Image Source: Unsplash

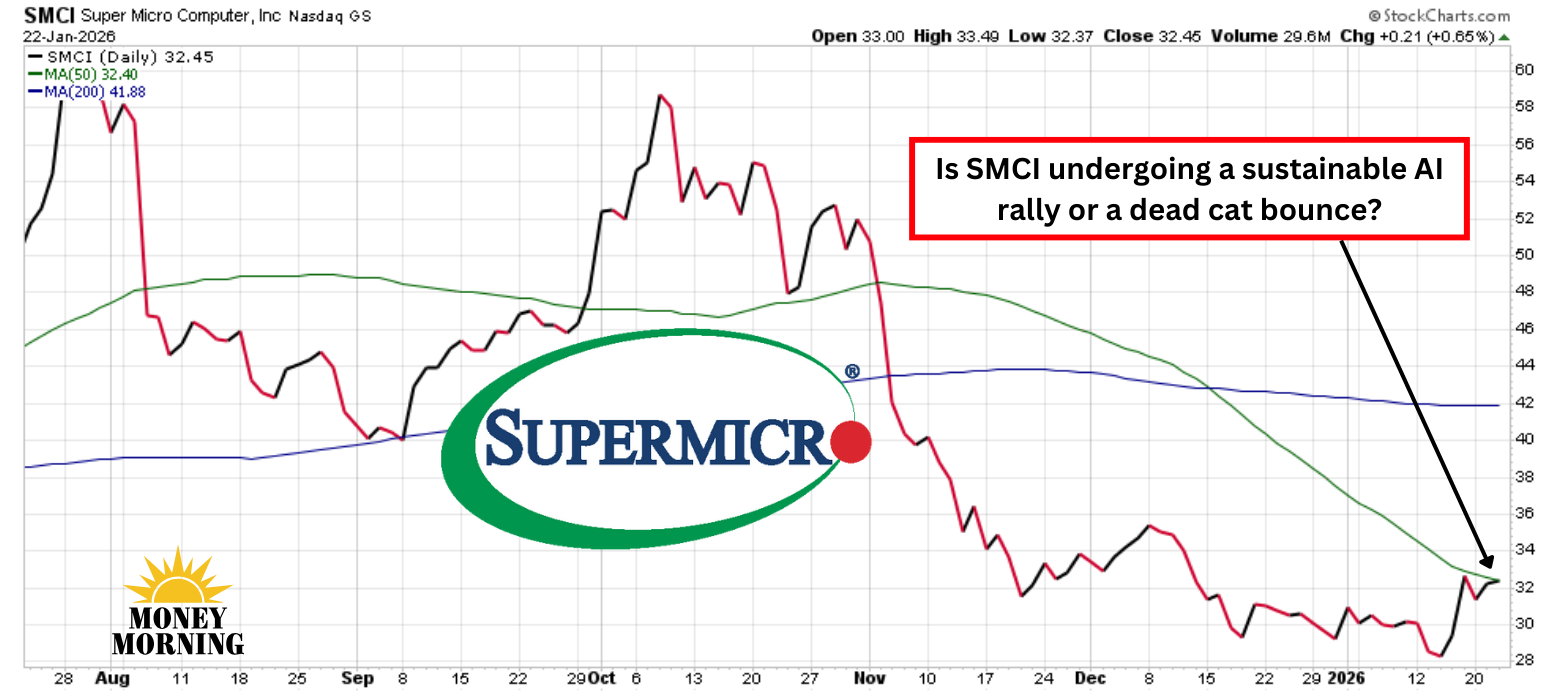

Super Micro Computer (SMCI) stock has surged about 15% over the past week, reflecting renewed trader interest in this AI server player. Yesterday, the company announced it will report fiscal Q2 2026 results on Feb. 3, sparking a 3.4% rise in pre-market trading this morning.

Notably, the press release focused solely on the earnings date and conference call details, without any pre-announcement warnings about revenue shortfalls or execution hiccups. This absence of caution – unlike the past two quarters, where management flagged misses ahead of time – stands out. While it removes a familiar negative catalyst, the "news" is mostly the lack of bad news, hardly justification for chasing the rally higher at current levels.

Why the AI Boom Has Largely Passed SMCI By

Despite riding the AI wave as a key supplier of high-performance servers optimized for GPU workloads (with AI platforms driving over 75% of recent revenue), Super Micro has underperformed the broader AI infrastructure surge. Competitors like Dell (DELL) and Hewlett Packard Enterprise (HPE) have captured more market share through diversified portfolios, stronger supply chains, and bundled enterprise solutions that allow them to avoid the deepest price concessions in massive AI deals.

SMCI's challenges stem from execution missteps, including delayed shipments, customer logistics issues, and supply chain vulnerabilities tied to GPU availability. Fiscal Q1 2026 revenue came in at around $5 billion, a sharp 15% year-over-year drop and well below the company's $6 billion to $7 billion guidance, missing consensus by roughly 17%. Gross margins compressed dramatically to the low double-digits, with further erosion expected from ramp-up costs on next-gen platforms like Nvidia's (NVDA) Blackwell series.

(Click on image to enlarge)

These pressures have led to consecutive misses, eroding investor confidence amid governance concerns, auditor issues, rising inventories, and receivables. Intense competition has also forced SMCI into lower-margin territory to secure hyperscaler orders, while broader macroeconomic factors and internal control deficiencies added headwinds. The result: shares have shed over 50% from 2025 peaks, trading near multi-year lows despite the explosive AI demand environment.

A Sign of Stability – or Just Relief?

Traders appear to interpret yesterday's plain-vanilla earnings date announcement as cautiously positive. In prior cycles, Super Micro paired such notices with preliminary downside revisions or shortfall signals, triggering sharp sell-offs. The omission this time suggests no immediate red flags on the horizon, potentially pointing to smoother operations, better backlog conversion, or stronger-than-expected traction in high-demand AI servers.

With $13 billion in orders tied to Blackwell and management guiding for at least $36 billion in full-year fiscal 2026 revenue (implying robust growth acceleration), the lack of warnings fuels speculation of a performance rebound. The recent lift in its stock price – partly tied to positive signals from partners like Taiwan Semiconductor Manufacturing (TSM) on sustained AI chip demand – reinforces this view for momentum players.

Bottom Line

Even if Feb. 3 brings stronger-than-expected results – beating lowered expectations or affirming upbeat guidance – investors should resist piling in aggressively. One solid quarter does not make a trend, and even a broken clock is right twice a day. Ongoing issues like margin compression, competitive pricing pressures, execution risks, and governance overhangs remain unresolved.

True sustainability requires multiple quarters of consistent delivery, margin stabilization, and market share gains. Waiting for that proof – even if it means potentially missing a bottom – beats chasing a rally that could fade if old problems resurface. Patience may preserve capital for a more convincing turnaround.

More By This Author:

Wall Street's Love For IREN Heats Up. Here's Why It Is A Buy NowIs This The Biggest Threat To Vistra's Growth Trajectory?

DraftKings Tumbles On NCAA Betting Ban Proposal. Should You Buy The Dip?

Comments

Log in or sign up to join the conversation.