Image Source: Pexels

Over the past decade, Tesla (TSLA) has grown from a niche electric vehicle startup into one of the world’s most valuable companies. It leads in EV innovation, energy storage, and AI-driven autonomy, and it’s now aiming for its most ambitious goal yet: building a $75 billion robotaxi network by 2030.

This could mark a major shift from car sales to a high margin, software-powered mobility platform.

But this isn’t just about replacing drivers, it’s redefining how transportation works. Tesla plans to use its existing fleet of vehicles, upgraded via software, to scale robotaxi services faster and more cost-effectively than competitors like Waymo or Zoox.

Paired with its new “unboxed” manufacturing system that could produce a car every five seconds, Tesla is laying the groundwork to make robotaxis its next major revenue stream. If successful, this move could transform Tesla from a car company into a platform business.

That said, there are hurdles. Tesla’s core automotive revenue fell 8% in 2024 and is expected to drop another 10% in FY25. While its energy division is growing rapidly, and projects like Optimus (humanoid robotics) could be game-changers, much of Tesla’s $1 trillion valuation is tied to future potential, not current profits.

Compounding this is CEO Elon Musk’s increasing political endeavours and his plans to form the ‘America Party’, which has already triggered brand backlash, policy risks, and even a potential $2 billion hit from lost EV tax credits.

Let’s have a deeper look at Tesla using the IDDA Framework: Capital, Intentional, Fundamentals, Sentimental, and Technical.

IDDA Point 1 & 2: Capital & Intentional

Before investing in Tesla, ask yourself:

Do you want to invest in the future of AI-powered mobility, energy, and robotics?

Do you believe Tesla can dominate not just EVs, but the robotaxi and autonomous vehicle market?

Are you comfortable with the risk that much of Tesla’s value is based on Elon Musk’s vision, not guaranteed execution?

Tesla isn’t just building cars, it’s building an ecosystem that connects AI, software, energy, and automation. Its robotaxi ambitions, vertical integration, and AI strategy give it enormous upside but only if it executes.

Still, there are real risks. Its valuation assumes near flawless delivery on future tech. Its automotive business is under pressure. And Musk’s political actions continue to trigger sharp price swings and brand damage. But for long term investors who believe in Tesla’s moonshot roadmap, the company offers both high risk and potentially high reward.

IDDA Point 3: Fundamentals

Tesla is undergoing a major transformation from a traditional EV manufacturer into an AI driven robotics and autonomy platform, with its long term growth centered around the rollout of a robotaxi network projected to generate $75 billion in revenue by FY2030. This shift comes amid declining automotive revenue, down 8% in 2024 and forecasted to drop another 10% in FY25, as competition in the EV space intensifies.

Tesla’s advantage lies in its ability to convert its existing vehicle fleet into robotaxis via software, making it far more capital-efficient than rivals like Waymo or Zoox. Paired with its new “unboxed” manufacturing system, which could produce a vehicle every five seconds, Tesla is building the scale needed to dominate this new space.

However, the company’s current fundamentals tell a more modest story: the core automotive business, while still the largest revenue contributor, is estimated to be worth just $70 billion based on premium multiples. The services division remains low-margin and underwhelming, while the fast growing energy segment, driven by AI-linked infrastructure demand, could be worth around $76 billion. Altogether, Tesla’s current operations support a valuation of around $186 billion, well below its $1 trillion market cap. The gap is filled by speculation on future technologies like robotaxis and humanoid robotics, which, while promising, are still in early stages and carry significant execution risk.

Musk’s leadership is now deeply intertwined with the stock’s performance, not just because of his vision, but also due to growing political endeavours. His involvement with Donald Trump, attacks on Democrats, and plans to launch a new political party called the “America Party” have created significant backlash.

These moves have led to real-world consequences: the potential loss of the $7,500 EV tax credit is estimated to cost Tesla around $2 billion in annual profit. Tesla’s own CFO has acknowledged increased vandalism and hostility toward the brand in some markets, with European sales already seeing sharp declines. Investor anxiety has grown, with analysts and firms flagging Musk’s political distractions as a risk to the company’s long-term stability. Ultimately, Tesla’s valuation today is less about its current numbers and more a high-stakes bet on its speculative future, and the polarizing figure leading it.

Fundamental Risk: Medium High

IDDA Point 4: Sentimental

Strengths

Robotaxi & Autonomy Potential – Tesla’s pivot toward autonomous vehicles and its plan to launch a robotaxi network by 2030 could open up a massive new high-margin, recurring revenue stream, potentially worth $75B annually. If successful, this could fundamentally reshape its business model.

Vertical Integration & Scale – Tesla’s in-house manufacturing, AI software (like FSD), and energy products position it as more than just a carmaker. Innovations like the “unboxed” manufacturing system and its global EV charging network give it cost and scalability advantages few competitors can match.

AI & Robotics Vision – Projects like Optimus (humanoid robots) and Tesla’s Dojo supercomputer could become future growth drivers. Investors bullish on AI and automation see Tesla as a long-term platform play, not just an auto company.

