Yesterday, McDonalds issued a health warning in their earnings announcement. The warning is not about the physical health of its consumers but the customers’ financial health. McDonalds global sales were down 1%, and U.S. sales fell by 0.7% in the second quarter. Moreover, as shown below, its same-store sales have fallen for the first time since 2020. Same-store sales only account for revenue from existing stores. Thus, revenue added due to the growth in the number of stores is eliminated. This is the preferred measure of sales for most retail outlets.

The McDonalds CEO opened the earnings call by saying low-end consumer weakness has deepened and broadened. We have heard this theme in many retail earnings announcements over the past six months. Savings have been depleted, and credit card debt has accelerated, leaving many consumers lacking funds to consume at prior rates. Typically, lower-end restaurants like McDonalds fare well during economic slowdowns or recessions due to their low prices. This time, however, its prices are not so low in the consumer’s mind. The Big Mac, for instance, averages $5.29, an increase of over 20% since the pandemic. Throw in fries and a drink, and the meal is over $10 in many locations. Any wonder McDonalds extended its $5 value meal, and many of its competitors offer similar deals.

(Click on image to enlarge)

What To Watch Today

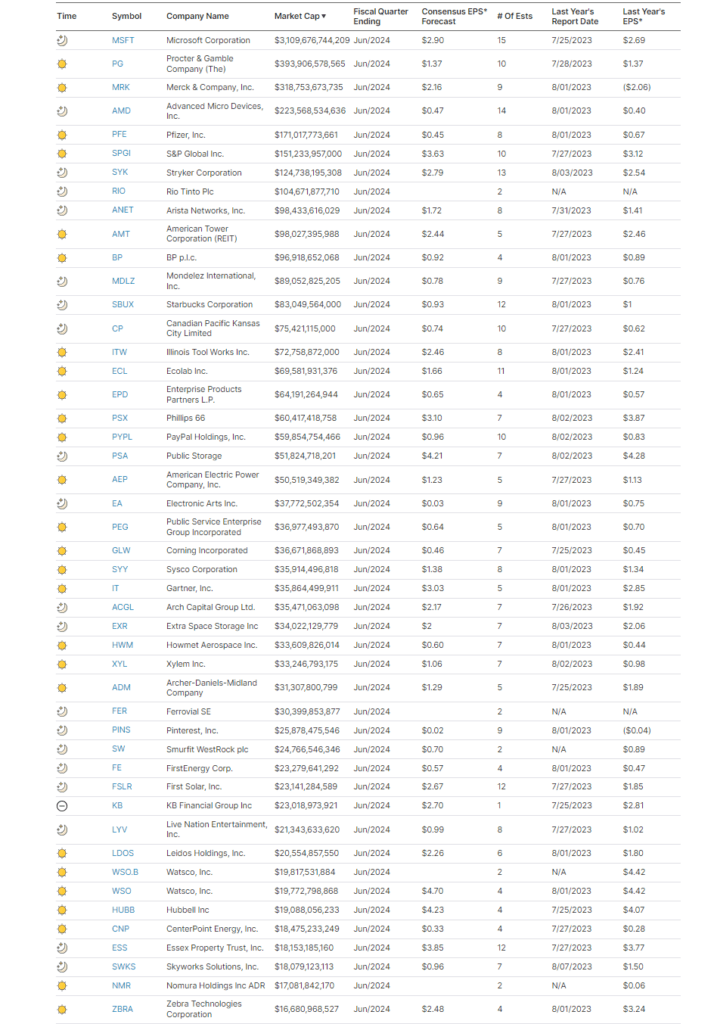

Earnings

(Click on image to enlarge)

Economy

(Click on image to enlarge)

