Image Source: Pixabay

With all eyes firmly focused on CapEx numbers to keep the AI-expansion narrative alive, Microsoft beat expectations on top- and bottom-line, and operating income, but a bigger than expected CapEx.

“We are only at the beginning phases of AI diffusion and already Microsoft has built an AI business that is larger than some of our biggest franchises," said Satya Nadella, chairman and chief executive officer of Microsoft.

“We are pushing the frontier across our entire AI stack to drive new value for our customers and partners.”

Microsoft posted adjusted earnings of $4.14 a share on revenue of $81.3 billion (better than expected earnings of $3.91 a share and revenue of $80.3 billion), beating across every segment:

- Intelligent Cloud revenue $32.91 billion, estimate $32.39 billion

- Azure and other cloud services revenue Ex-FX +38%, estimate +38%

- Productivity and Business Processes revenue $34.12 billion, estimate $33.45 billion

- More Personal Computing revenue $14.25 billion, estimate $14.33 billion

“Microsoft Cloud revenue crossed $50 billion this quarter, reflecting the strong demand for our portfolio of services,” said Amy Hood, executive vice president and chief financial officer of Microsoft.

“We exceeded expectations across revenue, operating income, and earnings per share.”

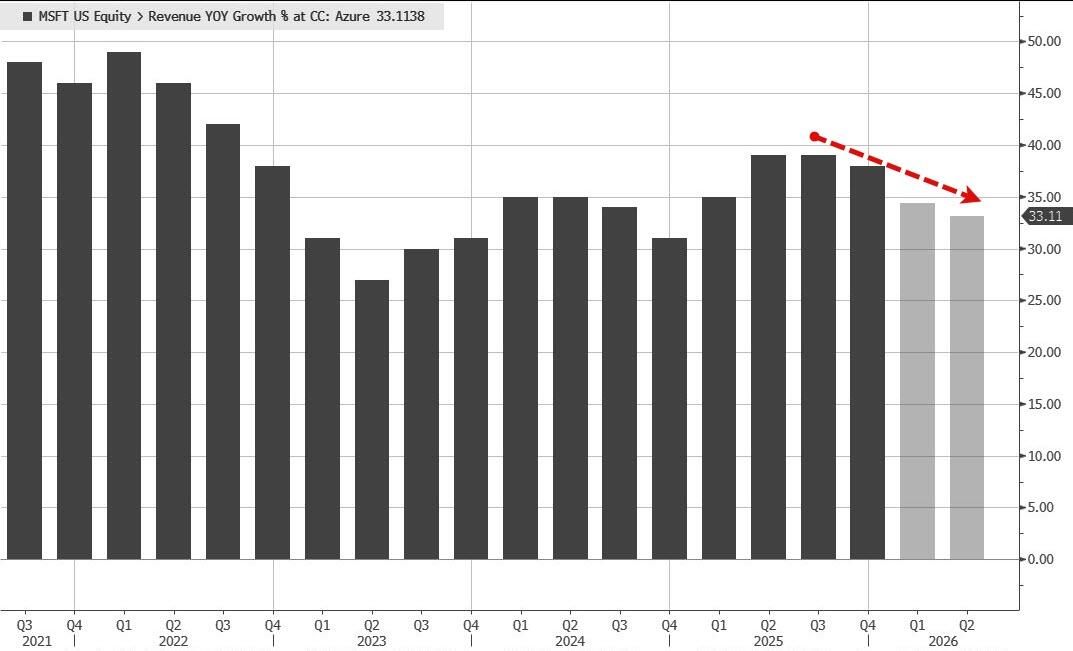

While Azure revenue rose 39% (beating stimates of 37.8%), it was down slightly from the first-quarter's 40% growth rate.

Additionally, Cloud gross margin also fell YoY to 67%.