Risks

Valuation Disconnect – Based on current earnings and fundamentals, Tesla’s $1T+ market cap appears significantly overvalued. Its core operations only justify a valuation closer to approximately $186B, meaning much of its stock price is based on speculative future growth.

Key-Man Risk: Elon Musk – Musk’s unpredictable behavior and deepening political involvement have led to regulatory risks, brand damage, and stock volatility. The potential loss of EV tax credits could cost Tesla up to $2B annually, directly tied to his public actions.

Intensifying Competition & EV Saturation – Global competitors like BYD, Xiaomi, and legacy automakers are aggressively ramping up EV production, often at lower price points. With EV demand softening and Tesla’s market share slipping in regions like China and Europe, growth could be harder to sustain.

Tesla’s valuation is driven as much by belief in Elon Musk as by its business strategy. While future ventures like robotaxis and robotics could add massive value, Musk’s growing political involvement—clashing with Trump and launching the “America Party” has introduced new risks.

The potential loss of EV tax credits could cut $2 billion in annual profit, and brand damage is already hurting sales in key markets. As a result, Tesla’s stock now moves more with Musk’s actions than its actual performance.

Sentimental Risk: High

IDDA Point 5: Technical

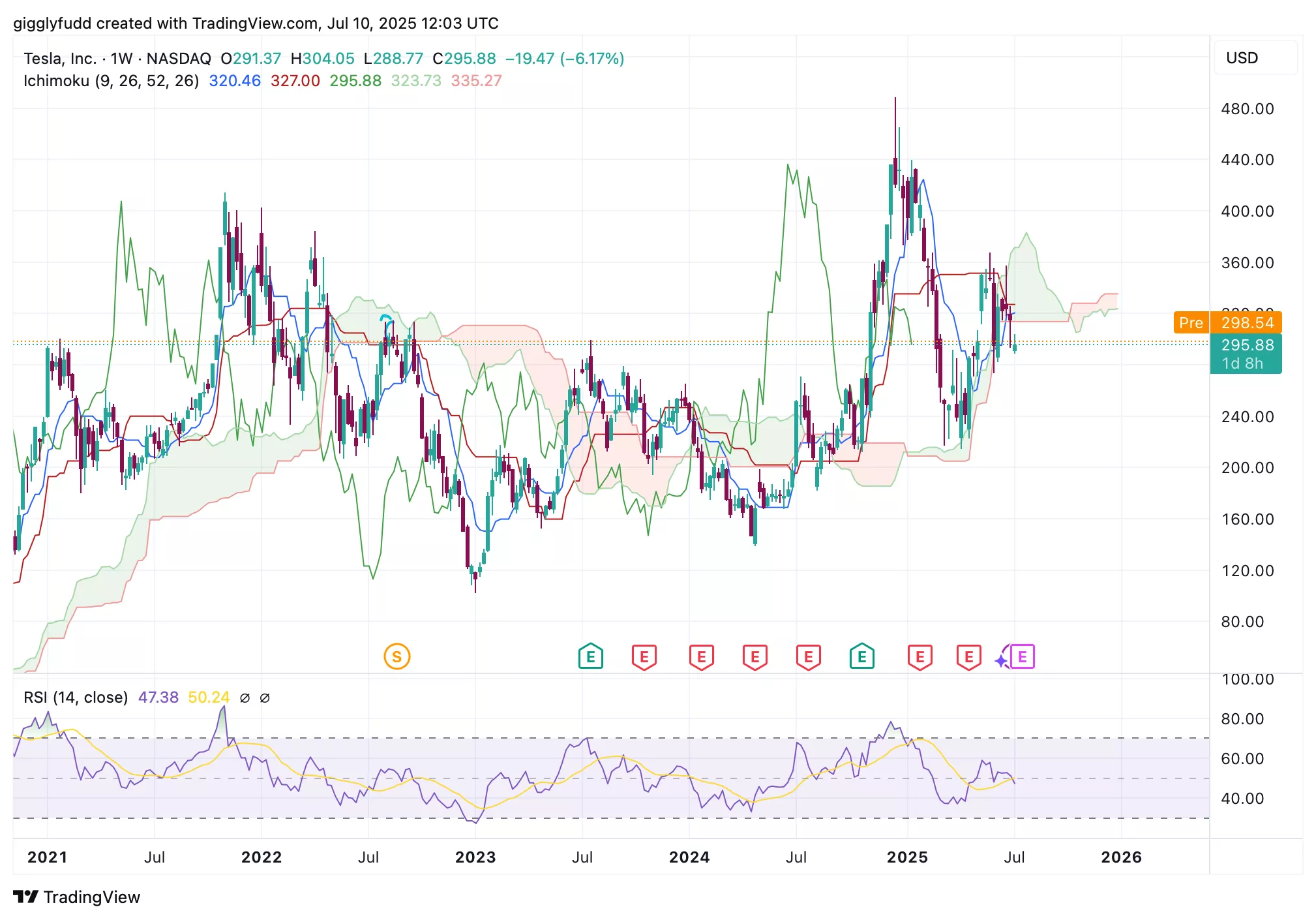

On the weekly chart:

The latest candlestick has closed below the Ichimoku cloud, signaling a bearish trend.