Market Trading Update

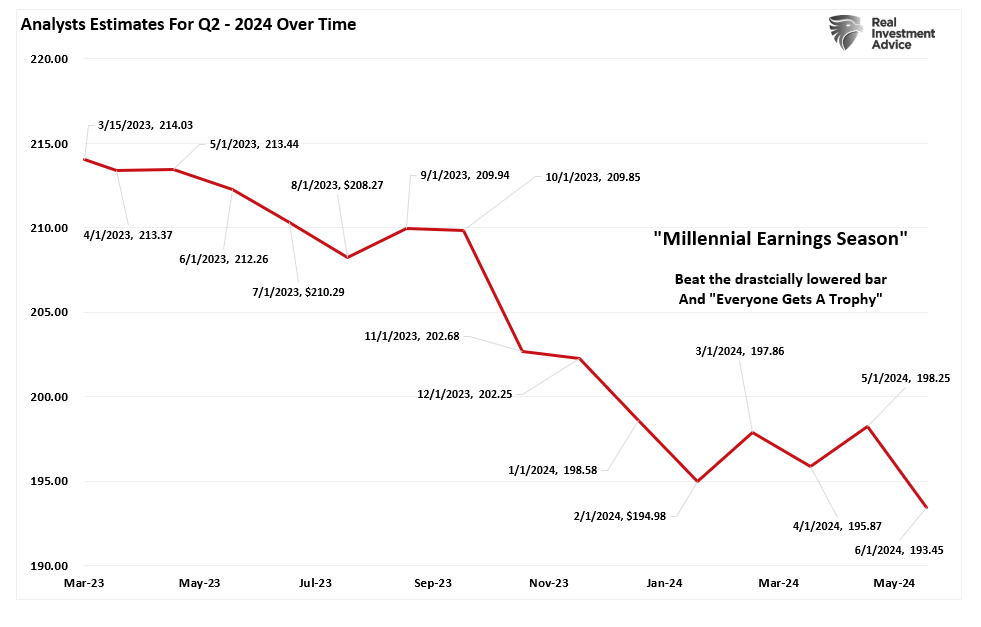

At the beginning of July, we discussed the “lowering of the earnings bar” for the Q2 reporting period. To wit:

“It will be unsurprising that we will see a high percentage of companies “beat” Wall Street estimates. Of course, the high beat rate is always the case due to the sharp downward revisions in analysts’ estimates as the reporting period begins. The chart below shows the changes for the Q2 earnings period from when analysts provided their first estimates in March 2023. Analysts have slashed estimates over the last 30 days, dropping estimates by roughly $5/share.”

(Click on image to enlarge)

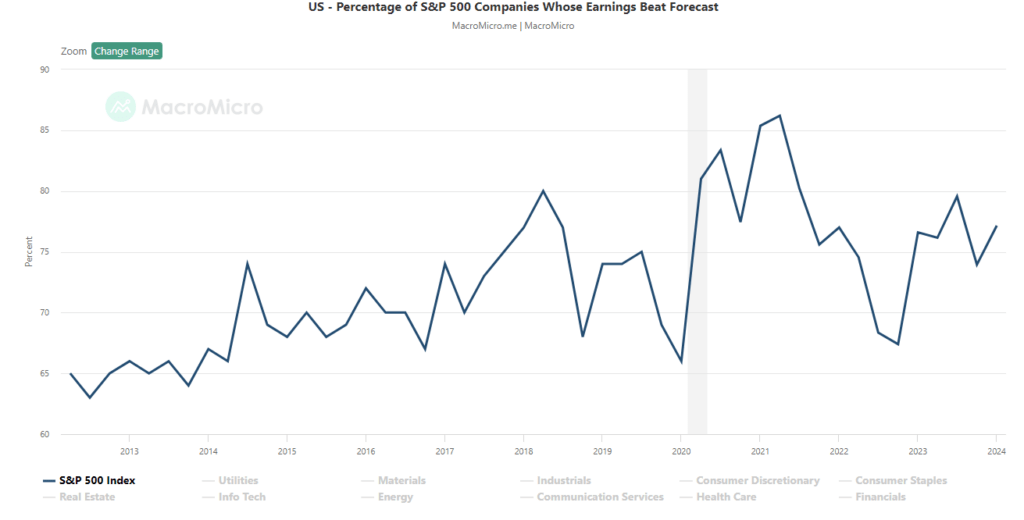

“That is why we call it “Millennial Earnings Season.” Wall Street continuously lowers estimates as the reporting period approaches so “everyone gets a trophy.” An easy way to see this is the number of companies beating estimates each quarter, regardless of economic and financial conditions. Since 2000, roughly 70% of companies regularly beat estimates by 5%, but since 2017, that average has risen to approximately 75%. Again, that “beat rate” would be substantially lower if investors held analysts to their original estimates.”

