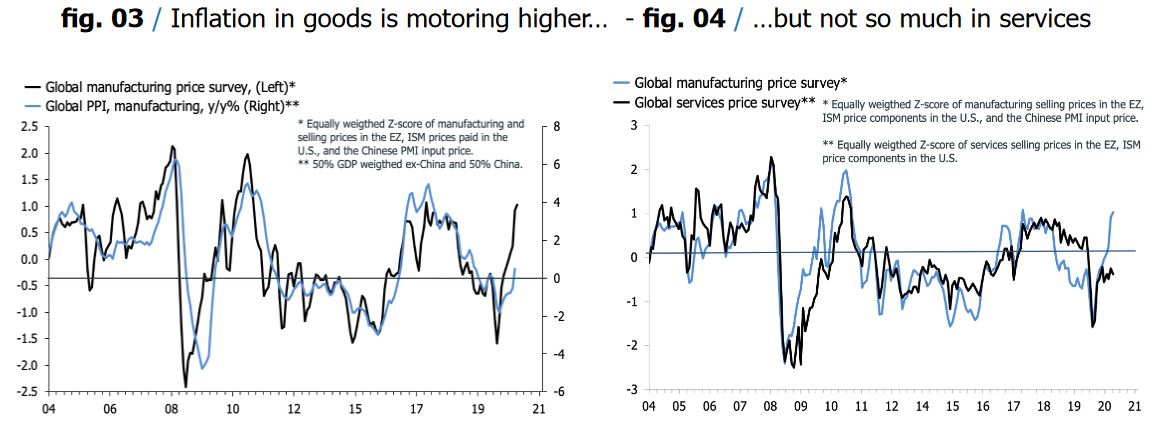

With every report that shows the inflation rate falling, financial analysts bombard the airwaves with alarmist calls for a pause in Fed rate hikes to avoid recession. They usurp a mantle of credibility by saying they knew the Fed was wrong last year for calling inflation “transitory”, therefore the Fed must be wrong again for assuming prolonged or sticky inflation that requires sustained credit tightening. With the Federal Funds Rate now at 4.25%, the majority think the Fed has presaged an economic Recession. This fear should continue growing over the next few quarters as the interbank Fed borrowing rate should reach 5% on March 21st and remain above 5% until at least Q3 of next year. By the end of summer, full employment will falter as unemployment approaches 4.5%, while the Fed’s core Personal Consumption Expenditures (PCE) inflation index should be testing 3% in Q3. For now, it’s premature to expect a Powell pivot until Q3 as the Fed Chair has learned that a single misconstrued word or inadvertent facial expression could trigger a massive market rally and irrational consumer exuberance that would delay his stable 2% PCE target and prolong the pain. The good news is that we have all reduced spending on “stuff” but continue to spend at exceedingly elevated levels on “fun”. The manufacturing sector is now experiencing deflation, so the Fed has turned its steely gaze toward the overinflated and much larger service sector. Expect further credit tightening by banks until consumer debt default rates and unemployment move decisively higher and until travel and leisure spend decline sharply.

(Click on image to enlarge)

With the Fed’s core PCE inflation gauge remaining near a 40-year high, we project that the knock-on or cumulative effects of the trailing 12 months will show a more persistent inflation decline over the next 7 months close to 3%. Once unemployment begins to tick above 4%, we suspect the “sticky” components of inflation such as owners’ equivalent rent, insurance, and healthcare, will begin to roll over and journey toward 3% as well, while recession fears grow. Core PCE could even reach 2.5% in the October 2023 report. Historically, it the Fed has finished its tightening cycle and spend months stimulating prior to the stocks entering a new Bull market. However, with the secular shortage of the labor supply due to aging demographics favoring fuller employment, we expect stocks to quickly enter a long-term uptrend once there is consensus that the Fed inflation battle has been won and lower rates are just around the bend.

(Click on image to enlarge)

With elevated interest rates for longer in 2023 awaiting weaker consumer spending, corporate profits will have to suffer in unison. Yet, for the past 8 straight quarters the SP 500 earnings have been growing year over year (YoY). There is a good chance that when Q4 2022 earnings are reported in January and February ’23, we will see the first YoY earnings decline.

(Click on image to enlarge)

Once labor supply relaxes and corporate earnings estimates fall more substantially in Q2, equity markets may finally be ready to anticipate upside catalysts roughly six months prior to a mission accomplished inflation number under 3%. It’s possible that price-to-earnings (P/E) multiples can move higher while earnings fall to ameliorate stock price declines, but contracting profit trends remove any catalyst for a sustained new Bull market over the next few months. A defensive portfolio with a high cash posture yielding ~ 4% risk-free, remains the plan with a core Healthcare, food, and defense exposure. The fact that our cautious outlook has become a stronger consensus over the past month fits with our chart below for a short-term rally, from a contrarian perspective. Readers know that we had expected a rally from early October to early December with a pullback until just before Christmas. As this occurred and as evidenced by our indicators below, sentiment has become washed out and our Seasonality pattern now favors a modest rebound into mid-January. Any price failure below the December bottom over the next few months would strongly favor a continuation to new lows in March or May time windows.

(Click on image to enlarge)

More By This Author:

Inflation Will Fall, But When?

Fed Soothsayers Expecting A Pause And Year End Rally

Has The Inflation Reduction Act Already Reduced Inflation?

Comments

Log in or sign up to join the conversation.