jobs, and are financially distressed on many fronts. Moreover, this is occurring during the longest financial and economic boom in the history of the United States.

Of course, the media is always there to help by chastising boot-strapped Millennials to dump their savings into the financial markets to chase overvalued, extended, and financially questionable stocks.

To wit:

“Only about half of American families are participating in some way in the stock market, according to research from the St. Louis Fed. When it comes to millennials (ages 23 to 38), about 60% have no direct or indirect exposure to the stock market.

Of course, you don’t definitely don’t have to invest, Erin Lowry, author of ‘Broke Millennial Takes on Investing,’ tells CNBC Make It. It’s not a life requirement. But you should understand what you’re losing out on if you avoid the markets. It’s a shocking amount, Lowry says. ‘You’re going to have to save so much more money to achieve the same goals because the market is helping do some of the work.’”

Great, you have a person with NO financial experience advising Millennials to put their “savings” into the single most difficult game on the planet.

Of course, this is all dependent on the same “myth” we just addressed last week:

“That’s because when you use a high-yield savings account or an investment account with higher returns, you put the magic of compound interest to work for you. When your money earns returns, those returns also generate their own earnings. It’s that simple.”

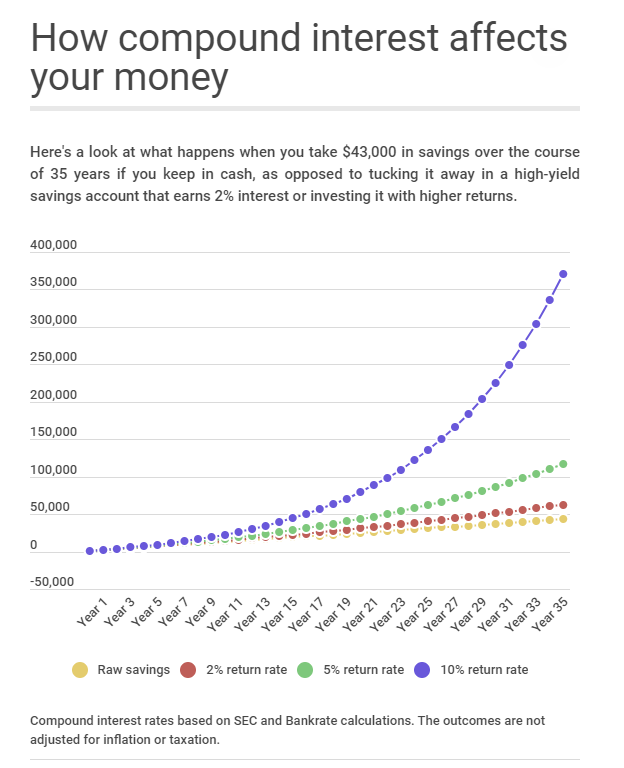

Here’s the math they use to prove their point.

“Let’s say you have $1,000 and add $100 a month to your savings over the course of 35 years. At the end, you’d have $43,000. Not bad. But if you had invested that money and earned a 10% rate of return, which is in line with average historic levels, you’d have over $370,000.”

Of course, you have to have a cool chart to go along with it.

Here’s a little secret.

It’s a complete fallacy.

From CNBC:

“Of course, investing is not risk-free. Typically, investors see some years where they earn double-digit returns and other years where they experience a loss. Losses happens, on average, about one out of every four years, and can be bad. During a bear market — which is when stocks fall by at least 20% — research shows that the market drops by an average of 30%. That condition typically lasts for about 13 months.

That means if you invested $1,000 and the market lost 30%, your investment would be worth $700. And it may take you more than 13 months to recover the $300 you lost.”

