Summary

- Chevron is a well-positioned, well-managed behemoth in the energy world.

- BP and Royal Dutch Shell also are right up there, as is Exxon Mobil.

- But for the best-managed, most forward-leaning and most responsible energy player, Total is No. 1.

I think Total (TOT) - pronounced "Toe-TALL," it's a French company - is the best-managed super-major oil company in the world, with the most complete plan to reinvent itself as not just a fossil fuel, but also a renewable energy, company of size. Yes, better than Exxon Mobil (NYSE:XOM) or even Chevron (NYSE:CVX).

With 100,000 employees and activities in more than 130 countries, Total, headquartered in Paris (France, not Texas), this nearly 100-year-old company is today the fourth-largest energy firm in the world, with more than $200 billion in annual revenue. They became a super major back in 1999 when they merged with two fiery competitors, Elf Aquitaine of France and Petrofina of Belgium.

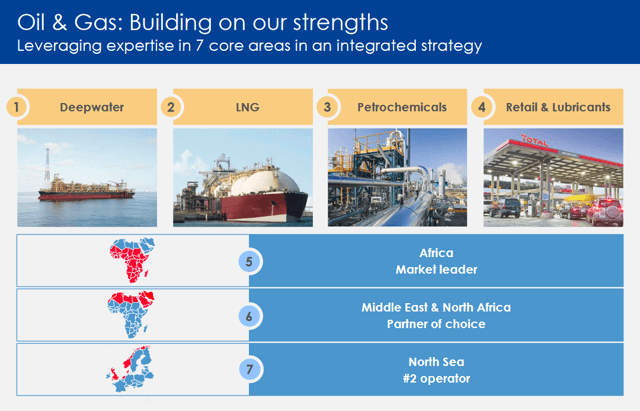

Total has resources around the world. If one region suffers some sort of civil unrest or geologic difficulty, another region simply picks up the slack. With exploration and production, midstream, refining and downstream distribution outlets, no one area’s weakness will pull the company down. Total is no one-trick pony.

The energy sector is particularly cyclical. Understanding those cycles, both short term and long, is the key to making money as an investor in this sector. The first time I bought Total was during the dotcom dotbomb. When everyone else was buying junk at hope x greed x infinity, the oil patch was a bargain.

TOT is of course subject to that cyclicality as well. However, in the last down cycle for energy that ended with a huge number of firms cutting dividends, showing losses or even going out of business, Total's earnings fell just more than 50% in the worst year (2016). It's important to note that both Chevron and BP (NYSE:BP) declared an actual loss that year.

Total's diversified portfolio of exploration and production, midstream assets, refining, and consumer operations has kept its earnings stream robust. When one area is weak, others still provide cash flow. I'm looking for 8%-10% growth this year and I expect I will see continued growth going forward as Total has diversified its portfolio even further by engaging in some serious renewable infrastructure.

SOURCE: TOTAL Sept 2019

You may recall that the price Occidental (OXY) paid for acquiring Anadarko was that Anadarko had to liquidate its assets in Africa. Total was right there, snapping up those property leases. France, and Total in particular, has had great success in Africa, with Total's deep-water drilling offshore Ghana as well as their LNG production in Mozambique. I personally believe if a company can navigate the different cultures and governments, Africa's vast resources will provide the fuel (not just for energy, but resource and intellectual capital as well) for future world progress. Because about 90% of TOT's natural gas production is outside the US, the current US glut in natural gas does not affect Total.

Recent earnings make this clear. Total reported fourth quarter 2019 operating earnings of $1.19 per share, handily beating the consensus estimate of $1.01 by 17.8%. This out-performance mostly came from a rise in production volumes, even in a time of softness in the prices of their products.

Cash and cash equivalents as of Dec 31, 2019, were $27.4 billion compared with $27.9 billion at the end of 2018. Net debt-to-capital was 20.7% at the end of the quarter. Total, unlike many (most?) firms that buy back shares at historic highs, took advantage of stock price weakness to repurchase shares worth $1.75 billion in 2019 and projects it will buy back $2 billion shares in 2020.

Yet, even with such steady and stellar performance in the real world, Total’s stock is currently selling within pennies of its low for the past 52 weeks. Free cash flow should be around $4 billion this year and I expect it to improve even more in 2021 and beyond. During the last five years, Total has increased its dividend 1 times on a year-over-year basis for an average annual increase of 1.44%. Total's current payout ratio is 54%. This means it paid out 54% of its trailing 12-month EPS as a dividend.

The company is currently getting about a 50% higher price for natural gas production than other US firms. How can this be? All we read is how natural gas prices are in the cellar. Ah, yes, in the US they are. We have a glut of natural gas in this nation. But around the world, the thirst for natural gas is higher than the amount that can be produced locally or within a near enough place to make the cost of transmission reasonable. Elsewhere in the world, where Total shines, gas prices are considerably higher.

SORCE: TOTAL Sept 2019

In addition to all its traditional energy capabilities, one of Total’s subsidiaries is Total Quadran. Formed in 2013, Total Quadran's provides renewable energy in the form of wind, solar, biomass, and hydropower. Total Quadran runs 11 wind farms and 35 solar plants. Total, including Quadran as well as the rest of its subsidiaries, operates 300 renewable energy plants in France. This company is clearly committed to growing its renewable energy business. Their most recent purchase in this was the Adani Group's solar portfolio for $510 million. Total is aiming for its renewable energy sector to account for 15% to 20% of sales by 2040.

Every bit as important as a company’s numbers is its commitment to employees. Employees of Total collectively own 5.3% of the company today. In addition, the company issues shares specifically for employees, allowing them to buy at a 20% discount to the market price.

While you and I cannot take part in that employee-only good deal, we too can buy shares at a 20% discount. The stock is down 20% over the past 52 weeks. At this price, the stock sells for a PE of less than 12 and yields just a shade over 6%.

I am buying Total for the long haul.

Good investing.

Comments

Log in or sign up to join the conversation.