Price alone doesn’t always classify a stock as cheap but when solid growth is expected and valuation fundamentals indicate the equity is undervalued it’s usually time to buy.

Considering this scenario, here is a look at three top-rated Zacks stocks that are starting to come off as cheap.

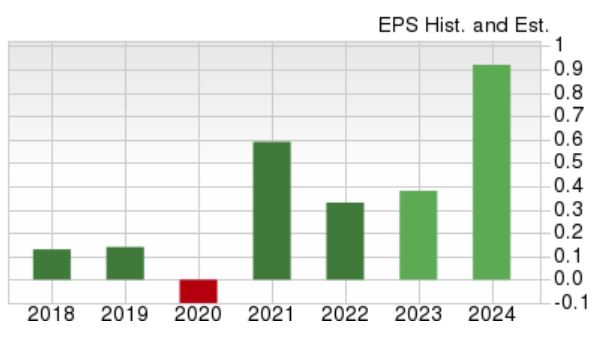

Harmony Gold (HMY)

Harmony Gold is starting to stand out with the gold mining company sporting a Zacks Rank #2 (Buy). Based in South Africa, Harmony Gold conducts underground and surface gold mining along with exploration, processing, smelting, and refining.

With Harmony stock trading at $4, earnings are forecasted to jump 15% this year and skyrocket another 142% in FY24 at $0.92 per share. The anticipated growth helps confirm Harmony stock is undervalued at 12X forward earnings which is well below its industry average of 21.5X and the S&P 500’s 20.6X.

Image Source: Zacks Investment Research

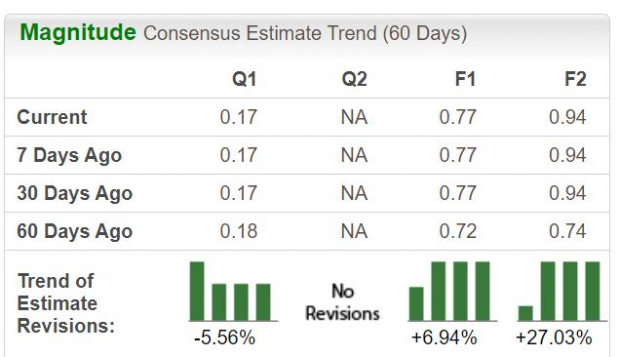

LSI Industries (LYTS)

Another stock that is starting to make the case for being cheap and undervalued is LSI Industries which also lands a Zacks Rank #2 (Buy).

LSI Industries is an image solutions company that combines integrated design, manufacturing, and technology to supply its own quality lighting fixtures and graphics elements for applications in the retail, specialty niche, and commercial markets.

Trading at $11 a share, LSI Industries’ earnings are forecasted to jump 20% this year at $0.77 per share compared to EPS of $0.64 in 2022. Plus, fiscal 2024 earnings are forecasted to climb another 20% to $0.94 per share.

Notably, earnings estimates are nicely up over the last 60 days for both FY23 and FY24 with LSI Industries stock trading reasonably at 15.5X forward earnings. This is near the industry average of 13.9X and nicely below the benchmark. Furthermore, LSI Industries price to sales valuation is very attractive with its P/S ratio of 0.69X beneath the industry average of 1X and the S&P 500’s 3.7X average.

Image Source: Zacks Investment Research

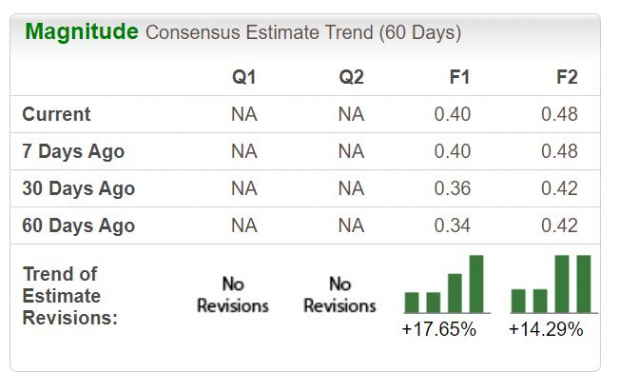

Marks and Spencer Group (MAKSY)

Lastly, higher earnings estimate revisions are making Marks and Spencer Group’s stock look attractive at $4 a share and coveting a Zacks Rank #2 (Buy).

Marks & Spencer is one of the U.K.’s leading retailers, offering premium clothing, home products, and higher-quality food. For its current fiscal 2024 earnings are now projected to dip -5% but rebound and soar 21% in FY25 at $0.48 per share.

Earnings estimates have gone up over the last 60 days with Marks & Spencer stock trading at 12.6X forward earnings which is slightly beneath the industry average of 12.9X and the benchmark.

Image Source: Zacks Investment Research

Bottom Line

Noticeable growth and rising earnings estimates are making these top-rated stocks stand out as cheap. This is supportive of their attractive valuations and is starting to make them look undervalued at their current levels.

More By This Author:

3 Intriguing Stocks To Buy For Value And Growth Potential3 Top-Ranked Stocks Investors Can Buy Now

Caterpillar Hikes Quarterly Dividend Payout By 8%

Comments

Log in or sign up to join the conversation.