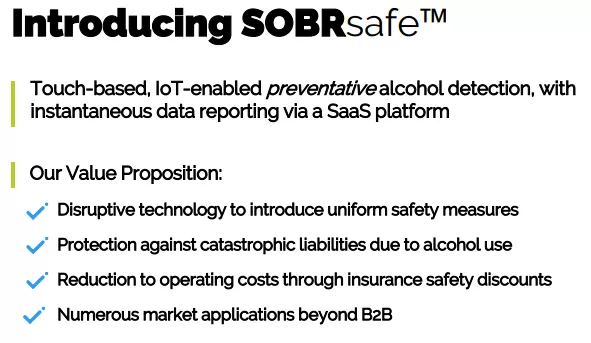

SOBRSafe (SOBR) is an early revenue company that brings a new solution to the market that has the potential to revolutionize the alcohol detection business.

They couple the non-invasive ease of use of the product with an innovative SaaS business model that produces high-margin recurring revenues, rather than one-time device sales, from the November 2022 IR presentation:

After a 3:1 reverse split and a $10 million offering of 2.35 million shares at $4.25 the company’s shares began trading on the Nasdaq under the ticker SOBR in May 2022.

The shares have not done so well recently as financing companies that provided much of the capital recently are converting their warrants en-masse and selling the shares.

They must have been preparing for this as the company’s shares were increasingly shorted in the last couple of months. This isn’t terribly surprising as these financing funds are simply moving to the next deal, this isn’t exactly patient capital.

While it is unnerving for existing shareholders, this has little to do with the company fundamentals and we believe it provides an excellent opportunity to establish a position.

