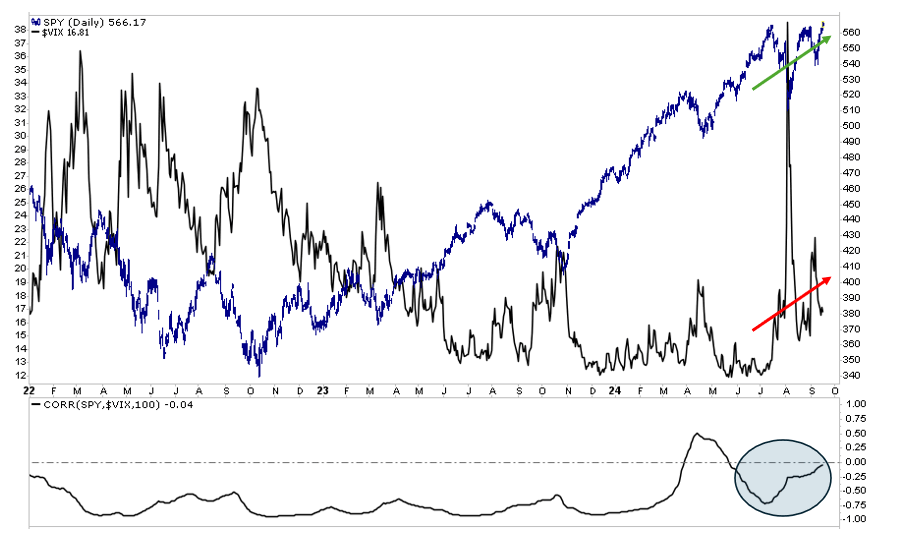

The VIX Index, often called the “fear gauge,” measures implied market volatility based on S&P 500 put and call options. Most often, the VIX rises when the stock market declines as investors tend to be willing to pay a higher premium for option hedges. Conversely, the VIX falls or hovers at very low levels as markets rise, and the aggregate market needs to hedge is minimal. However, there are times when the VIX Index rises alongside a rising stock market. This is occurring today, and it can be a sign that investors are suspicious of the viability of the recent stock market gains.

The current instance of an elevated VIX during alongside a record high suggests that investors are hedging more than is typical at market highs. Despite the positive momentum, investors are uneasy about the rally’s sustainability. Likely, the combination of the Fed starting to cut rates and the coming election are putting investors at unease. Furthermore, investors could be concerned that recent market gains are driven by short-term speculative trades rather than long-term fundamentals. Such a condition would leave the market vulnerable to corrections. The positive correlation between the VIX Index and the market should keep us alert for sudden changes in market conditions. Still, it doesn’t preclude the bull market from marching higher over the coming months.

(Click on image to enlarge)

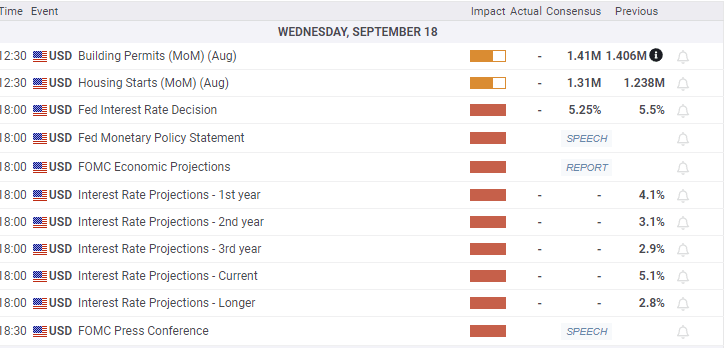

What To Watch Today

Earnings

Economy

(Click on image to enlarge)

