An investor reading Microsoft’s (MSFT) and Tesla’s (TSLA) earnings summaries on Wednesday night would likely anticipate that MSFT shares would trade higher and Tesla shares lower. At the opening of the market the following day, the opposite held. MSFT opened up 4% lower, while TSLA was 4% higher. Let’s summarize their respective earnings to see how sentiment, not fundamentals, plays a critical role in short-term stock performance.

MSFT opened 4% lower despite beating earnings and revenue estimates. Other than market sentiment regarding the impact of DeepSeek, investors are focusing on Azure, its cloud services division. This driver of marginal growth for MSFT grew by 31%, slightly less than last quarter’s 34%. Also of note is that they expect CAPEX spending to grow by 52% in 2025. While that will hurt margins, it’s an investment in the future and should be considered positive, given their investment track record.

TSLA rose 4% on the open despite weak earnings. They reported that revenues fell by 6%, and GAAP net income was down 53%. Notably, profits and revenues have been flat for over two years now. Moreover, some of their gains were due to an unrealized $600 million increase in the value of their digital assets (crypto). While growth at TSLA appears to be dwindling, investors are enamored with Elon Musk. He said he expects TSLA to be larger than the top five companies by market cap combined. CAPEX at TSLA is expected to be similar to 2024 levels.

While earnings matter significantly in the long run, sentiment has the biggest short-term impact on share prices. MSFT is trading poorly largely because investors are concerned about DeepSeek’s impact. Conversely, TSLA shares have extreme valuations as investors buy into Musk’s growth forecasts.

(Click on image to enlarge)

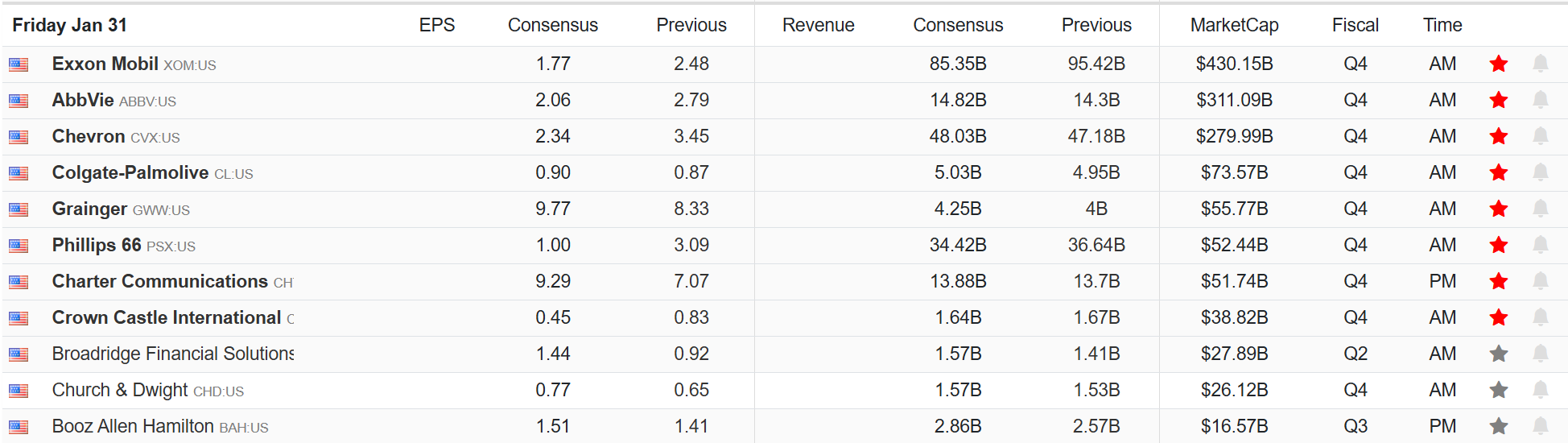

What To Watch Today

Earnings

(Click on image to enlarge)

