PayPal Holdings (PYPL) shares are tumbling 14% in premarket trading following the release of its fourth-quarter 2025 earnings report, which fell short of analyst expectations on profits. The fintech giant reported adjusted earnings of $1.23 per share, missing the consensus estimate of $1.28, while revenue came in at $8.68 billion against the anticipated $8.80 billion. Adding to investor concerns, PayPal's guidance for 2026 was lighter than expected, projecting adjusted profit to range from a low-single-digit decline to a slight increase, far below Wall Street's forecast of about 8% growth.

This disappointing outlook reflects ongoing challenges in consumer spending amid economic pressures, highlighting vulnerabilities in the payments sector.

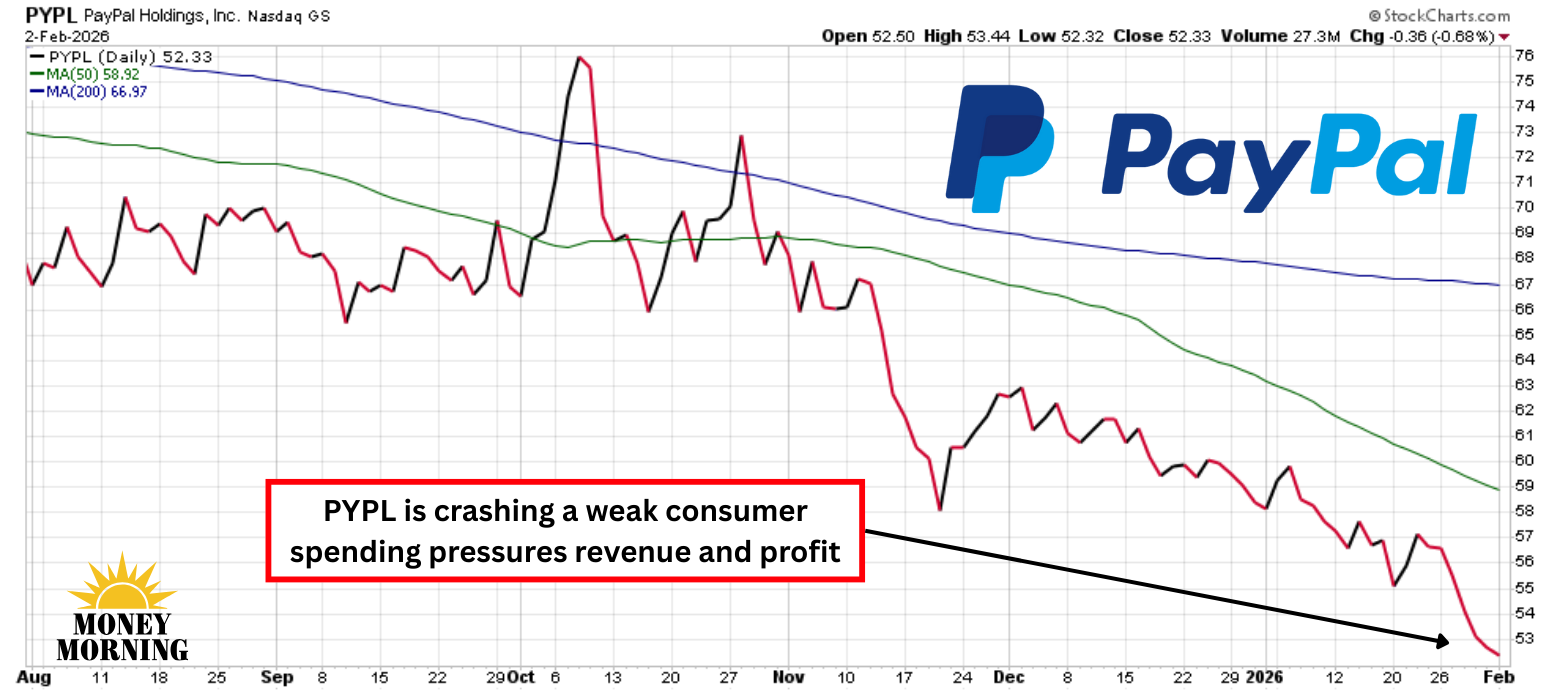

Disappointing Q4 Results Amid Weaker Spending

The earnings miss was largely attributed to softer consumer spending in the U.S., where high interest rates, elevated living costs, and a cooling labor market have made shoppers more cautious. PayPal's total payment volume (TPV) grew 6% on a currency-neutral basis to $475.1 billion, but this was overshadowed by deceleration in key segments.

Notably, growth in the branded checkout business slowed to just 1% in Q4, down from 6% a year earlier, driven by weakness in U.S. retail, international headwinds, and tougher year-over-year comparisons. Typically, the holiday quarter sees robust spending on gifts, travel, and promotions, but this year, consumers pulled back, impacting PayPal's transaction volumes and margins. The company also faced competitive pressures from Big Tech players like Apple (AAPL) and Google, which continue to erode market share in digital payments.

Despite these headwinds, PayPal highlighted some positives, such as steady performance in core products and efforts to streamline costs under outgoing CEO Alex Chriss. However, the overall results underscore how macroeconomic factors are weighing on discretionary spending, forcing fintech firms to adapt to a more frugal consumer environment.

(Click on image to enlarge)

Lackluster 2026 Outlook Raises Concerns

Looking ahead, PayPal's 2026 guidance has amplified investor worries, with projected profit growth falling well short of expectations. The company anticipates adjusted earnings to potentially decline in the low single digits or rise modestly, citing persistent softness in consumer spending as a primary drag. This conservative forecast comes amid broader economic uncertainty, including interest rate and labor market trends that could further suppress retail activity.

Analysts had hoped for stronger momentum, but PayPal's outlook suggests ongoing challenges in revitalizing growth. The firm is focusing on profitable expansion and operational efficiency, but external pressures like high inflation and competition may limit upside. This has led to questions about PayPal's ability to regain its pre-pandemic growth trajectory in a maturing digital payments landscape.

Bottom Line

In a bid to steer the ship back on track, PayPal has appointed Enrique Lores as its new president and CEO, effective Mar. 1, replacing Alex Chriss who emphasized cost-cutting and profitable growth during his tenure. Additionally, the company initiated its first-ever quarterly dividend of $0.14 per share, payable Mar. 25. It signals a shift toward returning capital to shareholders and potentially attracting income-focused investors.

This dip could present a buying opportunity for contrarian investors. Despite the near-term headwinds, PayPal's strong free cash flow generation – projected at $6 billion to $7 billion annually – and undervalued stock trading at low forward P/E multiples suggest long-term potential. With a new CEO at the helm and a new dividend, PYPL may rebound as economic conditions improve, making it worth considering for those betting on a fintech recovery.

Beat the market, without relying on brokers or biased institutions.

More By This Author:

Is Bitcoin About To Get Hit By A Polar Vortex?

Nvidia's Jensen Huang Says OpenAI Investment Will Be "Largest Ever"

Here's Why Joby Aviation Was Yesterday's Biggest Loser

Comments

Log in or sign up to join the conversation.