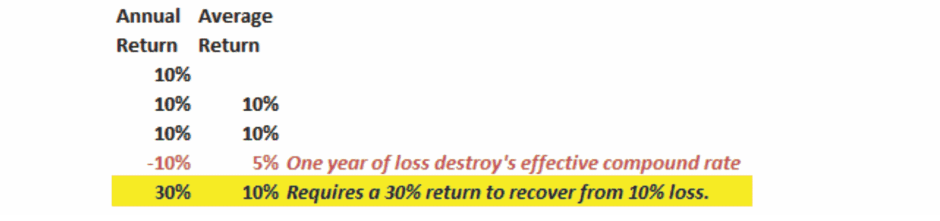

The importance of that statement is that “losses” destroy the “power of compounding.”

Let’s assume an investor wants to compound their investments by 10% a year over a 5-year period.

The ‘power of compounding’ ONLY WORKS when you do not lose money. As shown, after three straight years of 10% returns, a drawdown of just 10% cuts the average annual compound growth rate by 50%. Furthermore, it then requires a 30% return to regain the average rate of return required. In reality, chasing returns is much less important to your long-term investment success than most believe.”

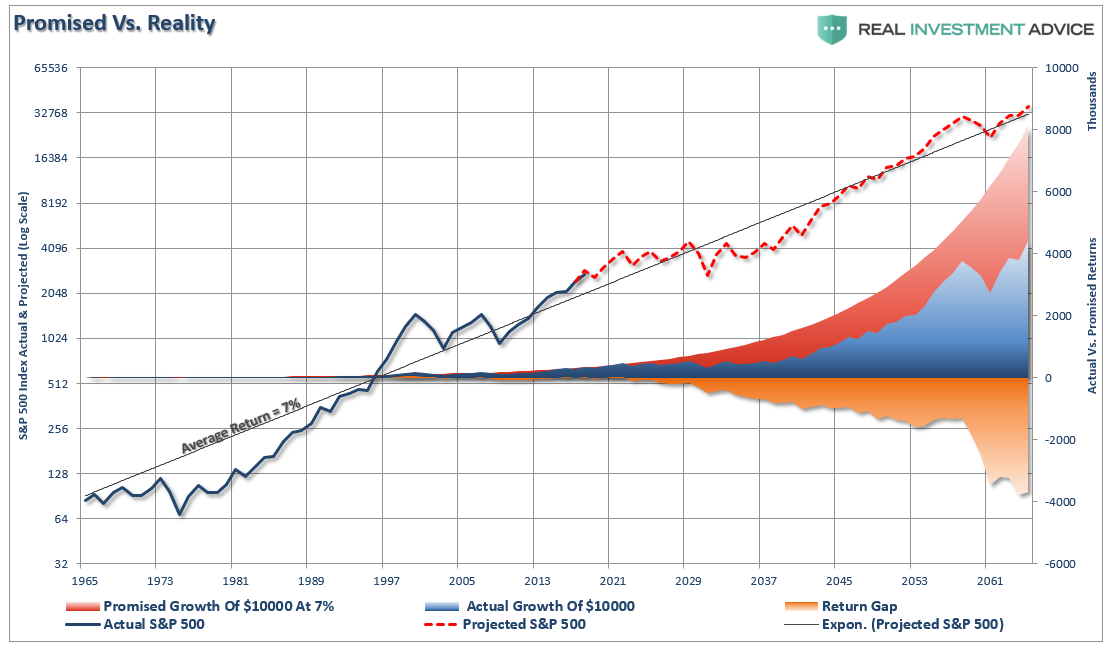

When imputing volatility into returns, the differential between what investors were promised (and this is a huge flaw in financial planning) and what actually happened to their money is substantial over long-term time frames.

