Burton Malkiel, author of the book A Random Walk Down Wall Street, asserted, “The facts suggest that successful market timing is extraordinarily difficult to achieve.”1

Multi-factor indices may be a way of ensuring you are “in the right place at the right time”, participating throughout market cycles without compromising timing or returns.

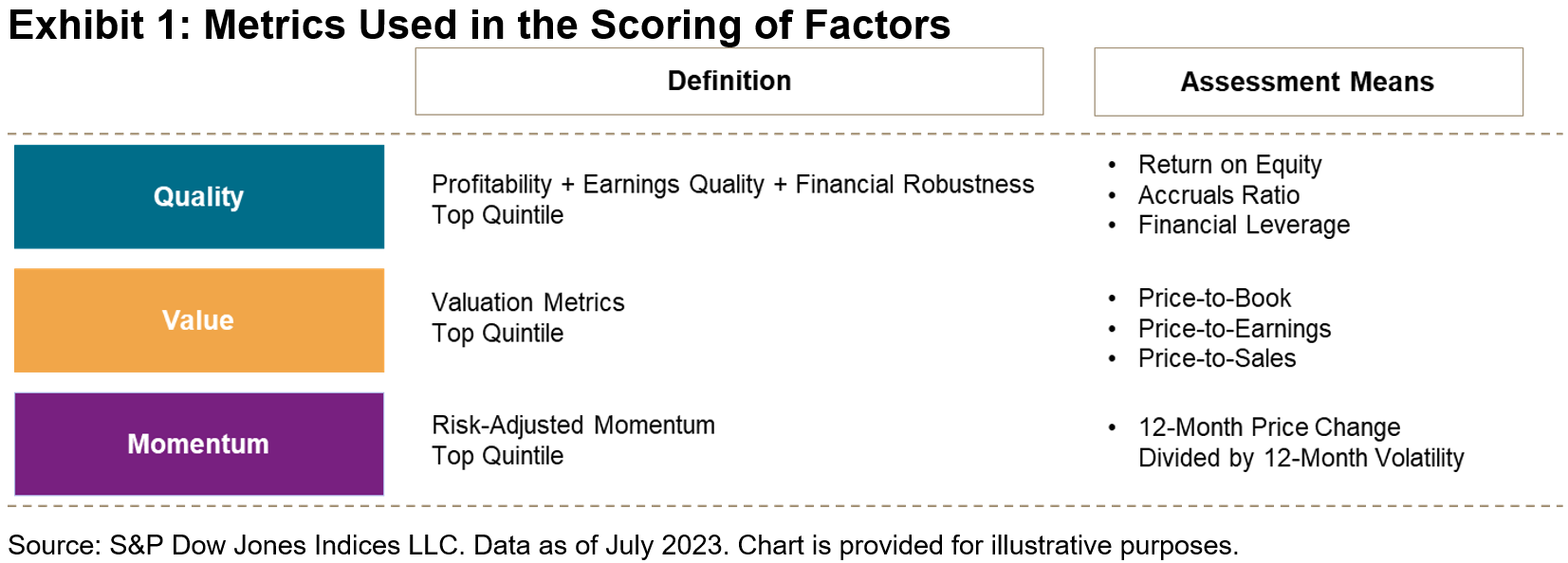

The S&P DJI Multi-Factor Indices are built on a bottom-up methodology. This means the factor scores are combined to select “all-rounders” that score highly across multiple factors. The S&P South Africa Composite Quality, Value & Momentum (QVM) Multi-factor Index utilizes the Quality, Value and Momentum factors. The illustration below shows the metrics used in the scoring for each individual factor.

(Click on image to enlarge)

To be eligible for inclusion in the S&P South Africa Composite QVM Multi-factor Index, the constituents must be members of the S&P South Africa Composite and pass a trading liquidity screen. Multi-factor scores are calculated for each company based on the average for each factor. The top 40 constituents with the highest factor score are included in the index. All constituents are market capitalization times factor score weighted, to a maximum weight of 10%.

The methodology enables various benefits to be built into the index. Stocks are selected within the context of the total combined portfolio and overall exposures to the desired factors may be higher. Additionally, back-tested results show stronger risk-adjusted returns than the index of indices approach.

Multi-factor indices have historically tended to perform more strongly over the longer term on a risk-adjusted basis. This improved dynamic is demonstrated by returns being closer to the top left in Exhibit 2. The S&P South Africa Composite QVM Multi-factor Index is nearer this point than other indices.

(Click on image to enlarge)

We show the S&P South Africa Composite QVM Multi-factor Index returns on a yearly basis with the individual factor returns overlaid in Exhibit 3. The S&P South Africa Composite QVM Multi-factor Index line demonstrates how the individual factor returns are working together over various years to deliver the risk-adjusted return.

(Click on image to enlarge)

The correlations across excess returns between factors are low, which allows for the potential benefits from combining individual factors within the S&P South Africa Composite QVM Multi-factor Index approach.

(Click on image to enlarge)

Exhibit 5 shows the risk-adjusted returns over time for each of the factors. The S&P South Africa QVM Multi-factor Index provides good returns over the long-term with lower tracking error against the S&P South Africa Composite. It also participates well in rising markets but avoids some of the downside in falling markets, reflecting the benefits of the multi-factor approach.

The S&P South Africa Composite QVM Multi-factor Index provides an interesting opportunity to consider for multi-factor indexing in the South African market.

1 Malkiel, Burton. A Random Walk Down Wall Street. W. W. Norton & Company, Inc. 1973.

More By This Author:

Balancing Defense With Growth: The S&P Quality Indices

4 Ways To Compare Asian And U.S. Dividend Markets

Dividends And Option Premiums: A Dual Income Story

Comments

Log in or sign up to join the conversation.