It’s the end of an era and the beginning of a new. When evaluating performance within PE, roughly two-thirds of the total return for buyout deals that were entered in 2010 or later and exited in 2021 or before can be attributed to market multiple expansion and leverage.[1]

Today, with higher financing costs, falling multiples, and a tighter exit environment, fundamental value creation through revenue growth and margin expansion are taking center stage for GPs. We encourage investors to go where fundamental value creation has been the largest driver of returns. The US Middle Market.

Private middle market: the engine of the U.S. economy

The U.S. middle market, comprised of 200,000 companies with annual revenue between $10M-$1B, has served as a driving force of the domestic economy for decades, representing one-third of private sector GDP and employing 48 million Americans.[2] The middle market has thrived in the post-pandemic era with 83% of middle market firms reporting positive year-over-year revenue growth in 2023 – the highest reading on record – alongside strong employment gains.2

Capitalizing on the lower middle market: Why bigger isn’t always better

The vast size and makeup of the middle market presents both challenges and opportunities to extract value. Private equity funds have historically served as the primary way to invest in this diverse segment of the economy.

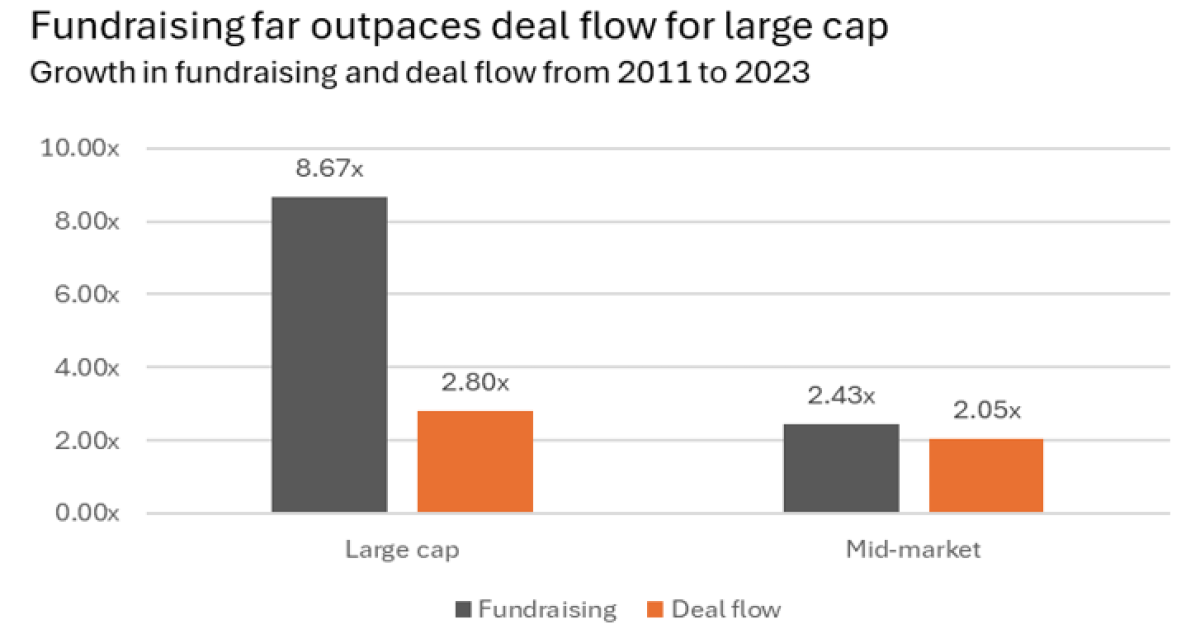

Middle market private equity managers have outperformed their large/mega cap peers over the long term. In fact, upper quartile U.S. mid-market buyout funds have outperformed large cap funds by over 500 basis points annually.[3] Despite performance, over the last decade, capital has predominantly flowed into large cap managers. This dynamic has resulted in larger funds far outpacing deal flow, creating higher competition and thus higher entry multiples for large deals. Large fundraising has grown by 8.67x while deal flow only 2.8x. On the contrary, middle market funds have experienced more proportional expansion with 2.43x growth in fundraising and deal flow growth at 2.05x.[4]

