Image Source: Pixabay

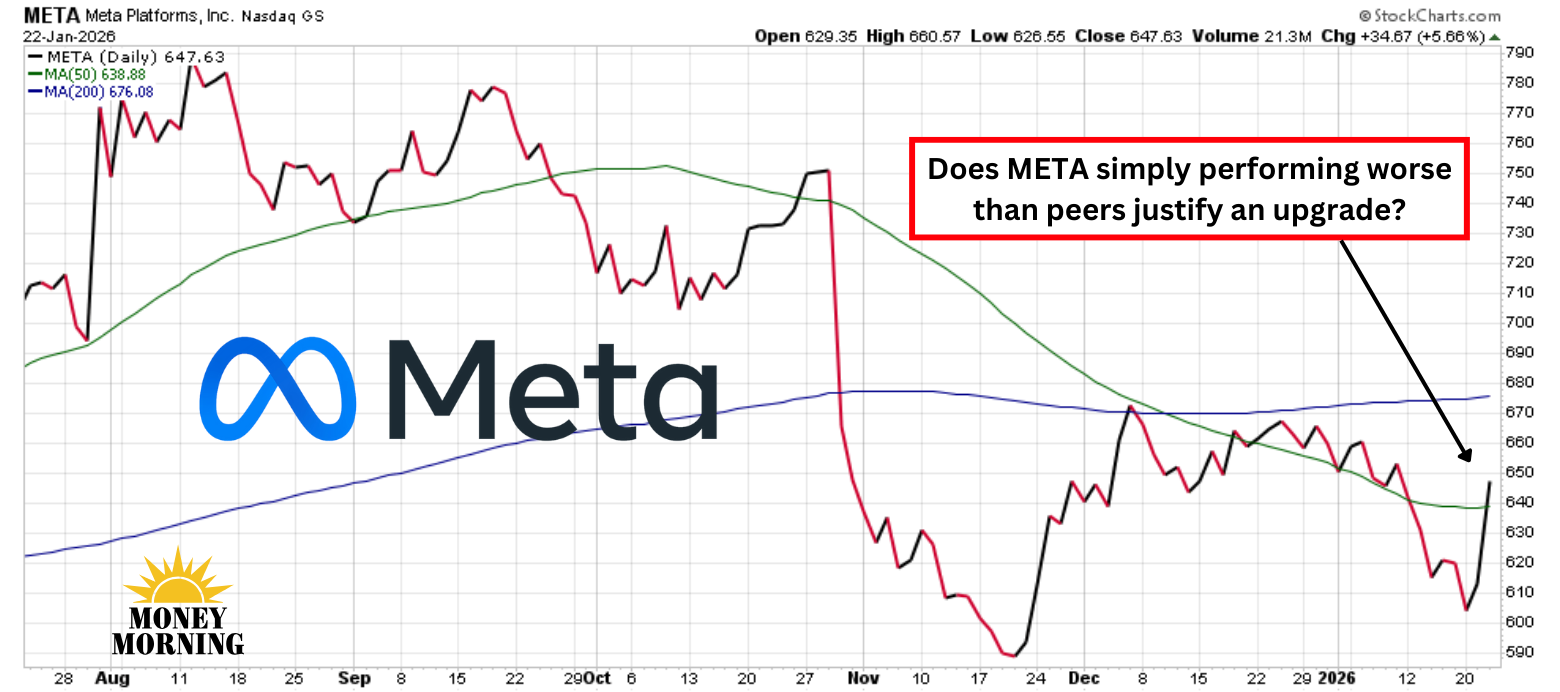

Over the past year, Meta Platforms (META) has significantly underperformed most of its Magnificent Seven counterparts, posting a meager 5% return while Alphabet (GOOG, GOOGL) surged 66% and even Apple (AAPL) managed a 12% gain. Investor skepticism has largely stemmed from Meta's aggressive shift toward artificial intelligence, which has necessitated hefty capital outlays and – for the first time in years – taking on substantial debt to fund expansive data centers and AI infrastructure.

This pivot has raised questions about long-term profitability amid ongoing losses in other ventures like Reality Labs. However, investors will get their first real glimpse into whether these AI investments are paying off.

Undervaluation Sparks Renewed Interest

Amid a broader market rebound, Meta's shares jumped more than 5% yesterday, fueled by Jefferies analyst Brent Thill maintaining his strong buy recommendation and setting a price target implying roughly 45% upside from recent levels. He emphasized Meta's position as the most affordably priced among the elite tech group, trading at under 29 times trailing earnings – a discount that stands out against peers like Alphabet, which has enjoyed far stronger gains over the last 12 months.

Thill argued that the recent sell-off following Meta's third-quarter report has created an opportune entry point, especially as the company's core digital advertising engine continues to accelerate, growing 26% in the latest period despite macroeconomic headwinds.

(Click on image to enlarge)

Looking beyond valuations, the analyst highlighted emerging revenue streams that could propel growth in 2026. Meta's messaging powerhouse WhatsApp is ramping up commercialization efforts, while its X rival Threads has hit a milestone of 400 million monthly active users. The platform is now expanding ad placements globally after successful tests in key markets, a move expected to unlock significant monetization potential.

These developments come at a time when Meta's AI initiatives are beginning to integrate more deeply with its social media ecosystems, enhancing user engagement and ad targeting precision.

Growth Amid AI Scrutiny and Geopolitical Tensions

Analysts forecast a solid performance for Q4, with consensus estimates pegging revenue at approximately $58.35 billion – a 20.6% increase year-over-year – and earnings of $8.22 per share, up modestly from the prior year's $8.02. This aligns with Meta's own guidance of $56 billion to $59 billion in sales, driven by robust holiday advertising demand across Facebook, Instagram, and other apps.

However, investors will closely watch updates on 2026 capital expenditures, which surged last year to support AI advancements, and any clarity on returns from these investments.

Complicating the picture is Meta's push into AI through acquisitions. The company recently snapped up Singapore-based startup Manus for $2 billion, aiming to bolster its agentic AI capabilities. But China is intensifying its scrutiny of the deal, expanding the investigation to encompass tech export controls, national security concerns, and cross-border investment regulations. With Manus founded by Chinese entrepreneurs, regulators in Beijing could demand modifications or even block the transaction outright, adding uncertainty to Meta's AI strategy amid escalating U.S.-China tech tensions.

Bottom Line

Meta Platforms is juggling numerous complexities right now, from ballooning AI expenditures to deep and ongoing losses at Reality Labs, making it challenging to assess if its bold bets are truly cost-effective.

While some on Wall Street view Meta's underperformance against peers as a compelling case for upgrades and potential rebounds, the market's guarded stance is justified – its discounted valuation reflects legitimate risks like regulatory hurdles and unproven returns on massive investments. Everything hinges on the Jan. 28 earnings report, which could either reignite confidence or deepen doubts.

More By This Author:

Intel Plunges After Offering Weak Guidance. Should You Buy The Dip?

For Super Micro, No News Is Good News, But Don't Chase The Rally

Wall Street's Love For IREN Heats Up. Here's Why It Is A Buy Now

Comments

Log in or sign up to join the conversation.