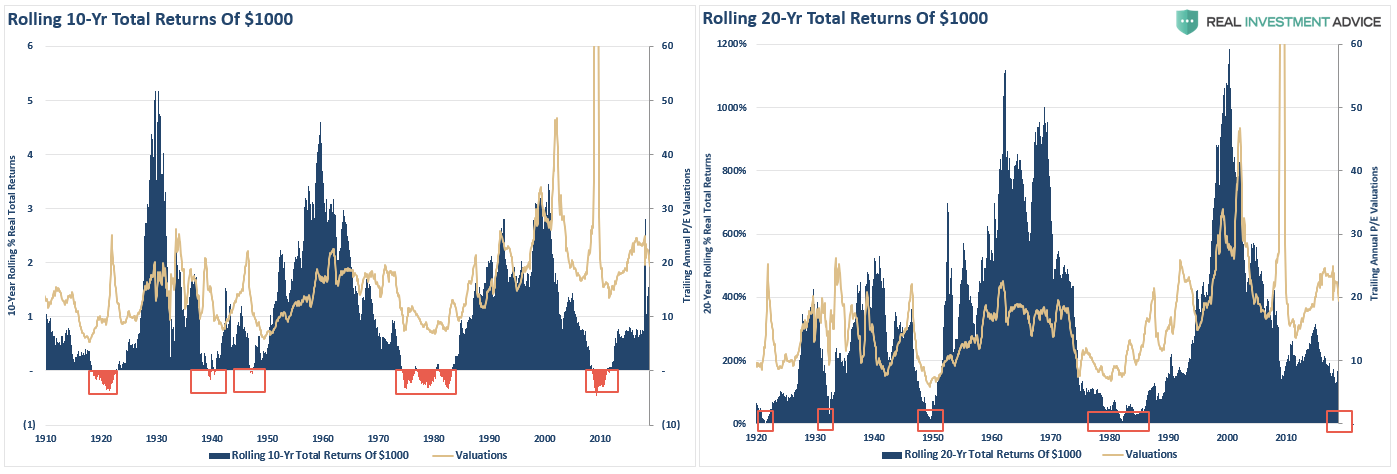

Here is another way to look at it.

If you could simply just stick money in the market and it grew by 6% every year, then how is it possible to have 10 and 20-year periods of near ZERO to negative returns?

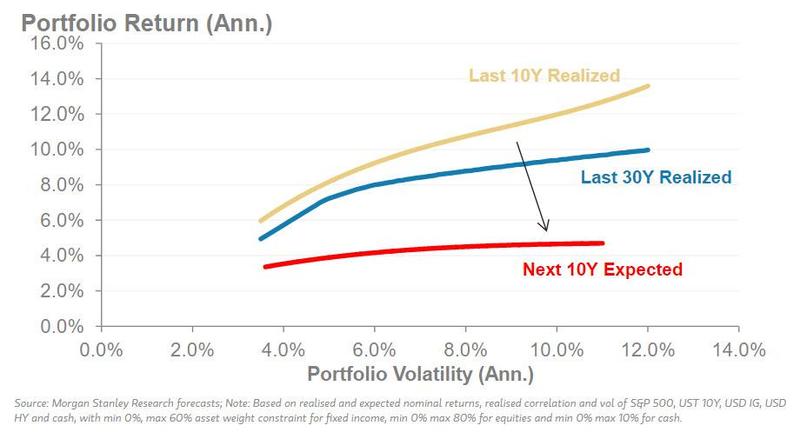

Morgan Stanley just recently published research on this exact issue:

“On our estimates, the expected return of a US 60/40 portfolio of stocks and government bonds will return just 4.1% per year over the next decade, close to the lowest expected return over the last 20 years, and one that has only been worse in 4% of observations since 1950.”

4.1% isn’t 6, 8 or 10%.

There went your savings plan.

The level of valuations when you start your investing journey is all you need to know about where you are going to wind up. Based on current valuations, if you are betting on the last decade of returns to continue 30-years into the future, you are likely going to be very disappointed.

Don’t Forget The Impact Of Inflation

Here’s the second problem.