The Product

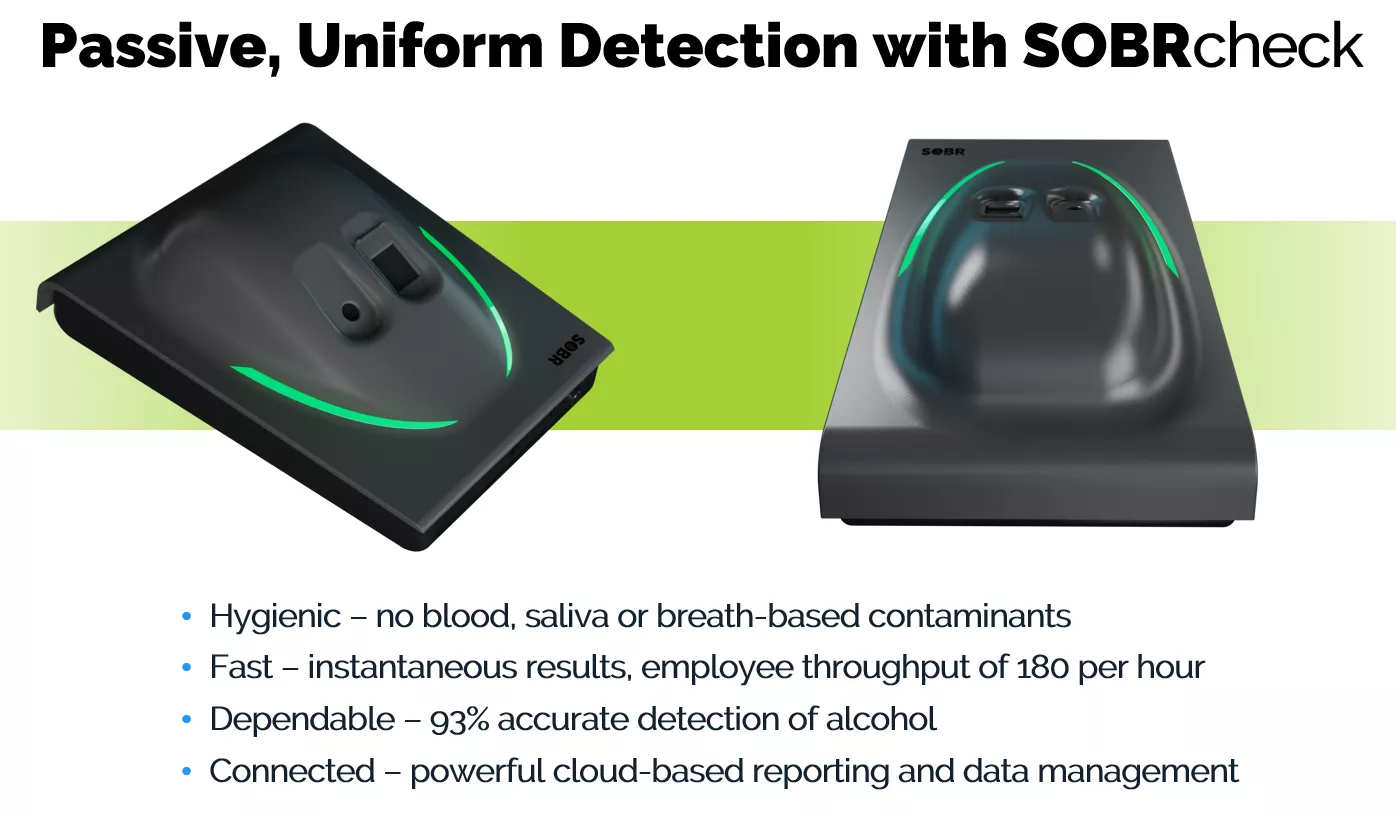

The company has two versions of its alcohol detection products, here is the main one, SOBRcheck:

The SOBRcheck enables a rapid, hygienic biometric finger scan to authenticate ID and determine the presence or absence of alcohol, and here is the idea for its use (Registration Statement):

The SOBRcheck™ product will provide the employer with real-time results, delivered securely, to more efficiently manage their existing substance abuse policy. Our device is meant to be a specific point in time, quick test for the presence of alcohol, with the results to be used as a complementary data source in support of the employer’s alcohol policies… We will gather de-identified information regarding Pass/Fail tests for use in determining trends in a company and/or industry, etc. but such information does not include any specific data about the individual user, only whether a pass or fail result occurred.

The SOBRcheck operates with two sensors: a fingerprint scanner ascertains the user’s ID and another sensor is capable of detecting alcohol released through the pores of the fingertip.

It doesn’t tell the level of alcohol in the blood (if necessary, additional - breath, blood-based - tests should be conducted). The company is already selling the SOBRcheck and has customer agreements in place per Q1/22 (see below).

In September 2022 the company introduced a second product with partner North-Star Care, the SOBRsure:

The products are made by BGM:

BGM will execute all supply chain functions, including design, engineering, component sourcing, manufacturing and testing for SOBRsafe’s Made in America safety devices.

The Business Model

The company’s business model has two components:

- A one-time installation fee of $500 per device for the SOBRcheck and a one-time device purchase price of $450 for the SOBRsure.

- A recurring monthly SaaS fee per user of $30 for both the SOBRcheck and the SOBRsure wristband.

Management also intends to monetize its anonymized data, which is an interesting opportunity in itself (Registration Statement):

The opportunity to collect millions of data points over time could enable the development of business and insurance liability benchmarking, and through AI, powerful guidance for perpetual safety improvement (and associated cost savings capture). By demonstrating substance-free environments, employers could deliver a data-driven argument for lowering insurance premiums. We could potentially partner with insurance providers to mandate use of the SOBRsafe™ devices and/or technology.

The SaaS Platform

From the Registration Statement:

These technologies will be integrated within our robust and scalable data platform, producing statistical and measurable user and business data.

The platform automatically notifies the relevant people and the data can be used for stuff like risk calculations which can lower insurance premiums.

The Market

It won’t come as a surprise to anyone that alcohol abuse comes with a very large bill (Registration Statement):

Through criminal-justice related costs, lost work productivity and healthcare expenses, the annual cost of alcohol abuse in the U.S. is estimated to be $249 billion. Half of all industrial accidents involve alcohol, and commercial fleets suffer from over 11,000 alcohol-related accidents each year.

The company is geared at prevention, rather than punishment after the fact and there are numerous segments where that approach is likely to add significant value.

So the company offers a touch-based alcohol detector that scans the person’s ID as well as detects any alcohol in the blood in one go, which should be ideal as a preventative workplace safety tool:

Then there are other applications such as the justice system and patient rehabilitation. Workplace and fleet seem by far the biggest opportunity though.