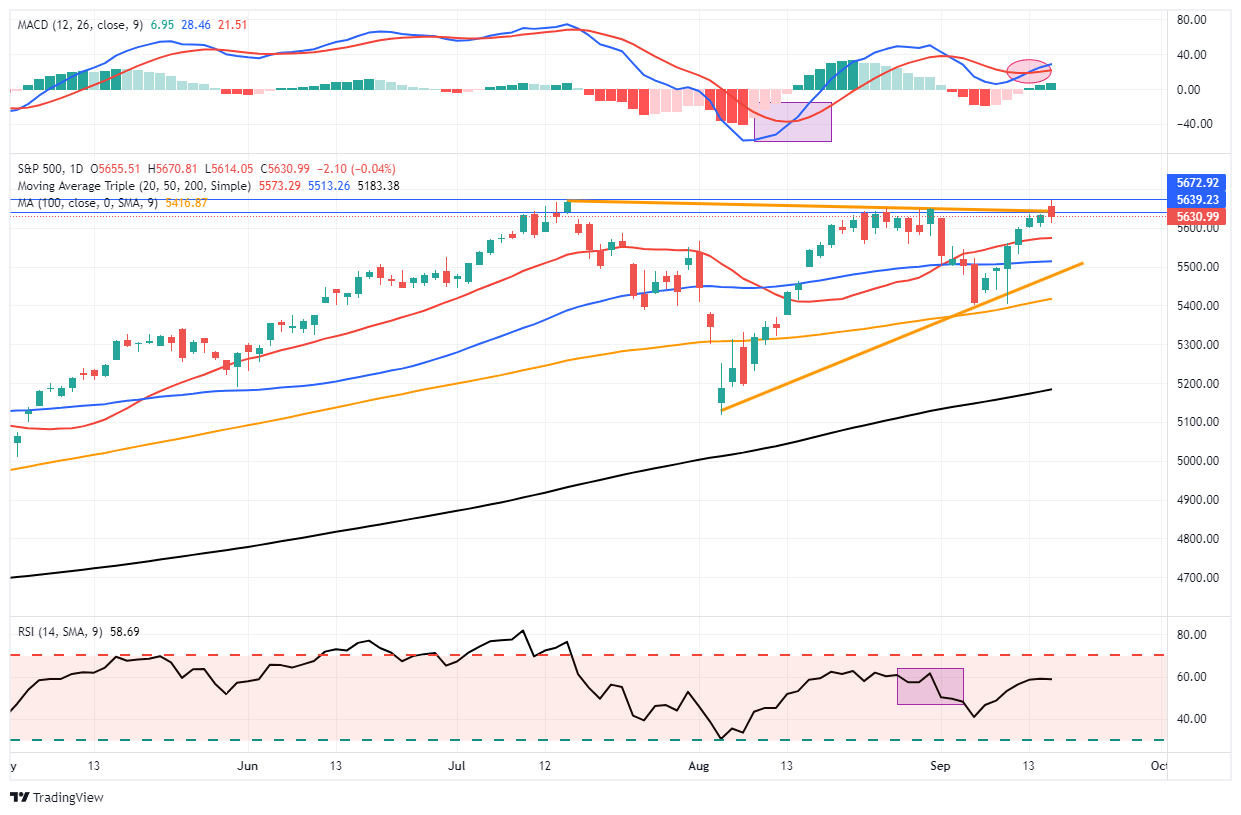

Market Trading Update

If you missed it, yesterday’s discussion focused on a question I have received several times about buying bonds. As I stated, short-term bonds are overbought heading into today’s Fed meeting, and a disappointment could lower bond prices. However, the same can be said for the equity market, which has also pushed into resistance at recent highs. As stated yesterday, the rally in stocks and bonds could be a “buy the rumor, sell the news” type event, so a bit of caution ahead of the Fed announcement is prudent.

As noted, the market is struggling with recent highs and is back in its previous consolidation range. From a bullish perspective, moving averages are trending higher, and the market is not egregiously overbought. With the market trading above the 20—and 50-day moving averages, the downside is somewhat limited. After today’s FOMC announcement, we should be better able to assess the next entry point to increase exposure. Furthermore, given the rather significant outperformance of defensive stocks as of late, a rotation to more cyclical growth stocks may be likely if the Fed signals lower rates are coming.

(Click on image to enlarge)

Regret Management

It’s easy to argue that the Fed should cut by 25bps, but the case for 50bps is more challenging. Given economic growth remains resilient and inflation is still 1%+ above the Fed’s inflation target, there is a reasonable case for lowering rates in 25bps increments. The risks of moving by 50bps are the market and political responses. Taking such a big first step may spark concern that the Fed is worried economic growth will slow rapidly. There is also politics the Fed must grapple with. Indeed, with any rate cut, but more so with 50bps, Donald Trump will blame the Fed for picking sides. If Trump wins, the Fed’s aggressiveness may move Trump to try to fire Powell. This potentially has big implications further down the road.

That said, Nick Timiraos, aka the Fed Whisperer, published a WSJ article Fed Prepares To Lower Rates, indicating the Fed could likely cut rates by 50bps this afternoon. The rationale appears to be regret management. Per the article:

If officials think about which mistake they are less likely to regret at this week’s meeting, the case for starting their rate-cutting cycle with a half-point move makes sense, said Robert Kaplan, who served as Dallas Fed president from 2015 to 2021.

“If I were in my old seat, I’d say, ‘I could live with 25, but I’d prefer 50,’ ” said Kaplan, now vice chairman at Goldman Sachs. Given where inflation and unemployment sit, the Fed’s benchmark rate should be about 1 percentage point lower than it is, he said. “If I started with a clean sheet of paper, I’d say rates should be at 4.5%-ish.”

The article raises an important consideration. The quarterly economic projections will be released at today’s meeting. The projections cover the rest of 2024, as well as 2025, 2026, and the “longer term.” Because only two meetings are left this year, the board’s Fed Funds projections for the remainder of 2024 will provide a road map for the market.