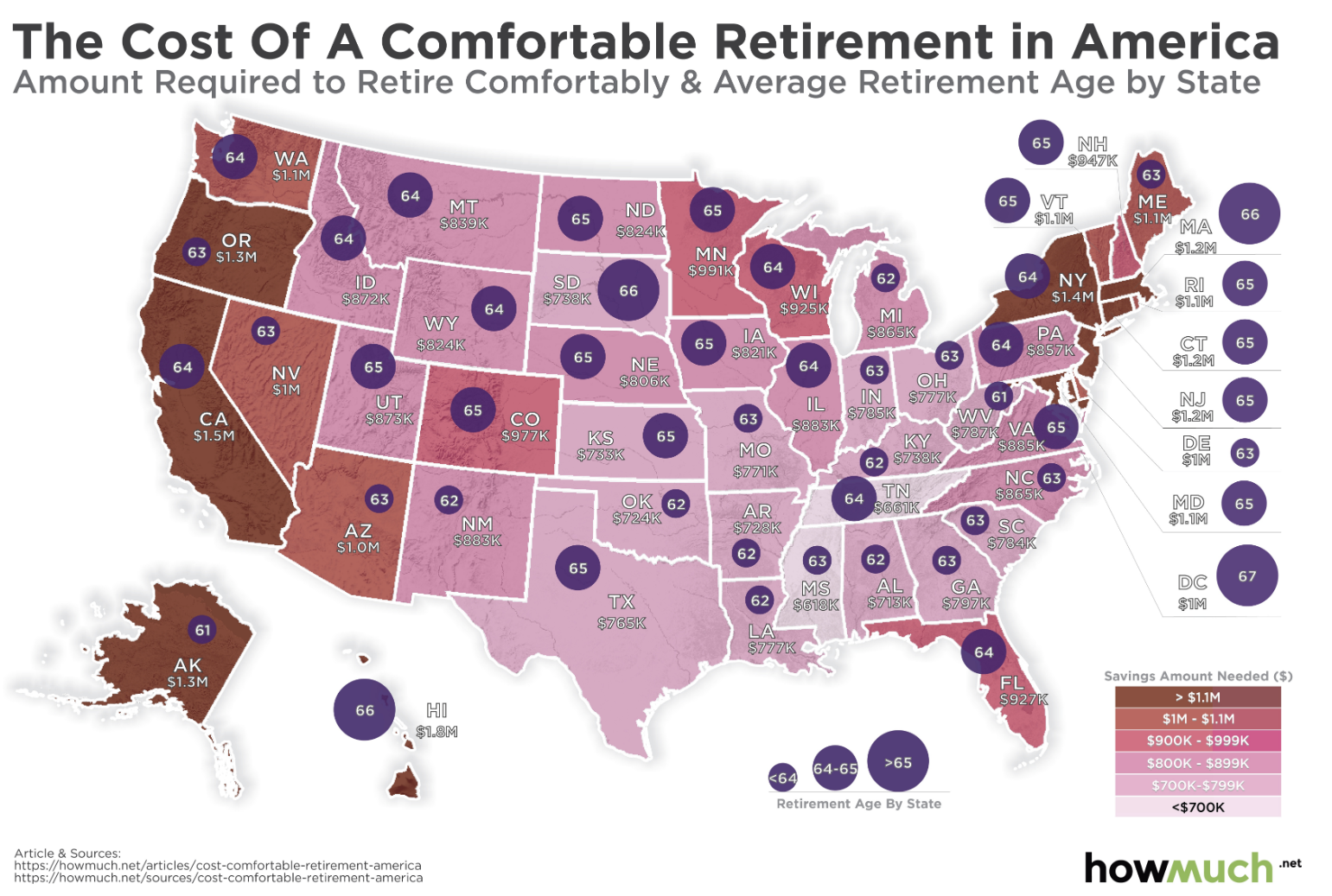

A recent article from MarketWatch pointed out how much it would cost to retire in each state. Using data from the BLS, Howmuch.net created the following visual.

“The average yearly expenses across the country for someone over the age of 65 is $51,624, but that figure comes in at $44,758 in the low-cost-of-living Mississippi and a whopping $99,170 on the other end of the spectrum in the Aloha State. ‘

This is misleading as the amounts shown above are based on TODAY’s data and what is required if you want to RETIRE TODAY.

