Image Source: Pexels

The big bank stocks have been laggards in the ongoing market pullback, though the Finance sector as a whole has held up relatively well on the back of strength in the insurance and regional bank spaces.

It will be interesting to see if the group’s stock market fortunes will change in any way as JPMorgan (JPM - Free Report) and Citigroup (C - Free Report) kick-start the Q3 reporting cycle for the group on Friday, October 14th.

The chart below shows the year-to-date performance of JPMorgan (blue line; down -31.7%) and Citigroup (green line; -28.7%), relative to the S&P 500 index (red line; -22.1%), the Zacks Finance sector (orange line; -20.3%) and the Zacks Tech sector (purple line; -33.2%).

Image Source: Zacks Investment Research

As you can see above, JPMorgan shares are practically neck-to-neck with the Tech sector in the year-to-date period.

The performance variance between JPMorgan and Citigroup this year, while not much, is nevertheless likely a function of the latter’s persistent earlier underperformance that Citigroup’s new management has been trying to account for through a strategic restructuring and repositioning.

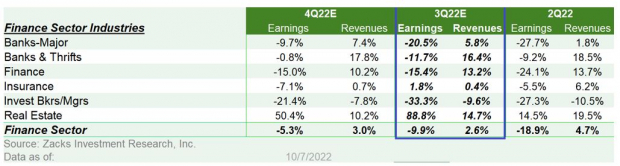

Bank Earnings Expectations

With respect to current earnings expectations for the group, Q3 earnings for the Zacks Finance sector are expected to be down -9.9% on +2.6% higher revenues. For the Zacks Major Banks industry, of which JPMorgan and Citigroup are a part, Q3 earnings are expected to be roughly a fifth below the year-earlier level on +5.8% higher revenues.

The table below shows the Zacks Finance sector’s 2022 Q3 earnings and revenue growth expectations in the aggregate as well as at the constituent medium industry level.

Image Source: Zacks Investment Research

For JPMorgan, Q3 earnings are expected to be -25.3% below the year-earlier level on +8.5% higher revenues, while the same for Citigroup are currently expected to change -42.2% and +7.6% respectively on a year-over-year basis.

The primary reason for the big year-over-year decline in Q3 earnings for the banks is the very high level of reserve releases in the year-earlier period.

You would recall that the banks had booked significant reserves or provisions for loan losses as the pandemic took hold, which they subsequently released. Booking reserves is a direct hit to earnings and its subsequent release boosts profitability. This makes year-over-year comparisons somewhat misleading.

Most analysts look at bank profitability yon a so-called ‘pre-provision’ basis, which strips out the impact of such reserves. If we looked at bank profitability for 2022 Q3 on such a ‘pre-provision’ basis, they are essentially flat from the year-earlier level.

If we look at a money-center bank like JPMorgan, we find that the commercial banking business is actually doing very well, with improved margins and modestly higher loan volumes offsetting weakness in the mortgage business and rising expenses. We know from Fed data that loan growth in the aggregate was up nicely in Q3, with credit card outlays particularly strong. In fact, other than home equity loans, all other loan categories should be up in the high single digits range in Q3.

The positive revenue growth expected for JPM is reflective of the expected strong net interest income, a direct function of expanded margins and bigger loan volumes.

On the capital markets side, the investment banking business is down significantly from the year-earlier level, perhaps by as much as -50%, with both M&A and capital raising activities materially down.

On the trading front, we are up against record volumes from the year-earlier level. But overall trading volumes, in the aggregate for the group as a whole, should essentially be flat from the year-earlier level. That said, there will be variations among the players, with some like JPMorgan modestly up from the year-earlier level, and others like Citi modestly down.

Why the Downbeat Sentiment on Big Bank Stocks?

Given the cyclical orientation of the banking business, they remain vulnerable to the rising recession risks to the economy as a result of the Fed’s aggressive monetary tightening. We see this heightened risk in the unusual behavior of the treasury bond yield curve, with shorter-dated instruments that are more aligned with Fed policy yielding above longer-dated bonds.

I wouldn’t repeat why yield curve inversions are scary things and why it’s useful for all of us to keep a close on the risk of such a development. But I do want to point out here that I am sympathetic to the view that the current yield curve and its signaling power about future economic growth may not be fully comparable to historical periods as a result of the Fed’s extraordinary QE policies since the global financial crisis.

