Image Source: Pixabay

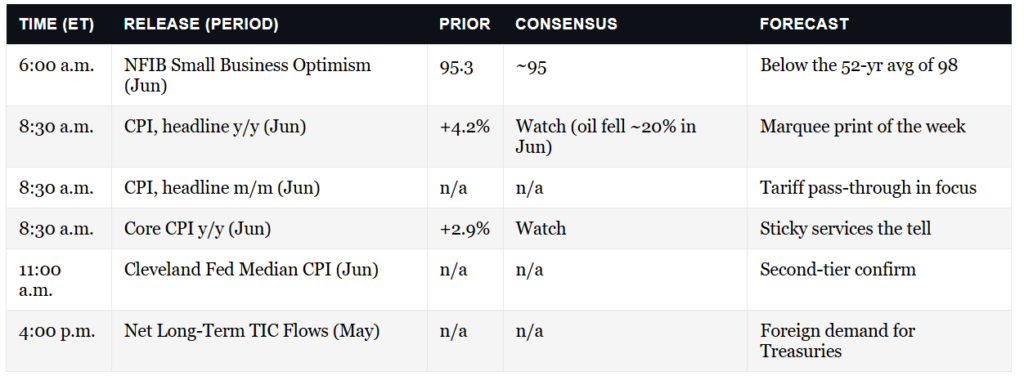

Typically, in Monday’s Commentaries, we share a few paragraphs titled “The Week Ahead’ in a lower section. This week, the amount and importance of the data could have a meaningful impact on markets and the Fed. Thus, this week’s’ “The Week Ahead’ gets top billing. Let’s review the calendar:

- Monday: There is little economic or earnings data to digest.

- Tuesday: JOLTs data will help us better gauge the breadth of the labor market. Earnings releases from V, PG, and UNH

- Wednesday: ADP data is the first look at June employment trends. This data set has been considerably weaker than the BLS. Following a decline of 33k jobs, Wall Street only expects a gain of 20k jobs this month. Second-quarter GDP is expected to increase by 2.5%, after declining by 0.5% in the first quarter. The FOMC will announce its rate decision. While the market expects no change, investors will closely watch for signs indicating whether a September rate cut is becoming more likely. Earnings from MSFT, META, and QCOM will be significant.

- Thursday: PCE prices, the Fed’s preferred inflation gauge, are expected to increase by 0.3%. AAPL, AMAN, MC, and ABBV headline earnings releases.

- Friday: The BLS report is expected to show a gain of 110,000 jobs, but a 0.1% increase in the unemployment rate. CVX and KMB release earnings.

Between this week’s labor and inflation data, corporate earnings, and new Fed guidance, the market has a lot of new information to digest. We should expect a healthy dose of volatility around many of the events we highlight.

What To Watch Today

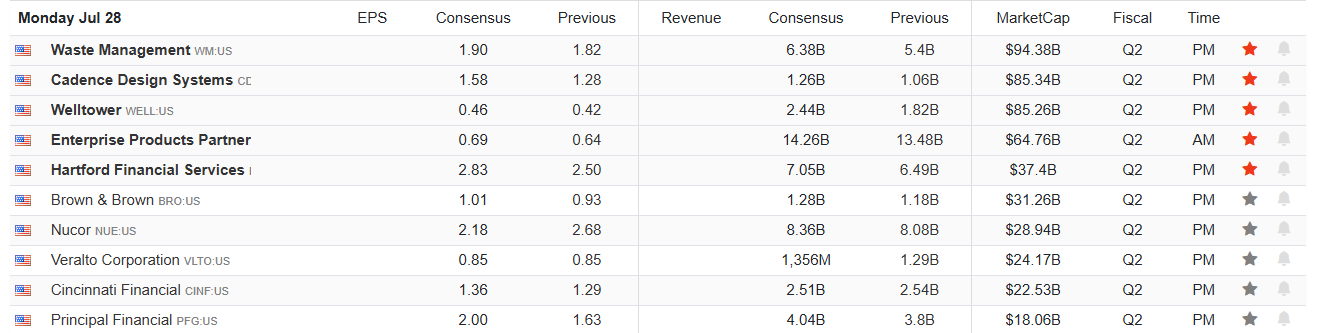

Earnings

(Click on image to enlarge)

Economy

(Click on image to enlarge)

![]()

Market Trading Update

The S&P 500 closed the week at 6,388.64, notching another fresh record high and extending one of the longest weekly winning streaks in the past three years. This persistent rally has been fueled by a potent combination of strong earnings from tech bellwethers, growing expectations of Fed rate cuts later this year, and an abundance of investor liquidity chasing momentum. So far, 87% of companies reporting through Thursday had beat expectations, primarily in Industrials, Financials, Healthcare, and Technology.

