Image Source: Pixabay

QuantumScape (QS) isn’t your typical EV battery company, it’s a bold bet on the future of energy storage. Positioned at the bleeding edge of solid-state battery (SSB) innovation, QuantumScape isn’t selling batteries yet, however it’s selling a vision: safer, faster-charging, and longer-lasting power for electric vehicles.

In the lead-up to Q2 2025 earnings, QuantumScape captured renewed investor attention thanks to the rollout of its Cobra separator which is a major technical milestone in its battery development process. The excitement pushed shares up more than 200% in just weeks, fueled by hope for commercial breakthroughs.

However, the actual earnings report offered no revenue, a –$0.20 per share loss (in line with expectations), and no new customer or licensing updates, reminding investors that this remains a long-term play with no near-term cash flow.

Now, with no sales, a commercialization timeline stretching beyond 2026, and an $8B+ market cap, some investors are asking: has the market priced in success before it’s earned?

The reality? While the technology is promising, the road to mass production is long and competitors like BYD and CATL are making rapid advances in conventional lithium-ion batteries that challenge the need for SSBs. Still, for believers in a cleaner, more powerful EV future, QuantumScape remains one of the most compelling moonshot plays in the market today.

IDDA Point 1 & 2: Capital & Intentional

Before investing in QuantumScape, ask yourself:

Are you willing to bet on a company with no current revenue but potentially breakthrough technology?

Do you want exposure to the next frontier of EV batteries – even if it means waiting years for returns?

Do you understand this is a high-risk, high-reward speculation, not a value or dividend play?

QuantumScape isn’t aiming to compete with today’s battery producers, it’s trying to leapfrog them entirely. Its intentional strategy focuses on developing solid-state lithium-metal batteries that solve the industry’s biggest pain points: safety, charging speed, energy density, and lifecycle. This isn’t about scaling today’s tech; it’s about rewriting the rules entirely.

The company’s focus on licensing, not mass production, reflects a leaner, capital-light model. Strategic partnerships with Volkswagen’s PowerCo and Murata aim to accelerate development while reducing CapEx pressure. The vision is clear but execution risk remains high.

IDDA Point 3: Fundamentals

Technology & Production Roadmap

QuantumScape’s most recent breakthrough is the integration of its Cobra separator into baseline production. This upgrade offers an approximate 25x improvement in heat treatment speed compared to its previous Raptor process and takes up significantly less space, potentially enabling more scalable gigafactory-level production. However, the company is still in the early stages of execution, with QSC-5B1 sample shipments planned for late 2025 and initial commercial field testing expected in 2026 with PowerCo. Joint manufacturing efforts and automation upgrades are ongoing with PowerCo engineers, and production scale-up remains a top priority.

Financials & Liquidity

Despite strong investor interest, QuantumScape remains a pre-revenue company, reporting a Q2 2025 net loss of $0.20 per share, in line with expectations. The company continues to invest heavily in R&D, with a projected EBITDA loss of $250M–$280M for FY2025 and no commercial sales expected until at least 2026–2027. While it holds a solid $860M cash balance, providing runway through the second half of 2028, the high burn rate raises concerns about potential equity dilution, especially after the recent surge in its stock price.

Revenue Outlook

QuantumScape’s revenue forecasts are minimal through 2027 – only around $65M combined, with $4.5M projected in 2026 and $60M+ in 2027. This limited near-term revenue, combined with a royalty-focused deal structure with Volkswagen (rather than full-scale manufacturing), tempers enthusiasm around commercial upside. While the company has a $130M pre-payment agreement with PowerCo, no revenue has been recognized yet as the deal is milestone-dependent. The broader commercialization push is expected post-2028, making this a very long term play.

Partnerships & Licensing Potential

Strategic partnerships remain a key part of QuantumScape’s growth narrative. The deal with PowerCo is crucial, and a potential long-term partnership with Murata, to supply ceramic separators, could help expand QuantumScape’s reach beyond its own manufacturing. Additionally, the company has received strong interest in its licensing model, with management citing “overwhelmingly positive” feedback from potential customers. However, these deals still hinge on technical milestones and field validation yet to be completed.

Competition & Market Threats

While solid-state batteries (SSBs) promise major performance benefits, such as higher energy density, faster charging, and improved safety, traditional EV battery makers like BYD and CATL are rapidly closing the gap. BYD’s Super e-Platform enables 249 miles of range in just 5 minutes, and its Blade Battery offers up to 5,000 charge cycles. If legacy lithium-ion technologies continue improving at this pace, the unique value proposition of SSBs could diminish, placing pressure on QuantumScape’s long-term competitiveness.

Fundamental Risk: High

IDDA Point 4: Sentimental

Strengths

Strong Cash Position – With $860 million in cash and no debt, QuantumScape has the financial runway to continue R&D and reach critical milestones without immediate funding pressure.