Within the middle market alpha generation has been driven by manager skill as well as attributes that are unique to the middle market and proven to be persistent over time, including:

- Lower pricing

- Less reliance on leverage

- More paths for value creation

- Greater exit options

Lower pricing begets lower leverage:

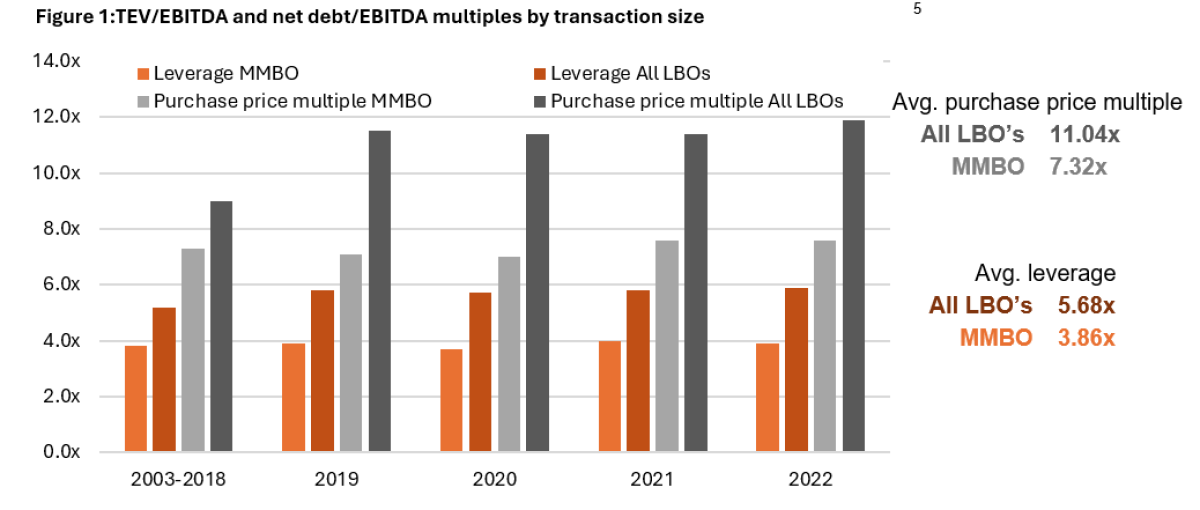

The average purchase price multiple for mid-market transactions is 34% lower than large cap transactions likely driven by a combination of the following factors:4

- A higher perceived level of risk due smaller size and earlier maturity in their life cycle compared to large cap companies

- The fragmented nature of the middle market which creates a lack of broad access to a company’s financial statement, management team track record and lack of financial

- The general lack of coverage of middle market companies by investment banks and other capital markets intermediaries.

Lower purchase prices multiples, in turn, require less leverage to finance middle market buyout transactions. The average middle market transactions typically use 32% less leverage compared to large cap transactions.4 This is especially important in today’s higher interest rate environment where the rising cost of capital has dampened M&A transaction volumes. Total PE buyout by deal value declined by -32.7% in 2023.[1] The U.S. mid-market fared much better, yet transaction volumes still declined by -18.9% last year. As a result, mid-market transactions accounted for 74% of all buyouts in 2023 – an all-time high.[2]

The mid-market showed notable signs of recovery as deal value and deal count increased 10.0% and 8.4% respectively in Q4 2023, standing in stark contrast to the broader buyout market which fell -27.1% and -12.6% respectively.6

Many paths to drive value:

With higher rates increasing acquisition financing costs, general partners (GPs) must rely more heavily on operational improvements such as growing an acquired firm’s revenue, revitalizing management teams, or increasing margins to drive value for their limited partners (LPs). Our desire for well-placed greed must take this real risk to forward returns into consideration.