Progress

The company has a multi-pronged marketing approach:

- Third part administrators (TPAs)

- Distributors

- Direct sales

- Popular and trade media public relations

- Advocacy group alignment

- Dynamic social media brand development

SOBRsafe already has customer adoption and is in revenue, with 5 customers and 6 distributors across its core markets Justice, Rehabilitation and Fleet & Workplace.

The company is also in pursuit of cutting-edge detection technologies for future integration, which would enable it to leverage its SaaS platform and part of its existing client base.

And the details are in the PRs:

- Advance Freight Traffic Services (May/22) */**

- Distribution agreement with Recovery Trek (June/22)**

- Insurer partnership for customer pilots in fleets (June/22)**

- Continental Services for fleet (July/22)*

- Aaron Contracting for construction (July/22)*

- North-Star Care for alcohol rehab treatment (July/22) *

- RubiRides for ridesharing (Aug/22) *

- Reconnect distribution deal for the justice market (Aug/22) **

- Butterfield Onsite Drug Testing (Aug/22) *

- Alternatives for the corrections and re-entry systems (Sept/22) *

- AWB Compliance Services for the air, rail and shipping industries (Oct/22) */**

- TerraTech demonstrations for the oil&gas industry (Nov/22) **

- CSN for school bus drivers (Nov/22) **

The ones marked with * are customers, those with ** are distributors.

The initial focus is on the commercial vehicle fleet segment, which is timely as the National Transportation Safety Board (NTSB) recently highlighted the need for technology solutions to eliminate impaired driving.

The Advance Freight Traffic Service agreement offers services to that segment and will introduce the company’s tech to its extensive client base (as well as having installed the SOBRsafe in its own headquarters). Here is what Advance Freight President Jeff Bogden said:

I have been working with logistics industry thought leaders for nearly four decades, and I believe that the SOBRsafe™ technology could be one of the most important developments for fleet safety in recent memory. Based on the success of our pilot test, we now intend to recommend SOBRsafe to top freight executives and our own customer base of substantial employers.”

The insurer partnership and deal with Continental Services are also directed at the fleet segment.

The deal with CSN which will promote their solutions for the roughly 500,000 school buses in the US could also produce results as CSN is endorsing SOBRsafe as the featured solution for November's National Child Safety & Protection Month.

SOBRcheck seems a pretty obvious choice for work situations where alcohol use would pose major risks, like aviation, fleets, atomic energy, construction, and the like.

And indeed, the company made a presentation for another obvious candidate, the nuclear energy sector. TerraTech, one of the world's largest oilfield services and logistics providers is going to demonstrate the product in multiple venues for the oil & gas sector which has the highest rate of binge drinking of any industry in the US.

Because that alcohol takes significant time to metabolize (roughly an hour per ounce, that is, per drink), binge drinking is a silent problem causing significant problems the next day.

The SOBRsafe will flash excessive use, not one or two drinks the next morning and this could even lead to behavioral changes which create wider benefits.

Then there is the construction industry is another segment where alcohol-related accidents are a significant problem and the company has produced a solution tailored for this segment, from the Aaron Contracting PR:

Aaron represents SOBRsafe’s launch into the potential $2.7 billion construction market, one enduring the highest adjusted heavy alcohol use rate and challenged by its outdoor workplaces and lack of internet connectivity. To overcome these challenges, SOBRsafe has engineered a field version of its SOBRcheck™ solution, complete with battery power, Bluetooth capabilities, rugged casing and a mobile shelter to protect against the elements. The solution was recently proven successful in an external environment test with an Amazon Delivery Service Partner vehicle fleet.

The company now also has six reseller deals for the judicial system, which include Reconnect, Recovery Trek, and Butterfield. This is an interesting segment, for instance, there are some 2 million people under probation-mandated alcohol testing in the US alone.

Then there is the rehab segment where the SOBRsure wristband could be especially useful and they signed a deal with Alternatives, a leader in innovative corrections and re-entry strategies with 7,000 clients.

