Image Source: Pixabay

Some pundits warn that, given extremely high stock valuations, one should sell everything. Yet, despite having the same information, other pundits show little concern and believe the bull market has further to run. The stark contradiction of opinions in today’s market leaves many investors understandably confused and anxious about what to do.

Based on valuations, there’s no denying we’re in a bubble. That’s noteworthy by itself, but it doesn’t tell us what will happen next. Tomorrow could be the day when valuations start returning to their historical norms. Or, valuations might become even more extreme, and the bull market could surpass all expectations before finally falling back to reality.

We believe that in this kind of environment, an active investment approach is preferable. Such an approach recognizes that as valuations increase, the risk/reward ratio worsens for investors, making adherence to technical analysis, risk tolerances, investment rules, and trading signals increasingly important. With this understanding of the growing risks, along with the potential for high short-term returns and the tools to navigate and limit downturns, we can continue to realize gains during strong bull markets and shift to a protective mode when a bear market begins.

We start by warning you about today’s high valuations. Then, we take a U-turn and explain why selling now might not be the best move.

Valuations In Perspective

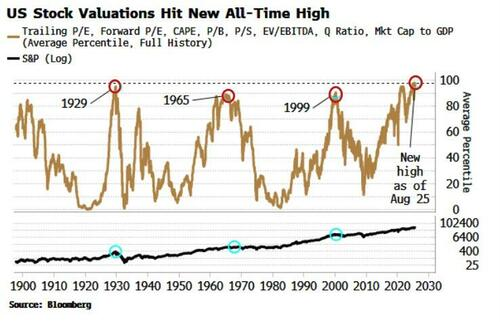

The first graph below shows that P/E and CAPE (P/E based on the last 10 years of earnings) are significantly higher than all other levels since 1950, except for 1999. They now match those from 2022. Although not shown, they are also well above the peak of 1929.

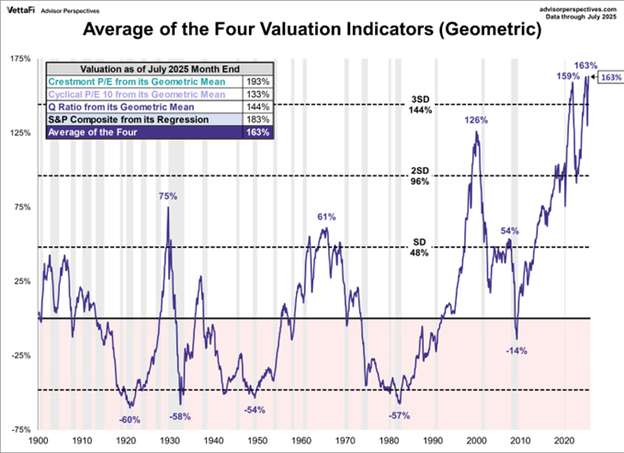

The following graph from our Bull/Bear Report shows that average valuations, as measured by an index of eight ratios, are at their highest level ever.

Slightly different from the previous graph, but the next graph delivers the same message.

66 of the 100 largest stocks by market cap (S&P 100) have P/Es over 30, and more than a quarter have a P/E over 50.

The Warren Buffett indicator, which measures the ratio of total market capitalization to GDP, is at an all-time high.

The equity risk premium is close to zero, meaning the reward for holding stocks over bonds is negligible.

After reviewing those graphs, it’s tempting to sell. The issue is that all the valuation metrics we use, along with many others, are unreliable trading tools. In the long term, high valuations often predict poor returns; however, in the short term, expensive valuations can become even more expensive.

Valuations Are Poor Timing Tools

In August 1997, the CAPE ratio reached 32.77, matching the previous record high set just before the Great Depression. While some experts at the time warned that the market would crash, as it did in 1929, the bull market largely ignored these fears. From August 1997 to the peak of the dot-com bubble in 2000, the market increased by more than 50%. Moreover, the extremely high CAPE ratio soared past the former peak to 44.

Those who exited the market in 1997 were ultimately rewarded in 2003 when the S&P 500 traded at a price below their selling point. However, an investor with a strong set of trading tools could have participated in most of the 50% increase, mitigated a good portion of the ensuing decline, and ended up well ahead of those who moved to cash early.

To demonstrate how a simple strategy might work, we use one of our trusted tools: the weekly 13- and 34-week moving averages. When the shorter-term average is above the longer-term average, the market is in a bullish trend. Conversely, it’s time to reduce risk when the shorter average drops below the longer-term average. The graph below shows the 1997 valuation record, market peak, and the activation of the sell signal.

From 1997 to the peak in 2000, our indicator issued three sell signals. As a result, reducing risk in late 1998 would have caused brief underperformance. The second signal, which appeared in late 1999, was short-lived and had minimal impact on overall performance. The third, and most significant, signal occurred after the S&P index dropped from 1,550 to 1,400. Holding onto stocks past the peak would have meant sacrificing some gains. However, the sell signal prevented much of the 50% decline. Despite the volatility in returns, this trading strategy would have outperformed staying in cash from 1997 to 2003.

Predicting Returns

Valuations serve as necessary wealth management tools when considering long-term perspectives. The graph below illustrates the monthly relationship between the CAPE ratio and the forward ten-year annualized returns. It demonstrates that, over ten-year periods, investors tend to benefit from purchasing at low valuations and face poor outcomes when buying at high valuations. As indicated by the red shading, the current CAPE suggests a bleak ten-year outlook, particularly since an investor can buy a risk-free 10-year Treasury note yielding over 4%.

While history suggests that total returns over the next ten years will likely be poor, it doesn’t reveal the path of those returns. Could the market decline by 60% in 2026, followed by a sustained bullish run for the remaining nine years, or might it rally for five more years before encountering turbulence?

The scatter plot below indicates that returns over the next six months are unpredictable, with no resemblance to those for the ten-year time frame. As we highlight, annualized returns from prior instances with similar valuations to today’s ranged from nearly -30% to +30%.

Summary

Records are meant to be broken, as they say. Just because valuations are reaching prior records doesn’t mean they won’t surpass them. They did in 1929 and 1999, and they may do it again soon. Conversely, given our current high valuations, we should expect poor future returns. This juxtaposition of statements leads us to take a cautious approach.

We understand both sides of the coin. While risks are increasing, there is a secondary risk for those not participating that markets could continue to steam ahead. Given the uncertainty, we prefer to stick with the trend. That doesn’t mean we are blindly buying the market. No, we are long the market and keeping a keen eye on our many indicators. We are able and willing to sell and reduce our risks when the time presents itself.

We will not call the top perfectly. And anyone who claims they can is lying. Our goal is to ride out the bull to and likely slightly past its peak, reduce our exposure, and remain underallocated to stocks until the market shows clear signs of a bottoming process. We do not know when the market will peak or how deep the correction will be. However, we are comforted that we have the right tools and rules to help us gain most of the upside and limit much of the downside.

More By This Author:

Momentum Strategies And Physics: Mass And Velocity Matter

UPS Is At Pandemic Lows: Value Or Value Trap?

The Index Isn’t Always Accurate: Factors Influencing Yields

Comments

Log in or sign up to join the conversation.