A year ago, the Fed Funds futures market thought the Fed would have cut rates two to three times before the July 31, 2024 FOMC meeting. Two weeks ago, the odds of a rate cut at the July 31 meeting were near zero. Furthermore, the market was only pricing in one cut for the remainder of the year. With Friday’s jobs report, a fragile ISM report detailed below, and renewed signs that the disinflation trend may be resuming, the prospect of a July 31 rate cut back into focus.

On Friday, the BLS reported the economy gained 206k jobs. The growth was slightly better than expected; however, the unemployment rate rose from 4.0% to 4.1%. Further, the April and May jobs figures were revised lower by 111k in aggregate. Like the prior few employment reports, this report was good from a headline perspective, but a look beneath the hood is troubling.

So, with the unemployment rate ticking up, might the Fed cut rates as soon as July if this week’s inflation data is weak? While the odds remain low, we will watch Jerome Powell’s speeches on Tuesday and Wednesday for clues. This weekend’s Newsletter discusses why the thought of a Fed cut in July is not unthinkable. Per the article, “We don’t think so, but the data is becoming more supportive of action. However, if the Fed cuts rates in July, it is likely a good signal that we will need to become less aggressive on equity allocations.“

What To Watch Today

Earnings

- There are no significant reports today.

Economy

- There are no significant reports today.

Market Trading Update

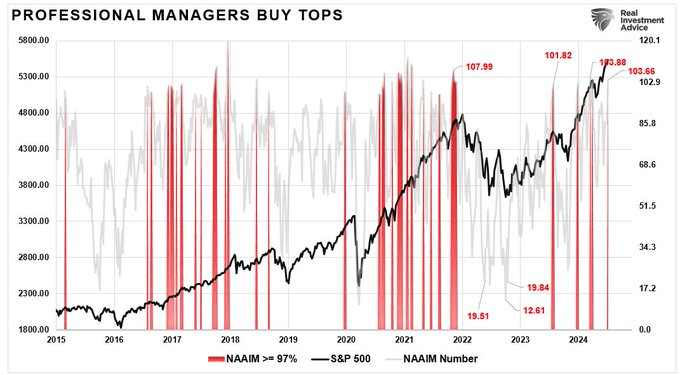

The market continues in a very bullish trend, with investors increasingly confident that they will receive higher returns. That infectious greed has also spilled over onto professionals, with their equity exposure exceeding 100%. While such is a warning sign, it does not necessarily mean the markets will have a deep correction. However, such positioning extremes have previously marked short-term tops and consolidations.

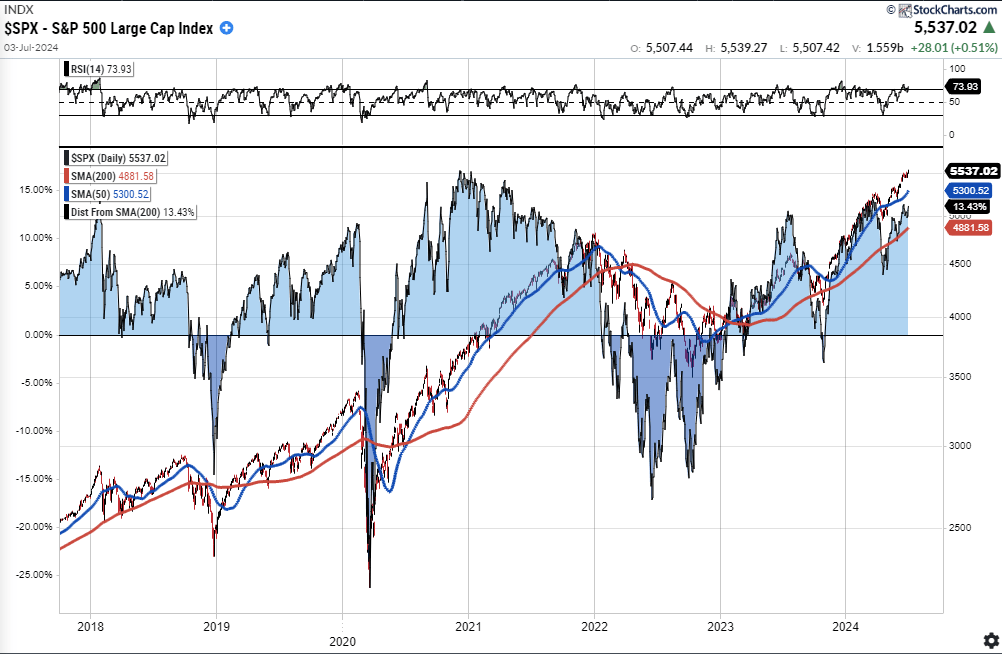

Furthermore, the market’s deviation from the underlying 200-DMA is also starting to reach levels that have previously preceded short-term market corrections or consolidations. As is always the case, for an “average” to exist, the market must trade above and below that average over time. Therefore, the more extreme the deviation from that average, the stronger the pull for a reversion.