Breakthrough Technology Potential – The Cobra separator represents a major leap in battery engineering, offering faster production, better thermal management, and a path toward scalable solid-state battery manufacturing.

Growing Interest in Licensing Model – QuantumScape has received overwhelmingly positive feedback from potential customers on its licensing model, which could provide a high margin revenue stream once commercial validation is achieved.

Risks

Lack of Clear Commercial Timelines – Despite years of development, QuantumScape has yet to provide a firm, quarter-specific timeline for key milestones like field testing or revenue generation, which adds uncertainty and weakens investor confidence in execution.

No Proven Product-Market Fit Yet – QuantumScape has not yet demonstrated that its solid state battery technology can perform reliably at scale in real-world EV applications, leaving questions about long-term viability and demand.

Heavy Dependence on a Single Customer (PowerCo) – With most commercial expectations tied to

Volkswagen’s PowerCo, QuantumScape’s revenue potential is highly concentrated. A delay or cancellation from PowerCo could severely impact the company’s growth trajectory.

QuantumScape’s recent surge, tripling in value following the Cobra separator news, has been fueled largely by hype and speculative momentum rather than fundamentals. The subsequent 22% pullback helped cool some of the excessive enthusiasm, setting a more balanced tone heading into Q2 2025 earnings.

However, expectations remained high, with investors hoping for updates on customer partnerships, licensing progress, or clearer field testing timelines. Instead, the earnings report offered no new catalysts i.e no commercial deals, no revenue milestones, and no revised roadmap, which disappointed a market already priced for good news.

As a result, the stock faced a classic “sell-the-news” reaction, with shares falling sharply in after hours trading. While the company reiterated prior guidance and confirmed continued R&D progress, the absence of any upside surprise triggered a shift in sentiment.

Analysts and retail investors are beginning to move from speculative optimism toward a more cautious realism. Confidence in the long-term potential of the technology remains, but without meaningful commercial milestones or near-term revenue, the short-term upside appears limited.

Sentimental Risk: Very High

IDDA Point 5: Technical

On the weekly chart:

Historically, the Ichimoku cloud has been bearish, and it remains bearish and flat at present.

Candlesticks are positioned above the cloud, reflecting recent bullish sentiment and a strong price upswing.

The RSI is overbought at 76.53, indicating that the uptrend may be short-lived and a pullback is likely in the near term.

Historically, the stock has struggled to perform over the long term, remaining in a general downtrend since inception with periodic sharp swings where many retrace as much as 100%. While this highlights its volatility, it also presents opportunities for short-term profit-taking during speculative rallies.

The most recent upswing came as the market reacted positively to the announcement of the Cobra separator. However, with the Ichimoku cloud still flat and bearish, and the RSI in overbought territory, the current rally may be losing steam.

(Click on image to enlarge)

On the daily chart:

The future cloud is bullish, reflecting recent upward momentum driven by excitement around the Cobra separator.

Candlesticks, along with the Kijun, Tenkan, and Chikou lines, are all positioned above the cloud, reinforcing current bullish momentum.

The RSI is overbought at 68.51, suggesting a potential pullback as sentiment shifts following Q2 earnings.