(Click on image to enlarge)

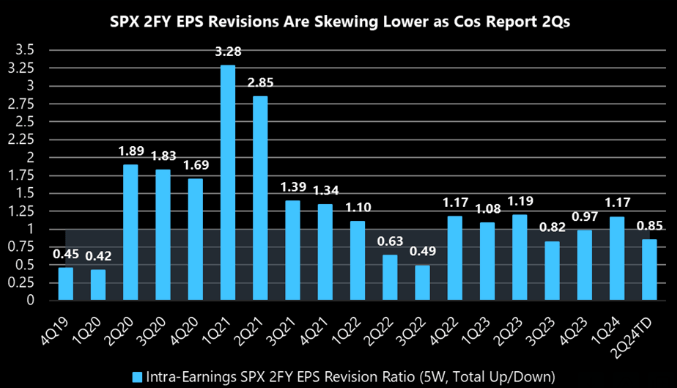

During just this past month, the expected earnings for not just Q2 but through 2025 have been cut further. As noted by Jefferies:

“….the negative revision skew (to earnings) is below the magic 1x level and bottom quartile. Although the magnitude of cuts is different vs. lockdowns & the tech layoffs, the mismatch between CY25 expectations earlier in the year vs. now looks widespread across most sectors as 7 of 11 are <1x.”

(Click on image to enlarge)

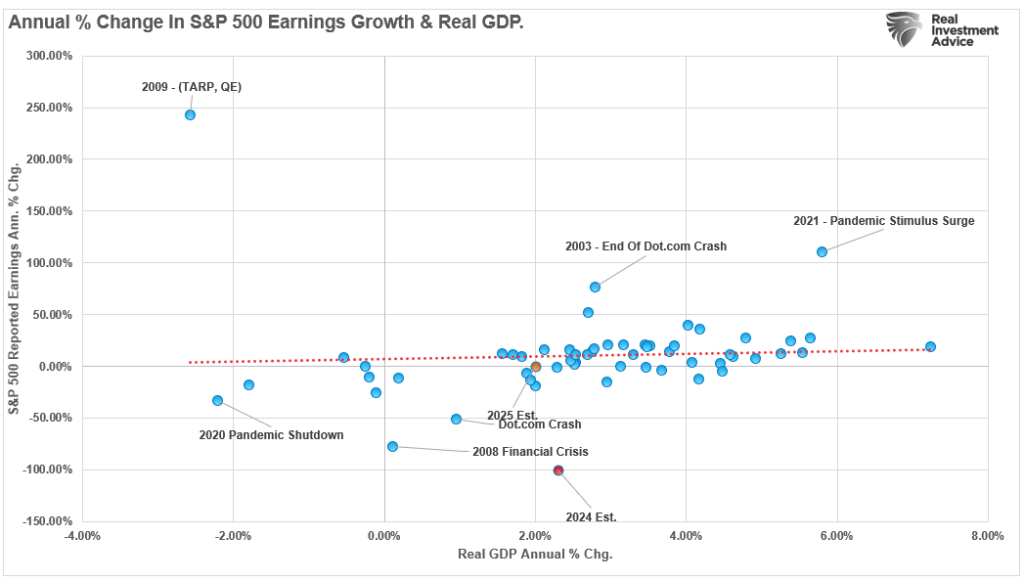

Given the current state of consumer data and the potential for slower economic growth in the months ahead, current Wall Street expectations seem overly optimistic. Furthermore, given the correlation between earnings and economic growth, a more cautious outlook would seem in order.

(Click on image to enlarge)

As noted previously:

“For investors, the most significant risk to portfolios is not inflation but most likely disinflation as the economy, and ultimately earnings, come under pressure in the months ahead. Such is crucial given that expectations for earnings growth in the overall index remain elevated, but that growth depends on just 7 stocks. In fact, since the beginning of this bull market cycle in Q4 of 2022, there has been ZERO earnings growth in the bottom 493 stocks of the S&P 500.”

(Click on image to enlarge)

We must pay close attention to consumer data. It will likely provide the warnings necessary to reduce equity risk in portfolios.

As the economy slows, the subsequent decline in earnings is unsurprising. With valuations high, a deeper correction to revert company prices to slower underlying earnings growth is becoming a higher probability event. As such, we suggest remaining cautious for now and managing exposure to companies with the highest probability of negative earning revisions in the near term.

More By This Author:

Bullish Years Often Have CorrectionsDoctor Copper Warns Of Slowing Growth

Market Correction Doesn't Deter Investor Bullishness

Comments

Log in or sign up to join the conversation.