Operating income beat expectations at $38.28 billion (versus a consensus estimate of $36.55 billion)

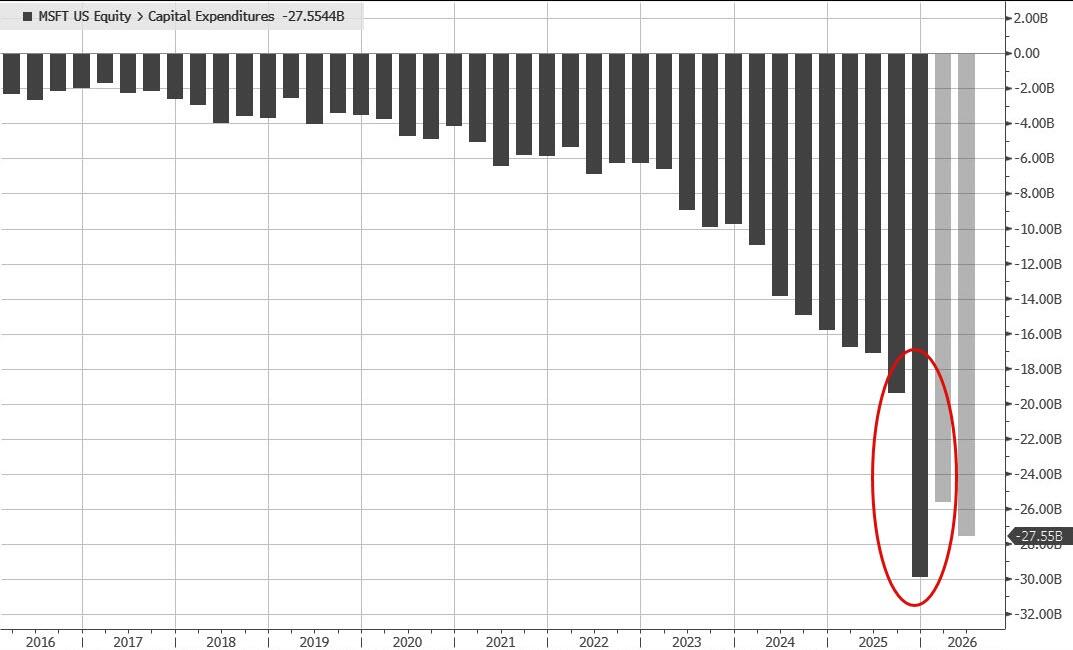

But Capital Expenditures were considerably higher than expected at $29.99 billion (versus consensus estimate of $23.78 billion).

- Capital expenditures including assets acquired under finance leases were $37.5 billion, up 66% to support customer demand for our cloud and Al offerings. Roughly two-thirds of capital expenditures were for short-lived assets, primarily GPUs and CPUs, which support Azure platform demand, growing first-party applications and Al solutions, accelerating research and development by our product teams, as well as continued replacement for end-of-life server and networking equipment.

- The remainder of capital expenditures were for long-lived assets which will support monetization over the next 15-year period and beyond. Finance leases, which are primarily for large datacenter sites, were $6.7B and are recognized at the time of lease commencement.

- Cash paid for property and equipment was $29.9 billion, up 89%, lower than capital expenditures primarily due to finance leases

Additionally, following the renegotiation of their deal, Microsoft says net gains from OpenAI investments totaled $7.6B, and more notably, 45% of Commercial Remaining Commercial Performance (RPO) from OpenAI commitments.

The OpenAI investment lifted per-share earnings by $1.02.

"In the second quarter of fiscal year 2026, net income and diluted earnings per share were impacted by net gains from investments in OpenAI, which resulted in an increase in net income and diluted earnings per share of $7.6 billion and $1.02, respectively."

The result of all this was selling pressure hitting MSFT (down over 8% after hours)...

(Click on image to enlarge)

It's unclear exactly what is triggering the selling pressure, but could it be that too much CapEx is now bad news not good news? Or is that Azure growth slowed?

More By This Author:

Despite Two Dovish Dissents, Fed Holds Rates As Expected; Upgrades Growth, Lowers Labor Risks

Amazon Cuts 16,000 Jobs As Tech Layoffs Accelerate In 2026

UPS Won't Resurrect MD-11 Fleet After Deadly Crash, Takes $137M Charge

Comments

Log in or sign up to join the conversation.