Bullish sentiment has been reinforced by a belief that inflation is finally cooling without significantly denting corporate profitability. Mega-cap tech and AI-related names remain key drivers, with earnings surprises and guidance upgrades boosting confidence. In addition, falling volatility, reflected in the VIX declining below 15, and record speculative activity in short-dated options (0DTE) suggest a market increasingly driven by sentiment rather than fundamentals.

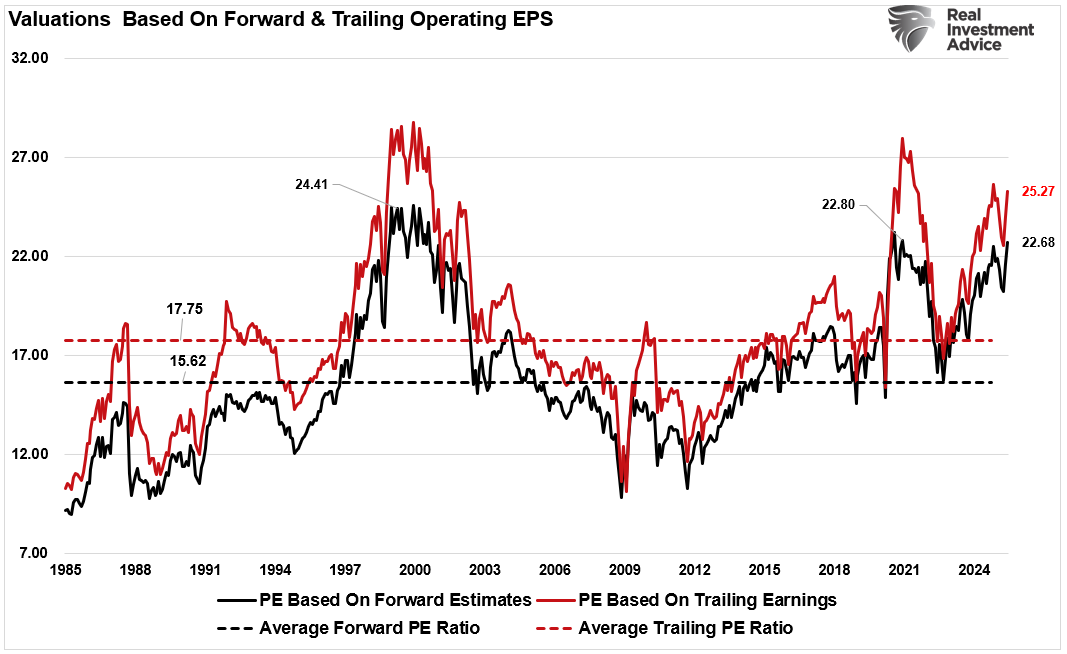

However, this surge in optimism comes with risks. Notably, valuations, while a terrible timing indicator, have surged to previous highs over the last month as prices are increasing faster than earnings. As is always the case, investors often overlook valuations, but valuations tell us much about sentiment and expectations.

Technical Backdrop

I reviewed some charts yesterday morning, and this one stood out. The ~20% correction in April was the seventh successful retest of the 36-month moving average since the Global Financial Crisis. Each of these tests, 2011, 2016, 2018, 2020, and 2022, has marked a critical turning point where the long-term bullish trend was defended. This consistent behavior suggests that the secular bull market remains intact, with long-term investors still stepping in during major pullbacks.

What’s particularly important is the context in which this retest occurred. April’s drawdown shook investor confidence amid concerns about inflation stickiness and a delayed Fed pivot. But despite macro headwinds, the market found strong technical support, and breadth improved modestly into the summer rally.