If more officials project a total of 1 percentage point of cuts this year, that would imply at least one move of 50 basis points this year. Withholding that larger cut until later this year could raise awkward questions over why that is the best approach. Another option is to cut by 25 basis points now and project cuts of a similar magnitude at the last two meetings of the year, reserving the option to accelerate the pace if the economy worsens.

Lastly, Timiraos brings up the possibility of a dissent from one or more Fed members. There has not been a dissent in two years. Per the article, that is the longest streak in the “past half century.”

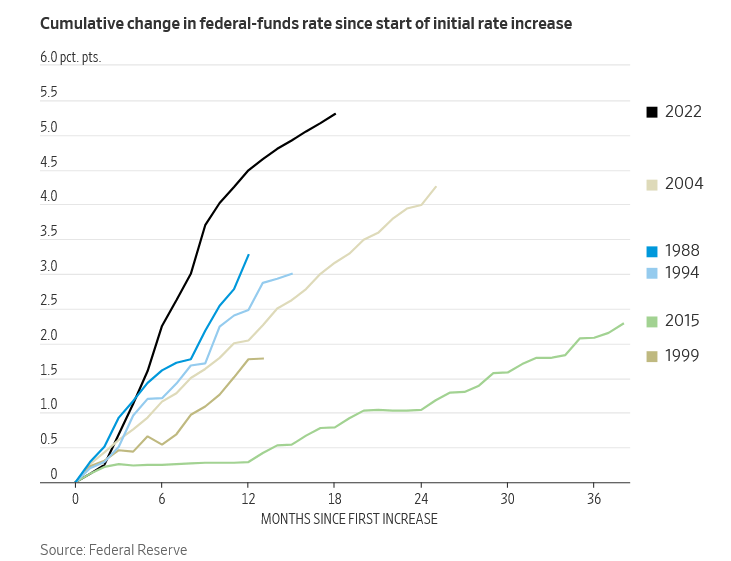

The graph below shows the rate increases of the past two years have been much more aggressive than the previous five rate-cutting cycles. Might aggressively removing said rate increase also involve an aggressive stance?

(Click on image to enlarge)

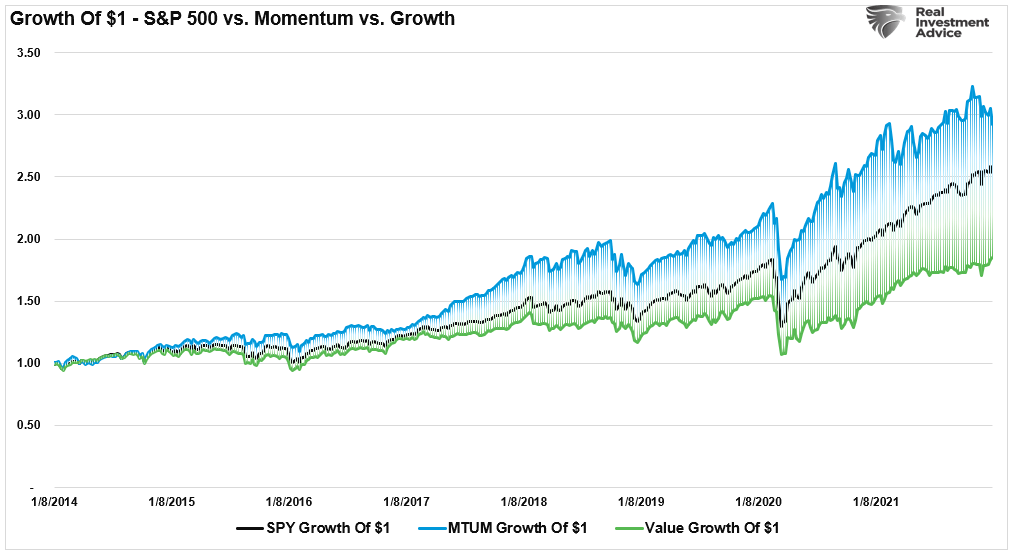

Momentum Investing Gives You An Edge, Until It Doesn’t

Do you buy a “momentum” fund and forget about it?

Well, not so fast, says Brett. However, while I agree with Brett, it is for a different reason. The issue with “Momentum investing” is that it is not a passive strategy. For example, if we look at the top 10 holdings of MTUM, we can see the changes being made to the ETF as momentum changes in the market.

(Click on image to enlarge)

Tweet of the Day

(Click on image to enlarge)

More By This Author:

Momentum Investing Gives You An Edge, Until It Doesn’t3 Market Risks We Are Watching Heading Into The Election

Labor Market Impact On The Stock Market

Comments

Log in or sign up to join the conversation.