These are warning signs that the market needs a short-term correction or consolidation to alleviate those conditions. Such a process would be healthy for a continued bullish advance. However, it doesn’t mean it will happen today or this month. As is always the case, timing is the critical part.

Trade accordingly.

The Week Ahead

This week will be highlighted by CPI on Thursday, PPI on Friday, two Jerome Powell appearances, and the start of earnings reporting season.

If the Fed is going to cut rates on July 31, it will likely require a lower-than-expected CPI number. The market expects CPI to rise by 0.1% and Core CPI by 0.2%. After declining by 0.2% last month, PPI is expected to increase by 0.2%. Jerome Powell speaks on Tuesday and Wednesday. He will likely have the inflation reports before the speeches.

Earnings season kicks off this week, with the large banks reporting earnings on Friday. The following week, a broader array of company earnings reports will be released.

ISM Services Was Much Weaker Than Expected

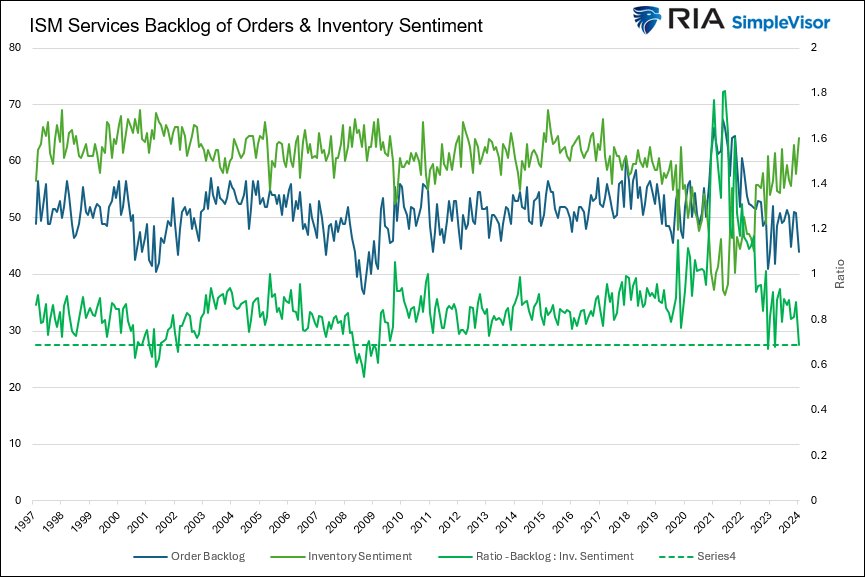

For the first time since 2009, excluding April and May of 2020, the ISM services index (blue- -lower graph) is in economic contraction territory. Wednesday’s reading of 48.8 was well below estimates of 52.7 and the prior reading of 53.8. Within the index, the prices paid index was weaker than expectations although still above 50, pointing to higher prices. That said, the manufacturing and services ISM are seeing their price indexes resume lower trends. Of the most concern is the employment index. It came in at 46.1, well below the estimate of 49.5. Such further affirms that the BLS headline job growth figures may be overstating the actual state of the labor markets. This is not lost on the Fed as they have acknowledged such.

New orders, a good leading indicator of activity, were also well below expectations at 47.3 versus an expected 53.6. The first graph below shows a robust leading economic indicator for the service sector. The ratio of order backlogs to inventory sentiment is in recessionary territory. Furthermore, within the report is the following quote:

The percentage of ISM Services respondents expecting higher new orders is at its lowest since the GFC and lower than ’01 recession

Tweet of the Day

More By This Author:

Rate Cut In July?The Economy Is Normalizing – Whats Next?

7-2-24 Interest Rates Are A Function Of Inflation And Economic Growth

Comments

Log in or sign up to join the conversation.