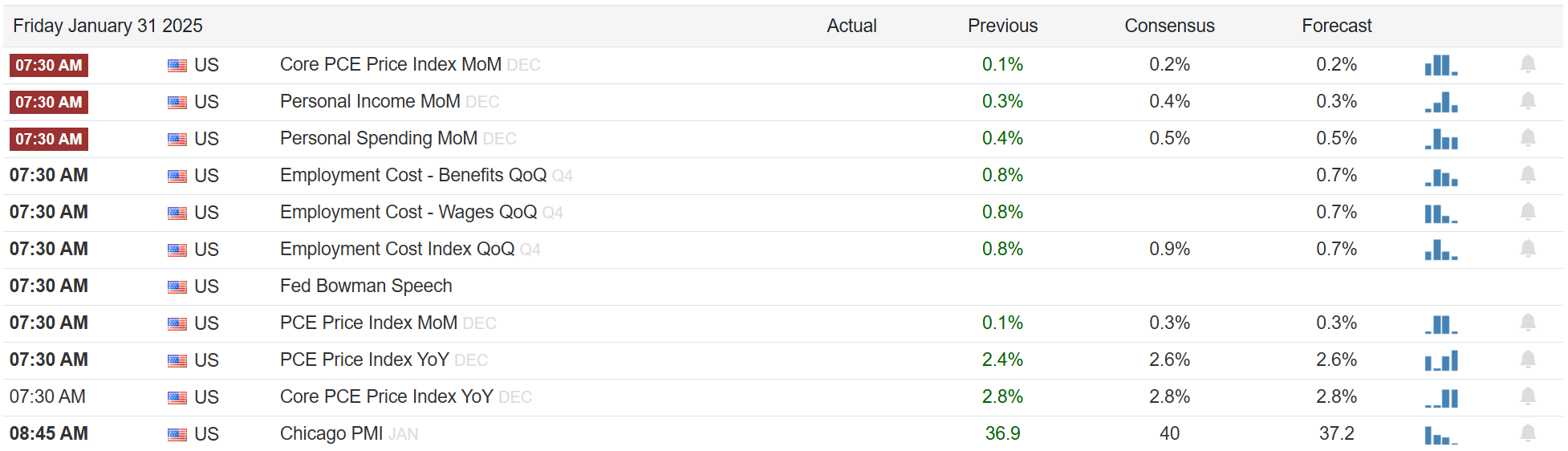

Economy

(Click on image to enlarge)

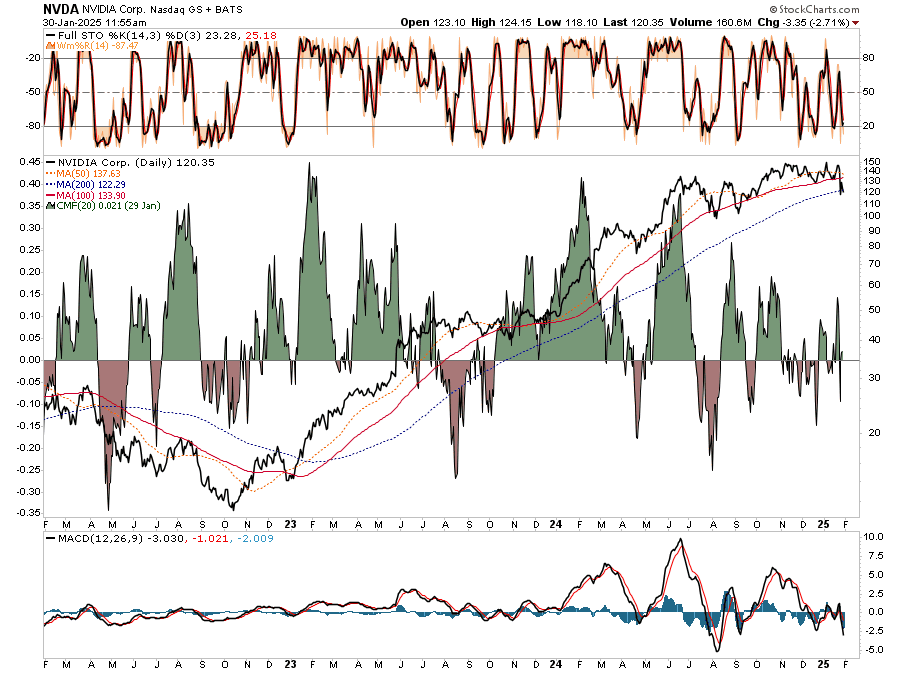

Market Trading Update – To Buy NVDA Or Not?

Yesterday, we addressed watching “money flows” into the market to help better determine when to increase or reduce overall market risk. We can apply the same to individual equities to help determine when, or in this case, even if, we should buy or add to an existing position.

Over this past week, Nvidia (NVDA) has come under fire over threats by DeepSeek to its core A.I. business of selling the GPUs needed to support future development, growth, and data centers. To be honest, I don’t have that answer with certainty. However, we hold a long position in NVDA and now need to determine if the recent decline is a “buy the dip” moment or a change that suggests reducing the position in the portfolio. For that analysis, we need to revert to some price analysis to try and determine our near-term and longer-term risks.

