This gives investors plenty of cash to buy any dips or drive the market higher.

“Davidson” submits:

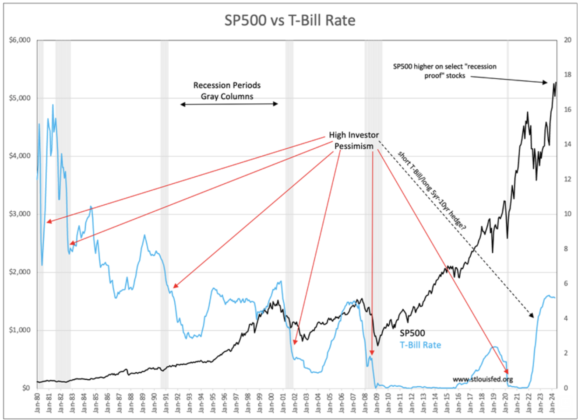

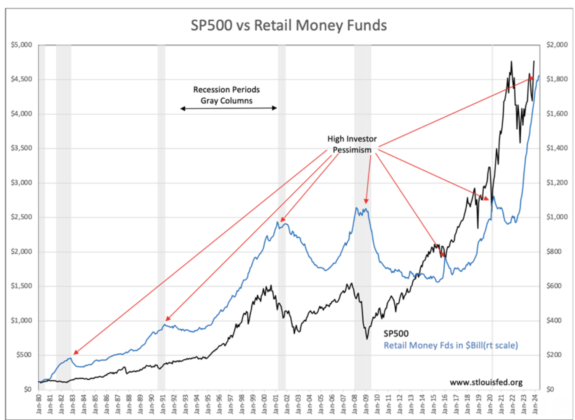

I am repeating this perspective precisely because the latest Retail Money Funds report emphasizes the unique situation investors face today that has no precedent in history. Two charts provide the market history we need to understand our current context. The investment history from 1980 for Retail Money Funds vs the T-Bill rate and SP500 has patterns that tightly correlate with investor psychology. Namely, when investors become fearful of losses, they shift capital out of equities to short-term secure investment vehicles i.e., T-Bills. Driving capital flows into Retail Money Funds forces T-Bill rates lower as the safest asset during past periods, coupled with a sharp decline in equities.

What makes today’s situation unique in history is that we have high pessimism and record retail flows into Retail Money Funds but T-Bill rates have risen not fallen. This is coupled with record SP500 due to a select few mega high tech issues deemed “recession proof” by institutions. Together, this defines the narrative for this unprecedented confluence of investment patterns. Institutions have made it clear they expect to profit during a recession as rates fall by owning 5yr-10y Treasuries and a select few tech issues that are expected to prosper regardless. The surge of retail capital seeking safety since Dec 2021 is nearly $1Trillion. The only way T-Bill rates can rise is if the institutions have shorted-T-Bills enough to counter this retail influx. Some have stated they are using this hedged strategy, short-T-Bills/long 5yr-10yr Treasuries. It is the only scenario that explains what we are seeing.

(Click on image to enlarge)

(Click on image to enlarge)

Not only is there a high level of pessimism reflected in these patterns but the confidence level is high that this strategy will work. They expect rates to decline shortly and in the process reap substantial gains. The Fed which follows T-Bill rates in setting the Fed Funds rate has modified its expectations for cuts as the T-Bill rate remains elevated. Thus far, institutional investors have not greatly modified their stance with the most recent disappointment in the PMI resulting in a yet higher T-Bill rate i.e., more shorting, and more buying of the 10yr. The proverbial monkey wrench is that the economic trends do not support recession. Outside the high tech world, revenues and earnings are growing well above expectations with guidance better than hoped. Investors briefly notice these results with one-day price surges that have faded only to be repeated on the next report with little overall upward price movement. But, history has one lesson for us with investor psychology i.e., economics has always won the upper hand with investors regardless of the prior psychological positioning.

I fully concur with the recent headline, “Sell Big-Tech & Bitcoin, Buy Everything Else… Link here.

More By This Author:

Data Still Murkey

PMI Often Cries Wolf

Construction Spending At Record Highs

Comments

Log in or sign up to join the conversation.