Irrespective of this plausible but otherwise minority view of the yield inversion, they are a net negative for growth outlook. This, coupled with elevated oil prices and the geopolitical uncertainty resulting from the Ukraine war appear to be weighing on bank stocks lately.

The market fears that JPMorgan and its peers will make a lot of money in the run-up to the start of the recession as a result of higher margins, but all of that will get offset by the inevitable deterioration in loan portfolios as recessionary forces take hold. That happens through ‘provisions for loan losses’ that banks will eventually need to book as recession becomes unavoidable.

The Covid recession turned out to be a non-event on the provisions front, as they ended up releasing the reserves that they had booked earlier. But that was because of the extraordinary fiscal support from the government.

The typical behavior in a recession is for the booked provisions to eventually get charged off (or written off), with the magnitude of the charge-offs a function of how bad or otherwise the recession is. The 2008 episode was particularly nasty in this respect, given how central housing was to that downturn.

The market has likely ‘over-learnt’ that lesson, as the banking group’s fundamentals remain rock solid at present, thanks in large part to the regulatory changes implemented in the wake of the 2008 recession. As such, we don’t see a lot of fundamental support for the excessively negative sentiment on big bank stocks at present, even if we assume a ‘typical’ recession on the horizon.

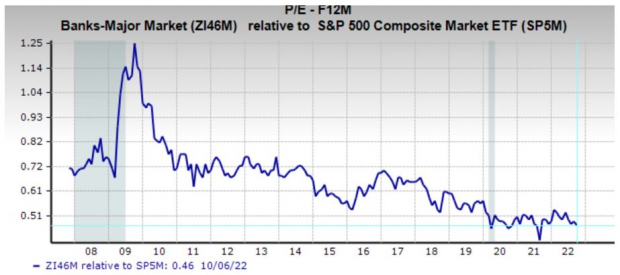

We see the bank stocks as attractively positioned currently on valuation grounds as well. The chart below shows the relative forward 12-month PE multiple for the Zacks Major Banks industry relative to the S&P 500 index.

Image Source: Zacks Investment Research

As you can see, the group is currently trading at 46% of the S&P 500 multiple, which compares to a 15-year high of 125%, low of 40% and median of 67%. Other valuation metrics validate this view as well.

What to Expect from the Q3 Earnings Season after the Nike & Micron Reports

We have been skeptical of extrapolating from FedEx’s (FDX - Free Report) downbeat quarterly numbers as we see a big part of FedEx's problems as company specific. But FedEx is hardly alone in pointing towards a cloudier horizon.

We don’t typically associate Nike (NKE - Free Report) with management and operational missteps, but we just heard them tell us of an inventory overhang that has negative implications for margins and profitability. Part of the +44% jump in Nike’s inventory is reportedly related to apparel whose movement through the company’s supply chain was affected by the logistical challenges.

We don’t know the details, but it’s fair to assume that some part of the inventory buildup is related to softening demand. After all, the U.S. Fed’s ongoing tightening cycle is directed at crimping aggregate demand as a way to bring down inflationary pressures.

Nike’s inventory problem validates what we heard from retailers in the Q2 reporting cycle. Chipmaker Micron (MU - Free Report) is faced with a comparable issue that forced it to cut guidance and slash capex to bring chip supplies in alignment with market demand that has come down as a result of weakening PC, tablet and smartphone sales.

We are starting to look at these early reports from FedEx, Nike, Micron and others for their fiscal periods ending in August as giving us a preview of what likely lies ahead as the banks kick-off the Q3 reporting cycle in about two weeks. For the record, we and other data vendors count these early reports as part of the Q3 earnings season.

Q3 Earnings Season Scorecard

The aforementioned JPMorgan and Citigroup results won’t be the first quarterly reports for the Q3 earnings season. In fact, we have already seen 20 S&P 500 members report results in recent days for their respective fiscal periods ending in August. We count all of these August-quarter results as part of our September-quarter tally.