The company was awarded the Occupational Health & Safety (OH&S) new safety of the year product and that wasn’t the only award:

Given that its prime use is to reduce risk in workplaces where alcohol would pose a major risk, a natural partner is the insurance industry:

Lowering the risk by screening out alcohol abuse creates a return that can be shared three ways, a triple-win for the company, insurers as well as clients. The latter is likely to benefit in terms of lower risks as well as lower insurance premiums, and this is a strong incentive for adoption.

Indeed, the above-linked agreement with a Top 100 Property & Casualty insurance company involves two pilot tests with last-mile fleet customers, as paid for by the insurer.

We shouldn’t forget that the company offers a much simpler solution compared to others:

And automatically saving anonymized results to the cloud will help insurers precise risk change assessments. The SOBRsure wristband has additional use cases, like:

Financials

June is the last available quarter with regards to figures and the company was just starting, with the SOBRsure not even having launched yet, from the Q3 10-Q:

Revenues were still negligible but the $2.7M OpEx is a good indication of cash burn, which we expect to be somewhat lower due to share-based compensation ($329K in Q3) and exercising warrants.

For the first 9 months of the year, the operational cash burn was $4.26M but $2.7M for the first 6 months so the cash burn is now $1.5M+ a quarter.

This is likely to gradually increase as they build out their sales force, but on the other hand, revenue will also increase and the $10M or so in cash should last at least to the end of next year, and that is before the up to $16M the company will receive from warrant conversion (see below).

Selling Financiers

From the prospectus:

The second column is what they could sell if they convert all the convertible warrants as of Monday into shares. This looks scary, but realize:

- There is NO dilution, these are existing shares and (mostly) warrants.

- If all these warrants are exercised the company gets up to another $16 million in cash, more than doubling its runway until it generates its own cash flow.

So while the shares are likely to remain volatile for quite some time these selling financiers have little regard for fundamentals. We think the keen investor can take advantage here.

Valuation

This should include the $6 million raise in September. At $1.3 per share, that’s a $40 million market cap. For a back-of-the-envelope calculation, at $360 per year per subscriber, that takes 111,000 subscribers to produce a $40 million run rate but one can assume that, depending on the speed of the ramp, the company would be able to command a considerably higher sales multiple.

And one could argue that SaaS companies with strong growth and 80%+ margins wouldn’t typically sell at 1x revenues, so at 5x revenues, it would only take 22,200,000 subscribers.

Of course, the company isn’t yet producing meaningful revenues nor 80% gross margins, but in a few quarters when the deals ramp it’s likely to be a different picture.

With another $16 million in cash from the warrants, the company would have $25 million+ in cash, well over half its market cap. This also greatly extends the runway they have until cash flow is positive to at least the end of next year even if OpEx increases to $4 million a quarter (it’s $2.7 million in Q3).

And it doesn’t take all that much for the company to become profitable. For instance, 30K subscribers would provide $10.8 million in revenue or at least $8.6 million in gross profit, which should cover OpEx even if it rises by 50% from present levels. This should be more than enough to produce positive operating cash flow.

Conclusion

There is obviously a huge market for the company’s products and the SaaS model makes it enticing for investors as well. While the $60 million or so market cap stands in no relation to revenues, the company has cash that could last them 2 years or more, and that gives them a pretty long runway to scale revenues.

We estimate that at just 30,000 subscribers the company could be cash flow positive already and we see that as a pretty soft target for next year. It could be way better than that.

While it’s difficult to get a feel for any kind of hockey stick development in subscriber growth with little concrete sales data to go on, given the amount of interest they’ve received, the usefulness of the product, and deals already closed, this could ramp quite a bit faster than that.

So while there is always a considerable risk for a new product where sales have yet to take off, they have at least two years to get to cash flow positive, and 25,000 subscribers.

Risk apart, the potential rewards are rather big when you realize that 100,000 or even 1 million subscribers are also eminently possible longer term. So we see this as a very favorable risk/reward play.

While the present selloff is scary and volatility is likely to continue, we think under $2.00 per share provides a nice opportunity as we don’t believe the selling is related to fundamentals.

More By This Author:

A Paradigm Shift In Healthcare Produces A Big Market Opportunity

A Ground Floor Opportunity in Splash Beverage

Bion Environmental Technologies Turns Waste Into Marketable Products

Comments

Log in or sign up to join the conversation.