Starting with a daily technical chart, NVDA is getting oversold on multiple levels and is testing support at the 200-DMA. While the recent selloff was notable, money flows continue to remain positive for the moment. Notably, previous deep oversold conditions have led to short-term reflexive bounces that provided a better exit point to reduce or exit current holdings. As such, while near-term volatility may be nauseating, some patience will likely allow for a better point to rebalance risks in NVDA.

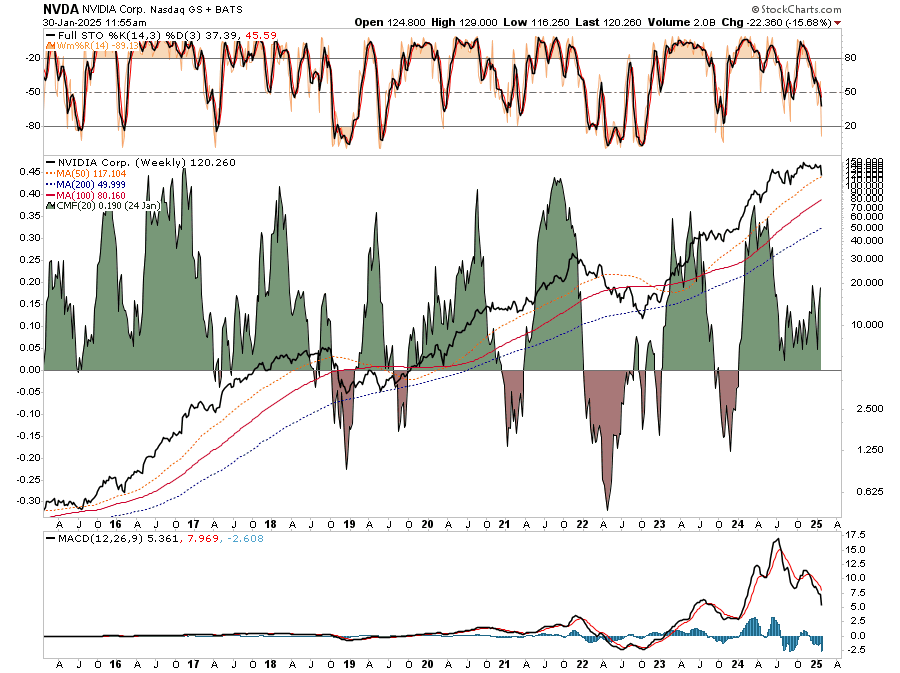

Using weekly data gives us a little more context. While the short-term analysis is deeply oversold, the intermediate analysis suggests that NVDA may need to consolidate or correct further before a better long-term entry point is available. In other words, holding NVDA may be “dead money” until more holders are washed out of their positions. The long-term analysis further confirms this.

The monthly data shows the current extreme overbought condition in NVDA. Historically, such overbought conditions were resolved through long consolidation and reversion processes. This time is unlikely to be different, suggesting that the next entry point could be closer to $50/share, substantially lower than current levels. While we are not saying with certainty that NVDA will drop to such levels, there is a risk it could. As seen previously, we will most likely see a long period of very choppy and volatile action that eventually exhausts buyers.

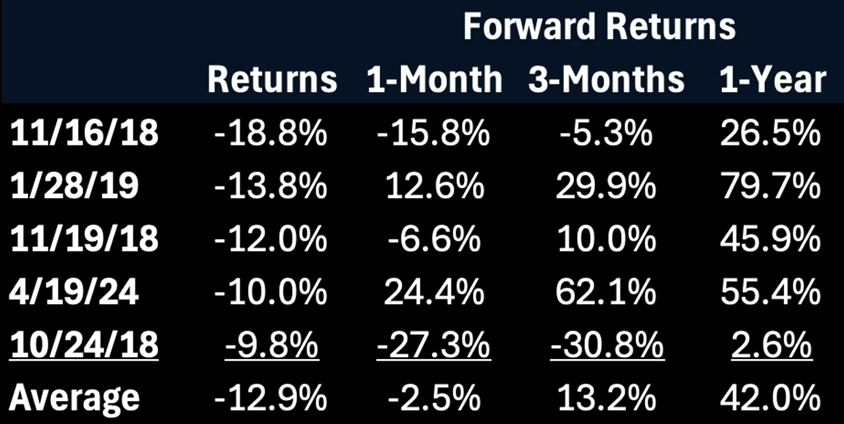

Notably, as pointed out by TheMarketEar, be careful suggesting that the recent decline is anything more than a reversion of massively overbought conditions. The past five times, the stock went down a lot; it was a massive buying opportunity if you had staying power for at least one year.

