Palantir Is A Buy: Why This Stock Could Go A Lot Higher

Palantir (NYSE: PLTR) had a strong run-up in 2020 and early 2021, but lately, the stock has mostly moved sideways. Palantir is a market leader in big data analytics and has significant growth potential and plenty of market share to capture. The company already caters to top government agencies, corporations, and sectors across numerous industries. The company is continuously improving and growing its business segments, and Palantir should continue to attract new clients in the future. Moreover, the company should continue to increase revenues and grow EPS as we advance. Palantir's stock will likely rise from here and could double within the next several years.

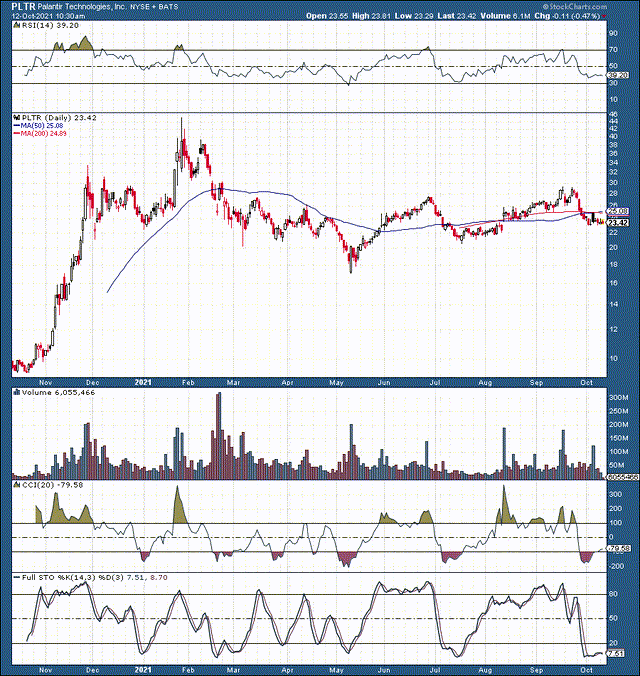

The Technical Setup

Source: Stockcharts.com

Palantir has been in a relatively tight trading range ($20-30) for most of this year. However, we see the stock making slightly higher highs and higher lows in recent months. There is now strong support around the $22 and $20 support levels. Additionally, the full stochastic, the CCI, and other technical indicators imply that the stock will likely shift towards a more positive technical momentum. Given the technical setup, a breakout above the $30 resistance level seems probable within the next several months.

Palantir's Businesses

Palantir operates out of three core segments. Gotham, Metropolis, and Foundry are the three main "projects" that the company is known for right now. While Palantir is a leading software big data analytics company, what I find most interesting is the company's client list.

The company's Gotham program is used by U.S. counter-terrorism analysts at the U.S. Intelligence Community and the Department of Defense. Moreover, the CIA, DOD, and numerous other intelligence and defense branches use Palantir's services. Government contracts are the primary source of income and growth for Palantir, and the company continues to attract clients amongst government agencies. The company signed contracts with the CDC, the U.S. Special Operations Command, the United States Space Force, and others.

The U.S. government would not use the services of an unreliable or incompetent company. The trusted seal of approval of the U.S. government is excellent for Palantir, as it signals that the firm is highly competent and can be trusted. Furthermore, government contracts are often recurring and can deliver steady long-term revenues for Palantir.

Palantir Metropolis is data integration, information management, and quantitative analytics software used primarily by banks, hedge funds, and other financial institutions. Metropolis is a lucrative area the company can continue to expand operations in.

The company's Foundry program is Palantir's software designed for other corporate clients. Over 200 companies already use Palantir's software, and the list continues to grow. Palantir will likely continue to improve operations and increase clients in its corporate segment. This trend should enable revenues to continue to expand and EPS to rise.

Palantir's Growth Story

With revenues looking to surge by about 38% this year, Palantir is one of the most exciting growth stocks around today. Analysts expect Palantir to report $1.5 billion in revenues in 2021, and sales could triple to more than $5 billion by the end of 2025.

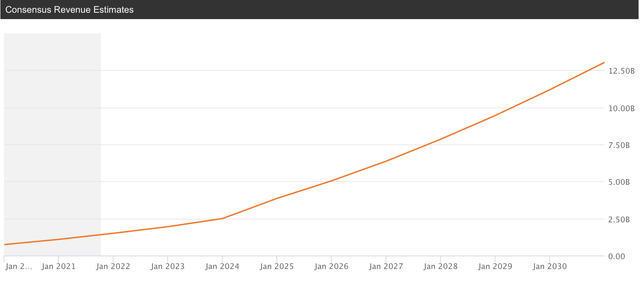

Revenue Growth

Source: seekingalpha.com

Palantir's revenues have doubled since 2019, and sales growth should continue to surge as we move ahead. The company has a powerful presence amongst government agencies, which provides Palantir with a continuous stream of lucrative government contracts. Additionally, the company continues to expand its reach in the corporate sector as well. It's important to consider that Palantir has a great deal of market share to capture, and the company has a remarkably long growth runway. We could see significant double-digit growth continue for many more years with Palantir as we move ahead. Therefore, the company's P/E ratio will likely remain relatively high well into the future.