Examining the historical drivers of value creation in the middle market, however, leaves us with some encouraging takeaways:

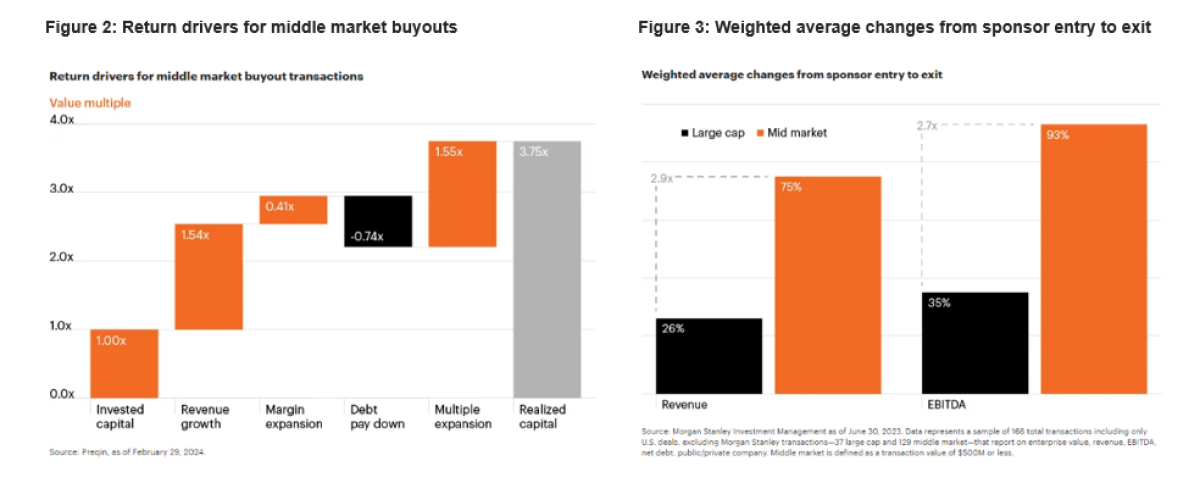

- Middle market managers tend to drive significant value creation by growing revenues and margins vs. their large cap peers. A Preqin study found that revenue growth contributed 1.54x to value creation for middle market transactions compared to 0.80x for large cap transactions across all industries and regions from 2006-2019. (Figure 2)

- Morgan Stanley conducted a similar analysis and determined that middle market managers grow revenue and EBITDA by nearly triple the amount of their larger cap peers from the time of purchase to exit (Figure 3).

- As result, middle market transactions have generated higher realized capital multiples (3.75x) than large cap buyout transactions (3.2x). (Figure 2)

Greater options for exit:

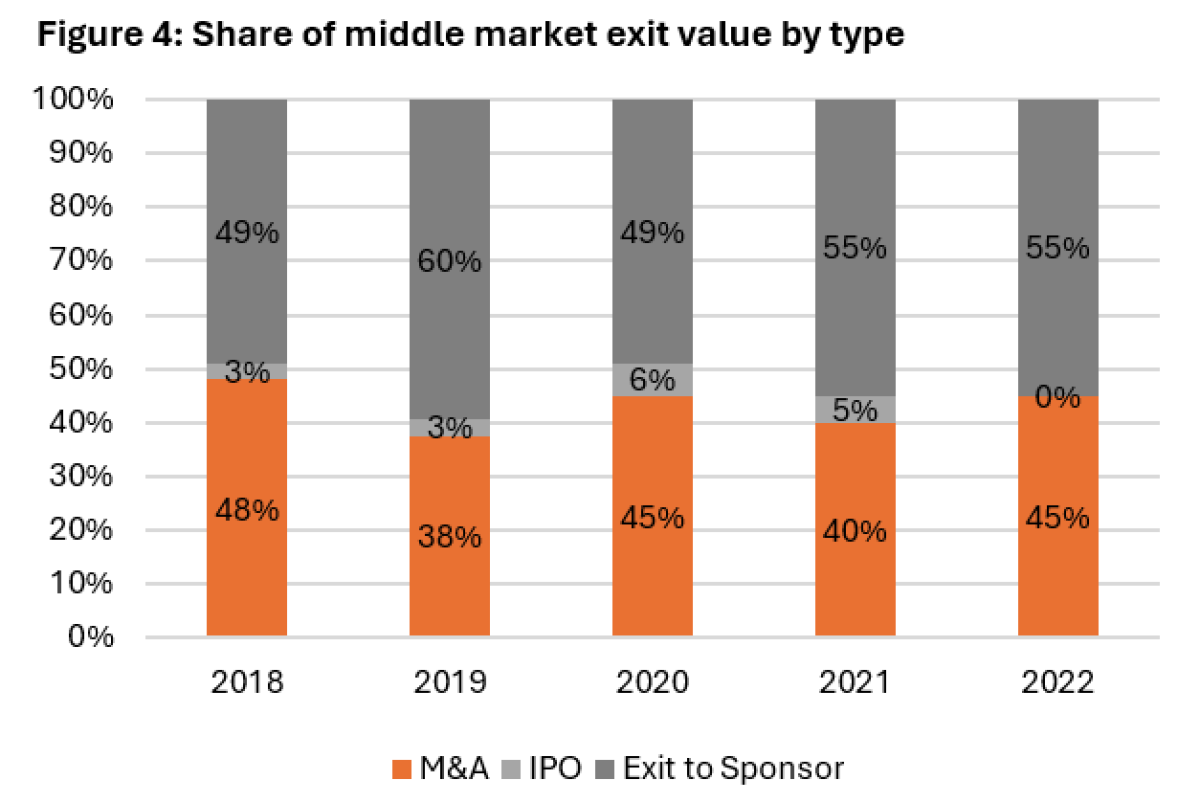

Lastly, as the saying goes, one investor’s exit is another’s entry point. Middle market managers have greater exit options beyond the IPO markets, a common avenue for large cap exits. In fact, from 2018-2022, approximately 97% of middle market exits were through sales to larger private equity sponsors (i.e. large cap funds) or to strategic corporate buyers via M&A activity (Figure 4).7 While holding periods are extending across the PE market, they are generally shorter for mid-market portfolio companies than the broader market.

Success going forward

We believe the U.S. middle market will continue to provide an attractive opportunity set versus large and mega cap managers as the segment offers capital structures less reliant on leverage, differentiated value creation strategies, and greater exit opportunities. While the opportunity set for mid-market buyout managers remains very large given the market’s size and relative inefficiencies, we emphasize the importance of manager selection as the market is relatively fragmented consisting of over 400 mid-cap focused buyout funds.[7] Investors should look for managers with operational expertise, advantages in deal sourcing, and industry specialization to help drive outperformance. When fundamental value creation becomes the largest driver of performance, go where it’s always mattered most.

Footnotes:

[1] McKinsey Global Private Markets Review 2024: Private markets in a slower era

[2] The National Center for the Middle Market. Middle Market Indicator, Year-End 2023

[3] Burgiss as of September 30, 2022. Mature U.S. Buyout funds defined as funds with a vintage year between 2000–2013. U.S. Large Cap defined as funds with a fund size greater than $5 billion. U.S. Middle Market defined as funds with a size less than $5 billion.

[4] Preqin 2024

[4] Pitchbook 2023 Annual U.S. Private Equity Breakdown

[5] Pitchbook 2023 Annual U.S. Private Equity Middle Market Report.

[6] Pitchbook, all U.S. LBOs as of March 31, 2023. GF Data, an ACG Company, M&A and Leverage Reports as of March 31, 2023. Leverage for all LBOs is calculated taking a simple average of yearly leverage and purchase price multiples from 2003-2018.

[7] Preqin. Total dollars raised versus number of funds raised by size. Sample set includes U.S. focused buyout funds closed since 2020.

More By This Author:

Have Option Selling Strategies Suppressed Implied Volatility?

Private Equity Continuation Funds

Proration -- Friend or Foe?

Comments

Log in or sign up to join the conversation.