What happens if you are a Millennial wanting to retire in 30-years? While $1 million sounds like a lot of money today and might net you a comfortable retirement in Colorado ($1 million at a 3% annual withdrawal rate nets you $30,000 plus social security), will it be enough in 30-years?

Probably not. Let’s run it backwards.

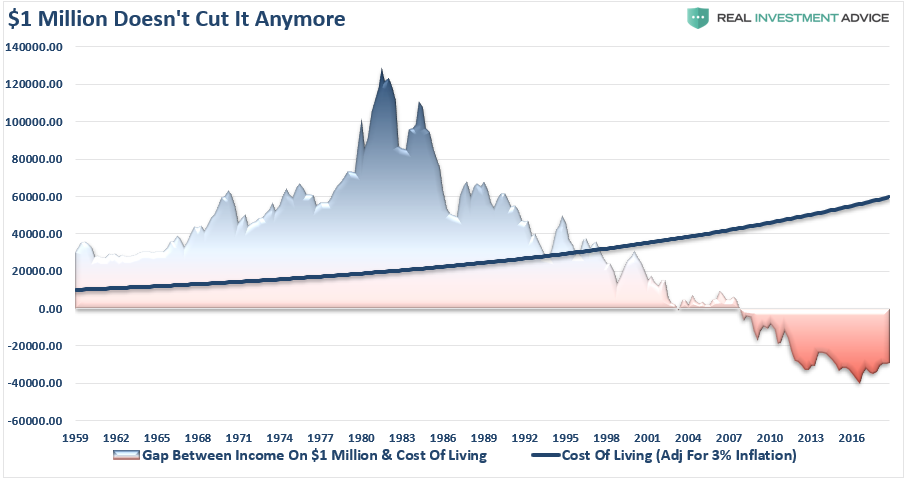

In 1980, $1 million would generate between $100,000 and $120,000 per year while the cost of living for a family of four in the U.S. was approximately $20,000/year. Today, there is about a $40,000 shortfall between the income $1 million will generate and the cost of living.

This is just a rough calculation based on historical averages. However, the amount of money you need in retirement is based on what you think your income needs will be in the future, not today, and how long you have to reach that goal.

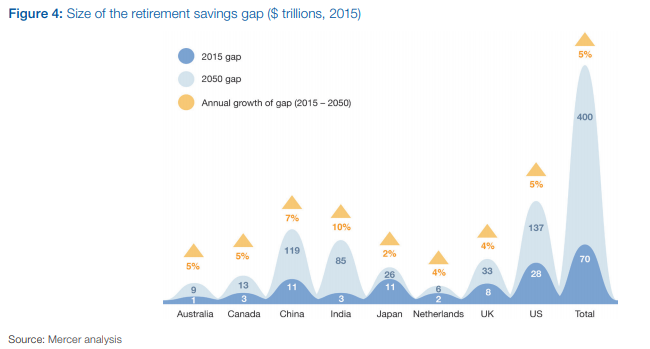

For most, there is a desire to live a similar, or better, lifestyle in retirement. However, over time, our standard of living will increase to reflect our life-cycle stages. Children, bigger houses to accommodate those children, education, travel, etc. all require higher incomes. (Which is the reason the U.S. has the largest retirement savings gap in the world.)

If you are like me with four kids, “a million dollars ain’t gonna cut it.”

The problem with Erin Lowry’s advice to her “millennial cohorts,” is not just the lack of accounting for variable rates of returns, but impact of inflation on future living standards.

Let’s run an easy example.

- John is 23 years old and earns $40,000 a year.

- He saves $14 a day

- At 67 he will have $1 million saved up (assuming he gets the promised 10% annual rate of return)

- He then withdraws 4% of the balance to live on matching his $40,000 annual income.

That’s pretty straightforward math.

The problem is that it’s entirely wrong.

The living requirement in 44 years is based on today’s income level, not the future income level required to maintain the SAME living standard.