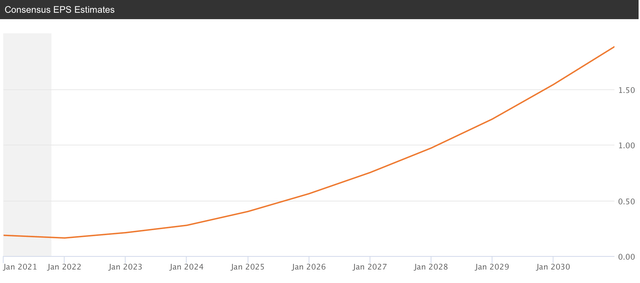

EPS Projections

Source: seekingalpha.com

While the company's EPS may appear relatively low right now, earnings will likely surge in the future. After all, this kind of earnings dynamic is what we should expect to see from a growth company. Limited EPS growth while the company is expanding operations and growing revenues is a normal phenomenon. Once Palantir gets more established in its core industries, we will likely see growth slow down and EPS increase as the company begins emphasizing earnings rather than growth.

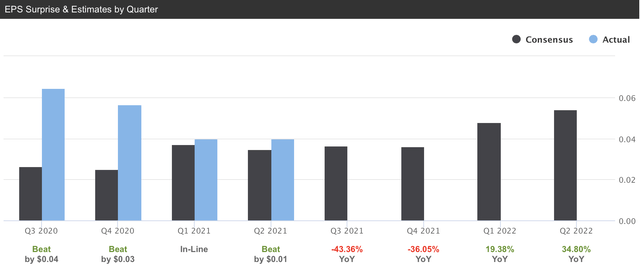

Beating the Analysts

Source: seekingalpha.com

Palantir is becoming quite adept at beating consensus analysts' projections. While analysts expected the company to produce $0.12 in EPS, Palantir delivered $0.20 instead. This outperformance is a significant 67% beat over the estimates. Now, we may not see 50-100% EPS beats in future years, but Palantir's EPS results could come in towards the higher end of estimates as we advance.

Here's What Palantir's Earnings Could Look Like in Future Years:

| Year | 2021 | 2022 | 2023 | 2024 | 2025 | 2026 | 2027 | 2028 | 2029 |

| Revenue growth | 38% | 30% | 28% | 55% | 32% | 28% | 25% | 20% | 19% |

| EPS $ | 0.16 | 0.24 | 0.32 | 0.44 | 0.65 | 0.90 | 1.15 | 1.45 | 1.90 |

| P/E ratio | 150 | 145 | 140 | 125 | 100 | 94 | 87 | 83 | 71 |

| Price | $24 |

$35 |

$45 | $55 | $65 | $85 | $100 | $120 | $135 |

Source: Author's material

My earnings estimates are just slightly higher than the consensus analysts' figures. However, I don't believe that I am overly optimistic about the stock price here. Due to Palantir's substantial revenue growth and earning capacity, we will likely continue to see a relatively high P/E ratio for this stock. This dynamic is nothing out of the ordinary, as we see relatively high P/E ratios persist in other dominant market-leading names with high growth prospects.

The Bottom Line

Palantir is a unique company that should continue to expand revenues and increase EPS as we move forward. The company has a very prominent position in the lucrative government software sector. Moreover, Palantir continues to improve its market position in its corporate segments as well. The company has significant growth potential and should continue to deliver double-digit revenue growth for many years. In addition, Palantir is already showing a tenacity for surpassing analysts' expectations, and the company could continue to bring in higher earnings than the market expects. I suspect that Palantir's stock can have a sustainable move up to around $50 over the next 1-3 years. After this appreciation, shares of Palantir can continue to move higher.

Risks to Consider

Despite my bullish outlook for Palantir, market participants should consider some potential risks. While the growth story is strong at Palantir, shares are far from cheap, and the company's earnings are still quite limited. Moreover, if the company's growth picture were to turn less bullish for whatever reason, the stock could head in the wrong direction. For instance, if Palantir lost favor with the government or had a data breach, the stock could experience a notable decline. Palantir is not a value company. It is an elevated-risk/high reward potential stock. The company needs to execute almost flawlessly and operate optimally for the stock price to continue to grow.

Disclosure: I/we have a beneficial long position in the shares of PLTR either through stock ownership, options, or other derivatives.

Disclaimer: This article expresses solely my opinions, is ...

more

Quite a detailed analysis, and certainly some interesting projectins.

Thanks for the article!