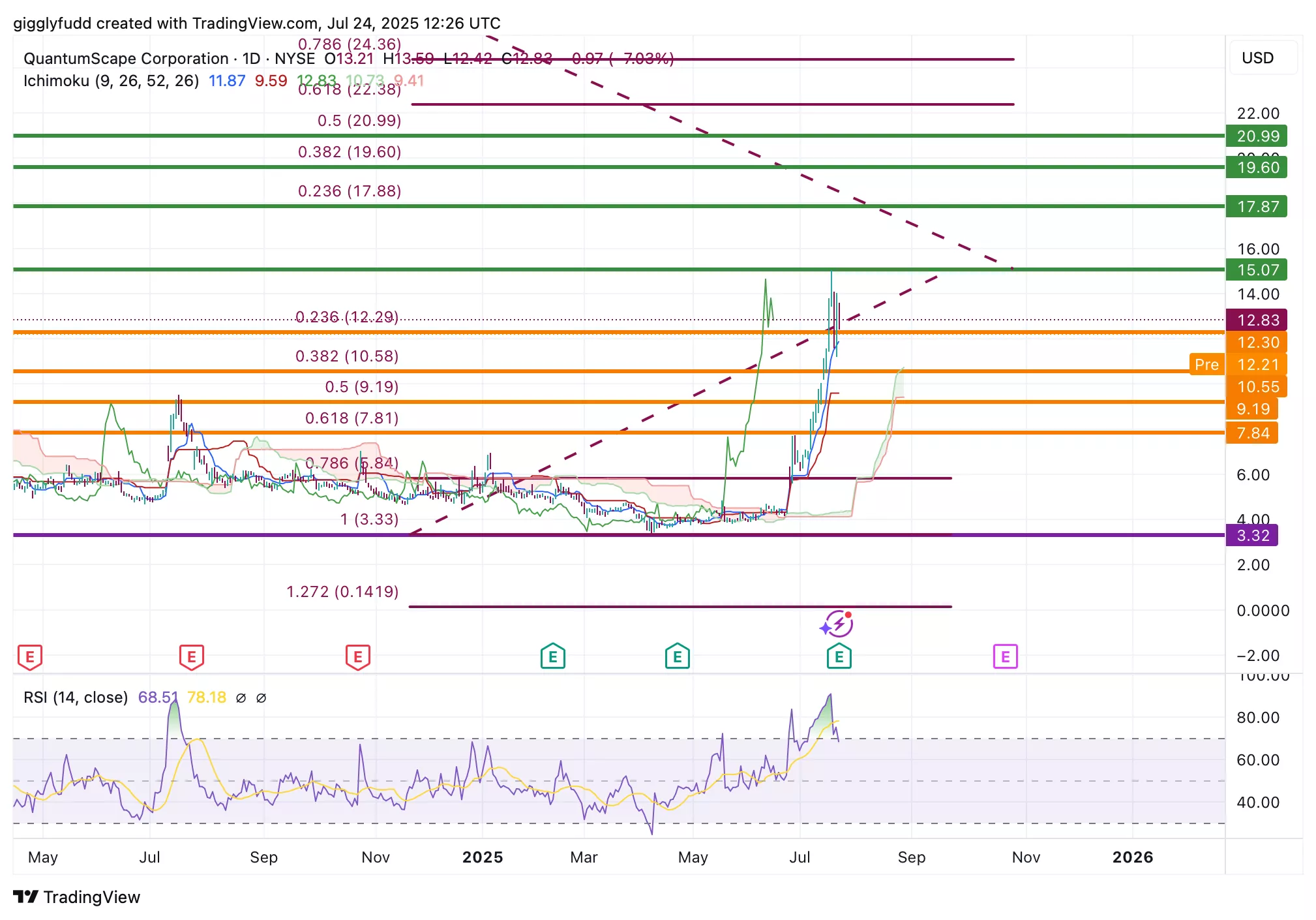

On the daily chart, the stock had been consolidating through late 2024 and early 2025 before trending upward in late June, driven by optimism around the Cobra separator. However, following the Q2 earnings report, the stock has started to decline, potentially signaling the beginning of a short-term pullback, and has already touched the 23% Fibonacci retracement level.

(Click on image to enlarge)

Investors looking to get into QS can consider these Buy Limit Entries:

12.30 (High Risk)

10.55 (High Risk)

9.19 (Medium Risk)

7.84 (Low Risk)

Investors looking to take advantage of these swings can consider setting Sell Limit orders at the following levels:

15.07 (Short term)

17.87 (Medium term)

19.60 (Long term)

20.99 (Long term)

Here are the Invest Diva ‘Confidence Compass’ questions to ask yourself before buying at each level:

- If I buy at this price and the price drops by another 50%, how would I feel? Would I panic, or would I buy more to dollar-cost average at lower prices? (hint: this question also reveals your

- CONFIDENCE in the asset you’re planning to invest in).

- If I don’t buy at this price and the stock suddenly turns around and starts going up again, will I beat myself up for not having bought at this level?

Remember: Investing is personal, and what is right for me might not be right for you. Always do your own due diligence. You should ONLY invest based on your own risk tolerance and your timeframe for reaching your portfolio goals

Technical Risk: High

Final Thoughts on QuantumScape (QS)

QuantumScape (QS) is a high-risk, high-reward play on solid-state battery technology, recently gaining attention after integrating its Cobra separator into production – a step toward scalable manufacturing. Backed by $860M in cash and key partnerships with PowerCo and Murata, it has the resources to push forward despite having no revenue.

However, field testing isn’t expected until 2026, and commercial sales remain years away. In Q2 2025, the company reported a $0.20/share loss with no new deals, leading to a post-earnings selloff. Technically, the stock tripled before earnings but has since pulled back over 20%, with bearish signals forming across both weekly and daily charts.

Key Takeaways: Speculative Hold or Opportunistic Buy on Pullback (for those with a minimum high risk tolerance)

QuantumScape presents a high-risk, high-reward opportunity for investors who believe in the future of solid-state batteries and are willing to play the very long game. While the recent hype has cooled and near-term catalysts are limited, the company’s strong cash position, technological edge, and global partnerships provide long-term potential.

For now, short-term profit-taking is expected, but for patient investors with a minimum high risk tolerance, QS could be a valuable moonshot in the EV ecosystem.

Overall Stock Risk: High

More By This Author:

What If The Next Quantum Leader Isn’t IBM Or Google… But Rigetti Stock?

First Apple, Now The Pentagon… What’s Really Going On With MP Materials Stock?

Under-The-Radar Moves Are Shaping Qualcomm Stock - Should You Be Worried Or Excited?

Comments

Log in or sign up to join the conversation.