The monthly RSI has moved back into overbought territory, currently at 71.5. While not yet at levels that triggered prior major reversals, like in 2021 or early 2018, it does suggest limited upside without a pause or consolidation phase. Meanwhile, the MACD remains in bullish territory but is starting to flatten, indicating waning momentum. That doesn’t mean the bull market is over, but it suggests the ascent rate could slow, especially as sentiment gauges flash complacency and speculative trading (such as 0DTE options and meme stocks) picks up again.

This isn’t a timing tool. Monthly indicators move slowly, but the message is clear: the trend is still up, but risks are building under the surface. Think of it like driving your car. Everything is fine, but the gas gauge is nearing “E.” You can keep going, but you’d better have an exit plan mapped out.

Overall Risk Outlook: Risk levels remain elevated. While earnings and disinflation are supportive, stretched valuations and technical exhaustion argue for more defensive positioning in the short term.

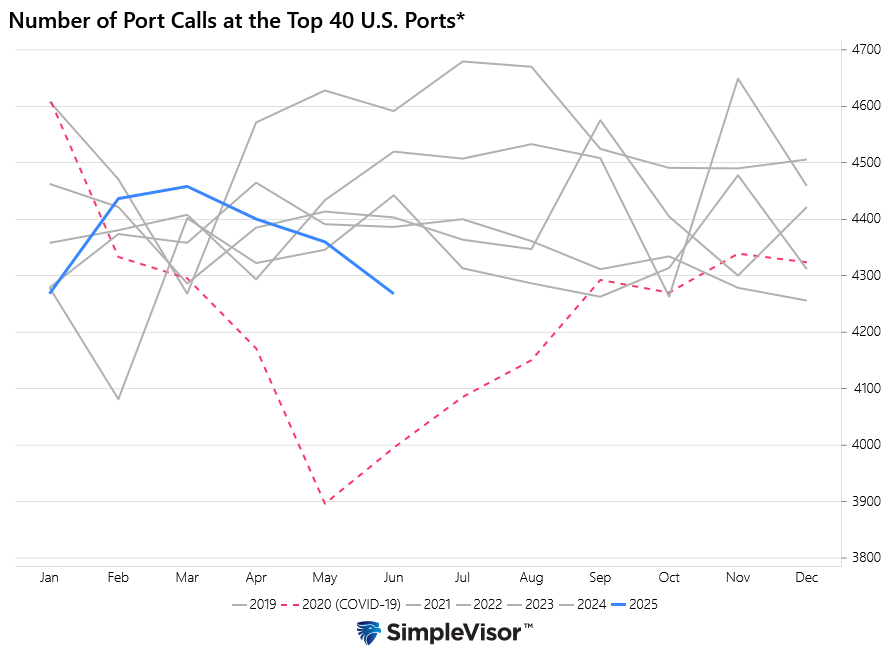

Port Traffic Slows: Tariffs Or Economy?

Imports into the top 40 US ports have slowed significantly over the past couple of months. To wit, June port calls are the lowest since Covid, as shown below. Furthermore, the number of port calls tends to increase in the Spring and into Summer. This year they have been declining.

This may allude to softer trade flows resulting from tariffs and shifting global supply chain patterns. Additionally, we might also question whether weaker consumption, as reflected in economic data, is a contributing factor. As tariff deals begin to materialize and trade normalizes, we can expect to see an increase in port calls. Moreover, the lull in imports likely means that companies have lower-than-normal inventories as we head into the holiday season. A pick-up in port calls could be sharp. Unless, of course, the economy is weaker than the current data allude to.

Is Private Equity A Wolf In Sheep’s Clothing?

In July 2007, just before the financial crisis erupted, Citigroup CEO Chuck Prince summed up Wall Street’s dangerous exuberance:

“When the music stops, in terms of liquidity, things will be complicated. But as long as the music is playing, you’ve got to get up and dance. We’re still dancing.”

Eighteen years later, Wall Street is dancing again, and the rhythm feels disturbingly familiar.

Private equity (PE), once a niche strategy reserved for sophisticated endowments and mega-pensions, is being aggressively marketed to everyday investors. It’s creeping into 401(k)s, target-date funds, and retirement accounts under the seductive promise of higher returns and diversification. But for investors who’ve forgotten history, or worse, were never taught it, the risks are mounting.

Tweet of the Day

More By This Author:

AI Is Powering MarketsThe Magnificent Seven Are Mediocre

Might Lower Rates Buy The Cure For Higher Prices?

Comments

Log in or sign up to join the conversation.