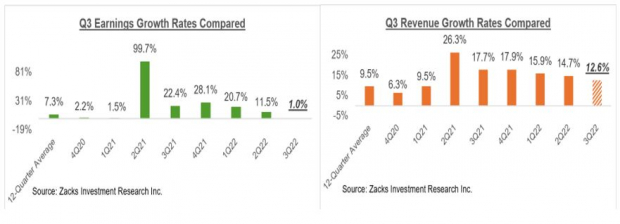

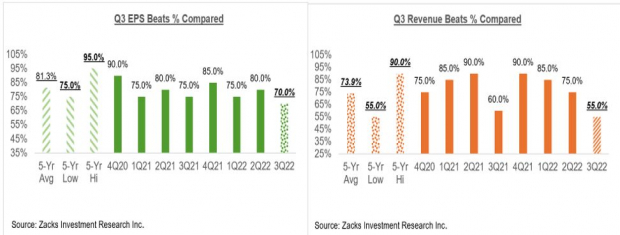

For the 20 index members that have reported results already, total earnings are up +1% from the same period last year on +12.6% higher revenues, with 70% beating EPS estimates and 55% beating revenue estimates.

Here is how the 2022 Q3 earnings and revenue growth rates for these 20 companies compares across different periods.

Image Source: Zacks Investment Research

Here is how the 2022 Q3 EPS and revenue beats percentages for these 20 companies compare across different periods.

Image Source: Zacks Investment Research

We are trying hard not to draw any conclusions here given how small the sample size of Q3 results is at this stage. But it’s hard to put a gloss on the fact that these 20 index members, some of whom are true bellwethers like FedEx and Nike, struggled to beat consensus estimates.

In fact, you can see above that the 2022 Q3 EPS and revenue beats percentages are tracking the 5-year lows for this group of companies. Needless to add that it is hardly a reassuring start to the Q3 reporting cycle.

The Earnings Big Picture

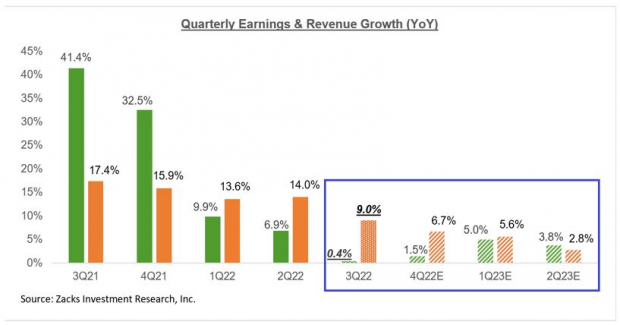

To get a sense of what is currently expected, take a look at the chart below that shows current earnings and revenue growth expectations for the S&P 500 index for 2022 Q3 and the following three quarters.

Image Source: Zacks Investment Research

As you can see here, 2022 Q3 earnings are expected to be up +0.4% on +9% higher revenues.

Don’t forget that it is the strong contribution from the Energy sector that is keeping the aggregate Q3 earnings growth in positive territory. Excluding the Energy sector, Q3 earnings for the rest of the S&P 500 index would be down -6.2% from the same period last year.

The chart below shows the comparable picture on an annual basis.

Image Source: Zacks Investment Research

The +6.7% earnings growth expected for the index this year drops to +0.1% once the Energy sector’s contribution is excluded.

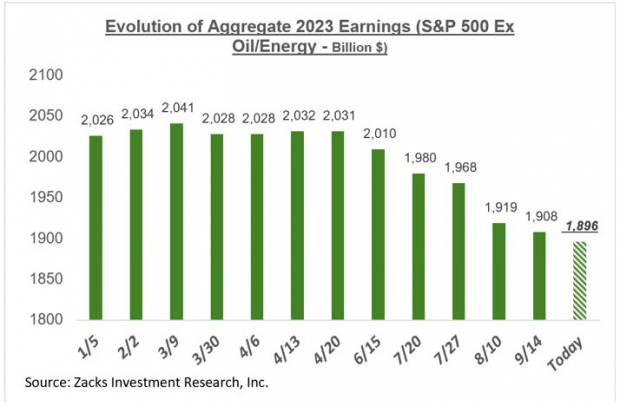

The chart below shows how the aggregate bottom-up earnings total for 2023 on an ex-Energy basis has evolved lately.

Image Source: Zacks Investment Research

More By This Author:

What Will Q3 Earnings Season Tell Wall Street?

Previewing Q3 Earnings Season After Rough Reports From Nike And Micron

Are Earnings Estimates Out Of Sync With The Economy?

Comments

Log in or sign up to join the conversation.