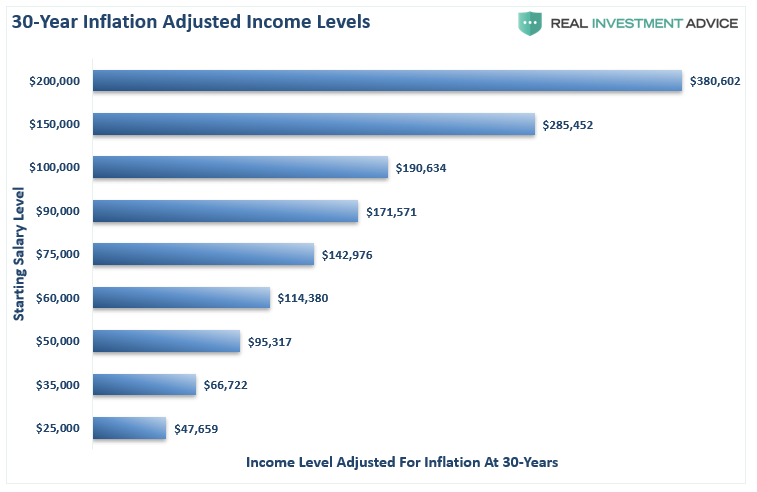

Look at the chart below and select your current level of income. The number on the left is your income level today and the number on the right is the amount of income you will need in 30-years to live the same lifestyle you are living today.

This is based on the average inflation rate over the last two decades of 2.1%. However, if inflation runs hotter in the future, these numbers become materially larger.

The chart above exposes two problems with the entire premise:

- The required income is not adjusted for inflation over the savings time-frame, and;

- The shortfall between the levels of current income and what is actually required at 4% to generate the income level needed.

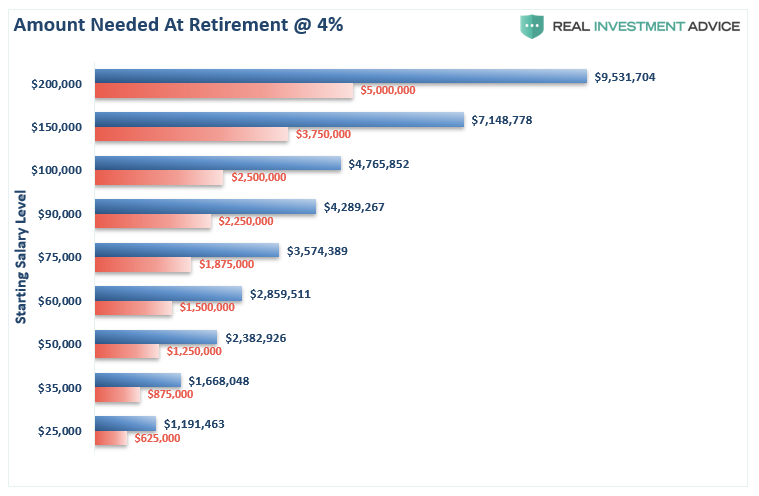

The chart below takes the inflation-adjusted level of income for each brackets and calculates the asset level necessary to generate that income assuming a 4% withdrawal rate. (For comparison purposes, the red bar is the “F.I.R.E. Movement” recommendation of 25x your income.)

If you need to fund a lifestyle of $100,000, or more, in today’s dollars, as Sheriff Brody quipped in “Jaws,”

“You are going to need a bigger boat.”

Not accounting for the future cost of living is going to leave a lot of people short, even including social security.

While authors like Ms. Lowry are creating a nice income for themselves by selling books to “broke Millennials,” the content is only as good as the current market cycle you are in. Ms. Lowry and her cohorts have never been through a bear market.

Mean reverting events expose the fallacies of “buy-and-hold” investment strategies. The “stock market” is NOT the same as a “high yield savings account,” and losses devastate retirement plans. (Ask any “boomer” who went through the dot.com crash or the financial crisis.”)

Unfortunately, for individuals, the results between what is promised and what occurs continue to be two entirely different things, and generally not for the better.

Comments

Log in or sign up to join the conversation.