“This was Nvidia’s third worst daily decline since 2014 (i.e., since the start of the US Big Tech’s slow-motion takeover of the S&P 500), so let’s put that move in historical context. Here’s a table of NVDA’s 5 worst daily declines since 2014 (excluding the Pandemic Crisis), as well as their 1-month, 3 month, and 1-year forward returns”

While we currently own a small portfolio position in NVDA and have bought and sold pieces of it many times over the last few years, we will likely use a rally to reduce the position and evaluate its future potential. Once NVDA finds its footing, we can increase our portfolio weighting again.

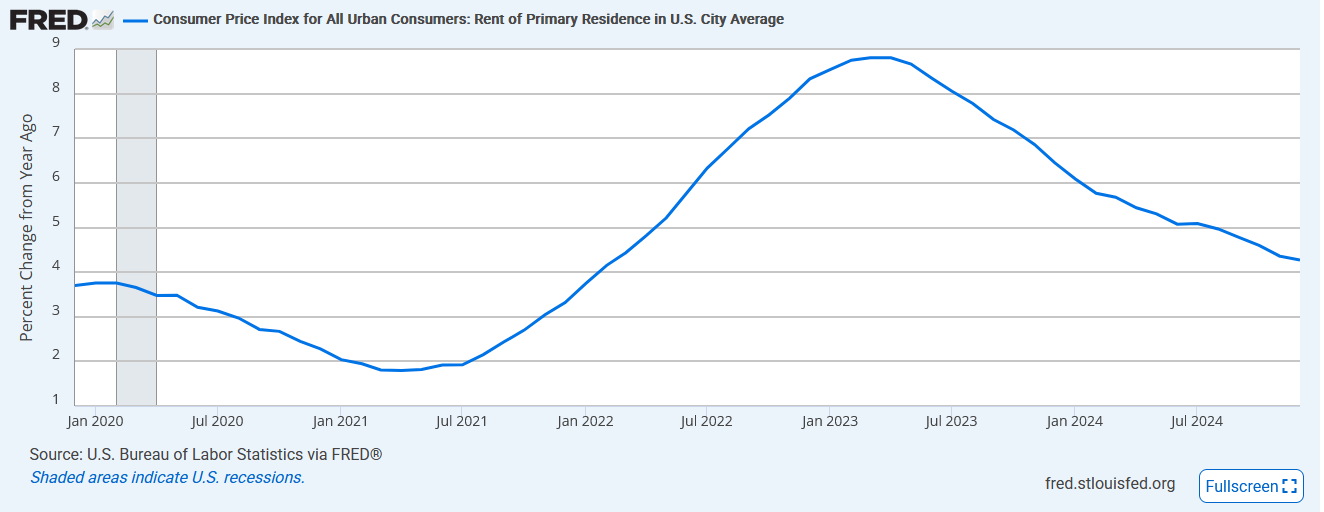

CoreLogic Confirms What We Knew

We often discuss the lag between the CPI shelter and market-based rent prices. At 36% of CPI, lagging rent data is critical to assess. While most market based rental data shows near zero inflation, CoreLogic was still showing more substantial rent price growth. However, its recent update shows a catch-down to other market data services. Per CoreLogic:

Single-family annual rent growth slowed in November to the lowest rate in about 14 years. Wage growth outpaced single-family rent growth for much of the past two years which kept rent growth in positive territory

CoreLogic claims rent growth is now 1.5%. Other services are flat to negative. The truth probably lies in the middle. CPI rent, shown below, is still over 4%, although recent annualized monthly readings have fallen to a range of 2.5% to 3.5%. Again, when CPI catches up to CoreLogic and the other data, CPI will close in on the Fed’s 2% goal.

UPS Tumbles

UPS fell by over 15% on Thursday, sending its shares to levels last seen in early 2020. Their earnings report is the culprit, although its current earnings are decent. EPS was well above estimates at $2.75. Revenue fell a hair short of estimates. Some concern is warranted as they reduced their revenue estimate by a little over 5% for 2025. However, the likely culprit behind the steep decline is an agreement with Amazon to reduce 50% of its shipping volume by the end of 2026.

The question is whether the market has already priced in the Amazon news. To that end, its forward P/E is down to 11. Its PEG is 1.38, and its Price to Sales ratio is 1.04. Lastly, it now boasts a dividend yield of 6%. Some may say it is now a value stock. That may be the case if management can deliver on some of its promises to shareholders.

(Click on image to enlarge)

Tweet of the Day

More By This Author:

Rate Cuts Put On HoldThe Chart That Should Worry The Fed

Emerging Junk In Demand

Comments

Log in or sign up to join the conversation.