The future cloud is also bearish but remains flat and thin, indicating that the downward momentum may be limited or short-lived.

The Tenkan and Kijun lines are converging, suggesting potential indecision or a pause in trend direction.

Since 2021, the weekly chart shows that TSLA stock has experienced significant choppiness and volatility, dropping as low as 101 in January 2023. In 2024, it saw a strong uptrend, reaching a high of around $488 before undergoing a sharp pullback.

Currently it is showing early signs of bearish momentum, with the latest candlestick closing below the Ichimoku cloud, a key technical signal often interpreted as a shift toward a downtrend. However, the future cloud, while still bearish, appears flat and thin, which may indicate that any downside could be temporary or lacking strong conviction.

Additionally, the Tenkan and Kijun lines are drawing closer together, a sign of potential indecision in the market that could precede either a pause in momentum or a possible reversal if supported by future price action. If the Kijun line crosses over the Tenkan line to form a death cross, this is another bearish confirmation.

(Click on image to enlarge)

On the daily chart:

The Kijun line has crossed over the Tenkan line, forming a death cross, an early bearish signal.

The bullish cloud is thinning out, suggesting the bullish momentum may be short-lived.

Doji candlesticks have formed within the cloud, both signaling market uncertainty.

Possible formation of a descending triangle, indicating potential downward continuation.

On the daily chart, a bearish crossover has formed as the Kijun line crosses above the Tenkan line, often referred to as a “death cross”, an early signal of potential downside. While the cloud remains bullish, it is beginning to thin, suggesting that upward momentum may be weakening.

Within the cloud, Doji candlesticks have appeared, highlighting market indecision and uncertainty. Additionally, there are signs of a possible descending triangle pattern forming, which could indicate a continuation of the current downward trend if confirmed.

If the candlesticks break below the lower band of the Ichimoku cloud, currently acting as a support zone, it may signal further downward momentum.

(Click on image to enlarge)

Investors looking to take advantage of the volatility and get into TSLA can consider the following Buy Limit Entries:

Current market price 295.88 (High Risk – FOMO entry)

277.78 (High Risk)

221.38 (Medium Risk)

148.15 (Low Risk)

Investors looking to take profit can consider the following Sell Limit Levels:

409.04 (Short term)

490.04 (Medium term)

570.03 (Long term)

Here are the Invest Diva ‘Confidence Compass’ questions to ask yourself before buying at each level:

- If I buy at this price and the price drops by another 50%, how would I feel? Would I panic, or would I buy more to dollar-cost average at lower prices? (hint: this question also reveals your CONFIDENCE in the asset you’re planning to invest in).

- If I don’t buy at this price and the stock suddenly turns around and starts going up again, will I beat myself up for not having bought at this level?

Remember: Investing is personal, and what is right for me might not be right for you. Always do your own due diligence. You should ONLY invest based on your own risk tolerance and your timeframe for reaching your portfolio goals

Technical Risk: High

Final Thoughts on Tesla (TSLA)

Tesla (TSLA) stands out as one of the most closely watched and debated AI and robotics plays in 2025, for two key reasons that continue to drive both market sentiment and volatility.

First, its bold pivot toward autonomy, particularly the launch of its robotaxi network, could generate up to $75 billion in revenue by FY2030. With software updates enabling existing vehicles to become autonomous, and a new “unboxed” manufacturing system targeting mass robotaxi production, Tesla is positioning itself to lead a future defined by AI powered transportation.

Second, Tesla is more than a car company, it’s a vertically integrated platform that spans energy, software, and robotics. Its energy segment is growing rapidly, and new projects like the Optimus humanoid robot hint at additional revenue streams that could redefine its long term valuation.

However, Tesla’s journey is far from smooth. Its fundamentals support a much lower valuation than its current $1T+ market cap, and the stock is heavily influenced by CEO Elon Musk’s political moves. His involvement in U.S. politics has already triggered policy risks and brand backlash, including the potential loss of EV tax credits worth $2 billion annually.

This makes Tesla a stock driven as much by sentiment and speculation as it is by revenue and execution.

Recommendation: Hold / High Risk – High Reward, ‘Speculative’ Growth Play

Tesla is best suited for investors who believe in its long-term vision of autonomous mobility and AI driven innovation and who are comfortable riding out short-term political and market volatility.

Overall Stock Risk: High

More By This Author:

2 Big Reasons Why Atlassian Could Be A Top AI Stock In 2025 That Investors Can’t Ignore

Amazon Stock Bold Yet Quiet Robotics Expansion: Why Investors Should Pay Attention Now

BigBear.ai Stock: Missed Palantir? This Might Be Your Second Shot

Comments

Log in or sign up to join the conversation.